- Money Markets. Lecture 10

Содержание

- 2. Lecture 10. Money Markets Murodullo Bazarov [email protected] ATB205 office hours: Tues 11:00-13:00

- 3. Lecture Outline The Money Markets Defined The Purpose of Money Markets Who Participates in Money Markets?

- 4. The Money Markets Defined The term “money market” is a misnomer. Money (currency) is not actually

- 5. Why Do We Need Money Markets? The banking industry should handle the needs for short-term funding

- 6. Cost Advantages of Money Markets Reserve requirements create additional expense for banks that money markets do

- 7. 3-month T-bill rates and Interest Rate Ceilings

- 8. The Purpose of Money Markets Investors in Money Market: Provides a place for warehousing surplus funds

- 9. Sample rates from the Federal Reserve Sample Money Market Rates, May 15, 2013

- 10. Who Participates in the Money Markets?

- 11. Money Market Instruments Treasury Bills Federal Funds Repurchase Agreements Negotiable Certificates of Deposit Commercial Paper Banker’s

- 12. Money Market Instruments: Treasury Bills T-bills have 28-day maturities through 12- month maturities. Discounting: When an

- 13. Money Market Instruments: Treasury Bills T-bills are auctioned to the dealers every Thursday. The Treasury may

- 14. Money Market Instruments: Treasury Bills The Treasury accepts the following bids: Bidder Bid Amount Bid Price

- 15. Money Market Instruments: Treasury Bills

- 16. Money Market Instruments: Fed Funds Short-term funds transferred (loaned or borrowed) between financial institutions, usually for

- 17. Money Market Instruments: Fed Funds Federal Funds and Treasury Bill Interest Rates, January 1990–January 2013

- 18. Money Market Instruments: Repurchase Agreements These work similar to the market for fed funds, but nonbanks

- 19. Money Market Instruments: Negotiable Certificates of Deposit A bank-issued security that documents a deposit and specifies

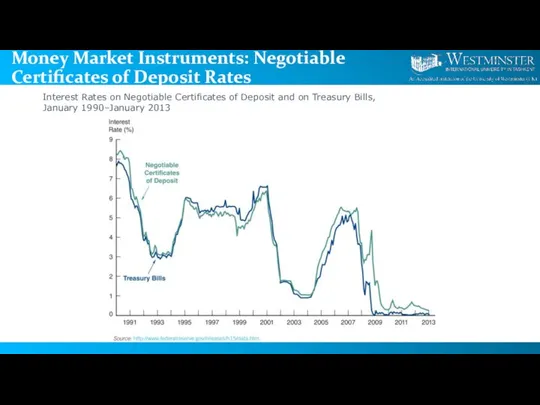

- 20. Money Market Instruments: Negotiable Certificates of Deposit Rates Interest Rates on Negotiable Certificates of Deposit and

- 21. Money Market Instruments: Commercial Paper Unsecured promissory notes, issued by corporations, that mature in no more

- 22. Money Market Instruments: Commercial Paper Rates Return on Commercial Paper and the Prime Rate, 1990–2013

- 23. Money Market Instruments: Commercial Paper Volume Volume of Commercial Paper Outstanding

- 24. Money Market Instruments: Banker’s Acceptances An order to pay a specified amount to the bearer on

- 25. Money Market Instruments: Eurodollars Eurodollars represent Dollar denominated deposits held in foreign banks. The market is

- 26. Money Market Instruments: Eurodollars Rates London interbank bid rate (LIBID) The rate paid by banks buying

- 27. Global: Birth of the Eurodollar The Eurodollar market is one of the most important financial markets,

- 28. Comparing Money Market Securities : a comparison of rates (1990-2013)

- 29. Comparing Money Market Securities: Money Market Securities and Their Depth

- 31. Скачать презентацию

Слайд 2Lecture 10.

Money Markets

Murodullo Bazarov

[email protected]

ATB205

office hours: Tues 11:00-13:00

Lecture 10.

Money Markets

Murodullo Bazarov

[email protected]

ATB205

office hours: Tues 11:00-13:00

Слайд 3Lecture Outline

The Money Markets Defined

The Purpose of Money Markets

Who Participates in

Lecture Outline

The Money Markets Defined

The Purpose of Money Markets

Who Participates in

Слайд 4The Money Markets Defined

The term “money market” is a misnomer. Money (currency)

The Money Markets Defined

The term “money market” is a misnomer. Money (currency)

Слайд 5Why Do We Need Money Markets?

The banking industry should handle the needs

Why Do We Need Money Markets?

The banking industry should handle the needs

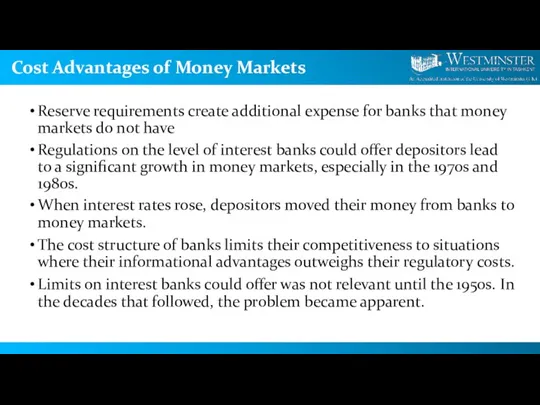

Слайд 6Cost Advantages of Money Markets

Reserve requirements create additional expense for banks that

Cost Advantages of Money Markets

Reserve requirements create additional expense for banks that

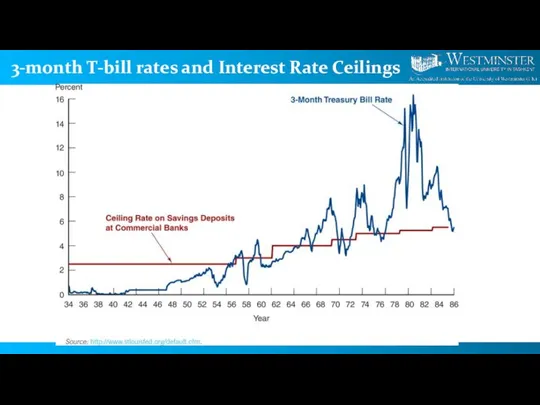

Слайд 73-month T-bill rates and Interest Rate Ceilings

3-month T-bill rates and Interest Rate Ceilings

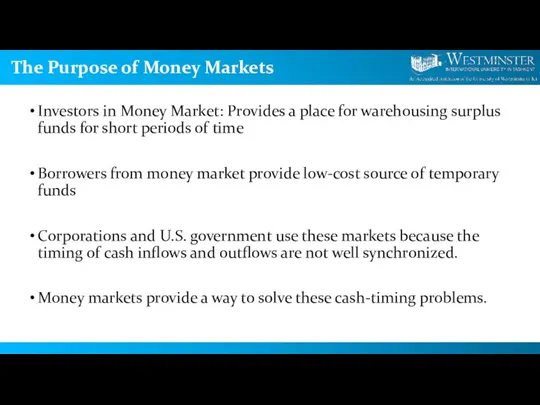

Слайд 8The Purpose of Money Markets

Investors in Money Market: Provides a place for

The Purpose of Money Markets

Investors in Money Market: Provides a place for

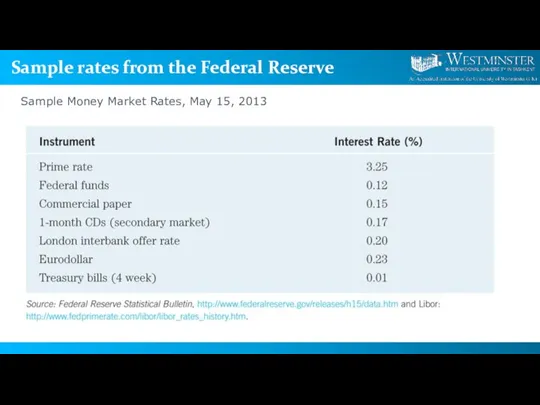

Слайд 9Sample rates from the Federal Reserve

Sample Money Market Rates, May 15, 2013

Sample rates from the Federal Reserve

Sample Money Market Rates, May 15, 2013

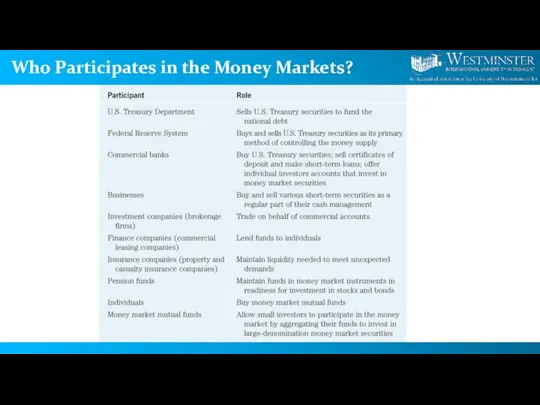

Слайд 10Who Participates in the Money Markets?

Who Participates in the Money Markets?

Слайд 11Money Market Instruments

Treasury Bills

Federal Funds

Repurchase Agreements

Negotiable Certificates of Deposit

Commercial Paper

Banker’s Acceptance

Eurodollars

Money Market Instruments

Treasury Bills

Federal Funds

Repurchase Agreements

Negotiable Certificates of Deposit

Commercial Paper

Banker’s Acceptance

Eurodollars

Слайд 12Money Market Instruments: Treasury Bills

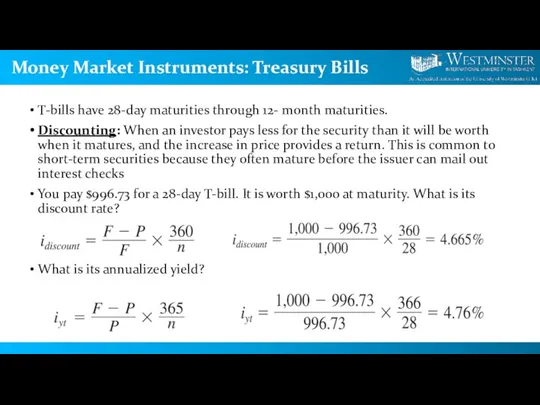

T-bills have 28-day maturities through 12- month maturities.

Money Market Instruments: Treasury Bills

T-bills have 28-day maturities through 12- month maturities.

Слайд 13Money Market Instruments: Treasury Bills

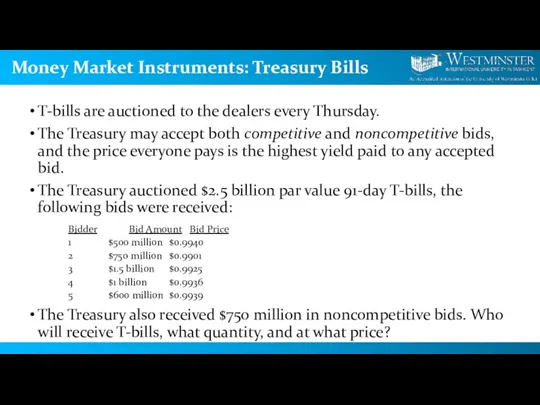

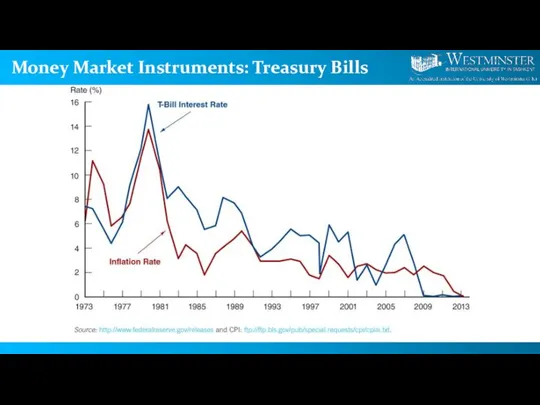

T-bills are auctioned to the dealers every Thursday.

The

Money Market Instruments: Treasury Bills

T-bills are auctioned to the dealers every Thursday.

The

Слайд 14Money Market Instruments: Treasury Bills

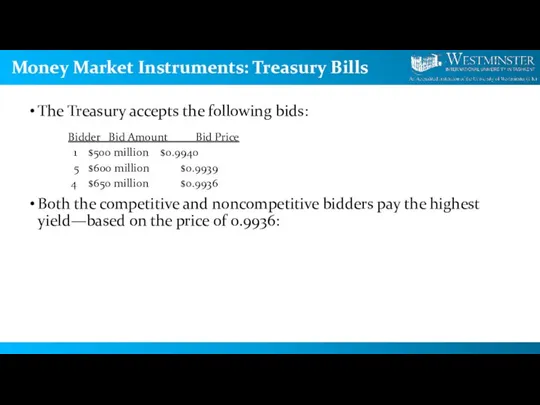

The Treasury accepts the following bids:

Bidder Bid Amount

Money Market Instruments: Treasury Bills

The Treasury accepts the following bids:

Bidder Bid Amount

Слайд 15Money Market Instruments: Treasury Bills

Money Market Instruments: Treasury Bills

Слайд 16Money Market Instruments: Fed Funds

Short-term funds transferred (loaned or borrowed) between financial

Money Market Instruments: Fed Funds

Short-term funds transferred (loaned or borrowed) between financial

Слайд 17Money Market Instruments: Fed Funds

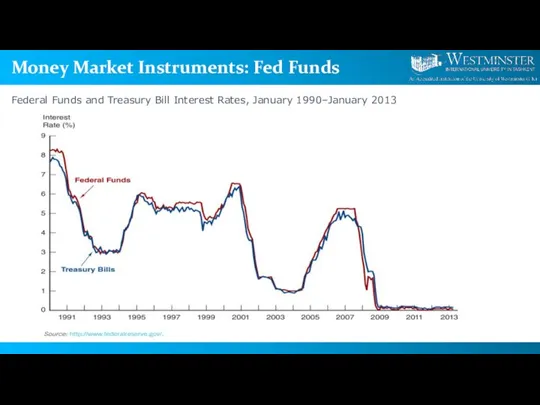

Federal Funds and Treasury Bill Interest Rates, January

Money Market Instruments: Fed Funds

Federal Funds and Treasury Bill Interest Rates, January

Слайд 18Money Market Instruments:

Repurchase Agreements

These work similar to the market for fed

Money Market Instruments:

Repurchase Agreements

These work similar to the market for fed

Слайд 19Money Market Instruments: Negotiable Certificates of Deposit

A bank-issued security that documents a

Money Market Instruments: Negotiable Certificates of Deposit

A bank-issued security that documents a

Слайд 20Money Market Instruments: Negotiable Certificates of Deposit Rates

Interest Rates on Negotiable Certificates

Money Market Instruments: Negotiable Certificates of Deposit Rates

Interest Rates on Negotiable Certificates

Слайд 21Money Market Instruments:

Commercial Paper

Unsecured promissory notes, issued by corporations, that mature

Money Market Instruments:

Commercial Paper

Unsecured promissory notes, issued by corporations, that mature

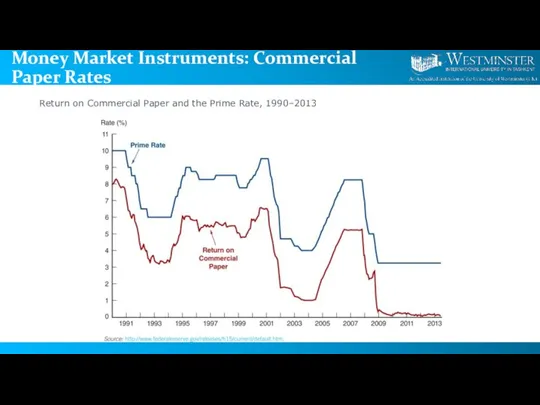

Слайд 22Money Market Instruments: Commercial Paper Rates

Return on Commercial Paper and the

Money Market Instruments: Commercial Paper Rates

Return on Commercial Paper and the

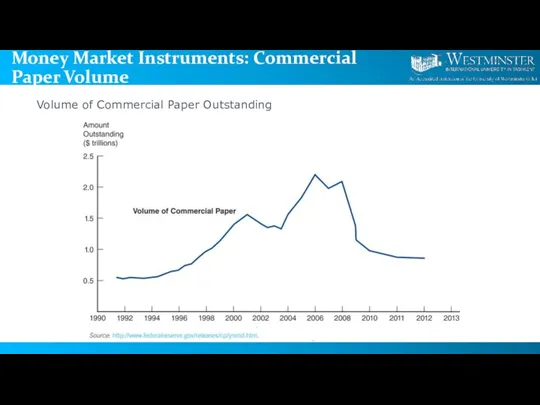

Слайд 23Money Market Instruments: Commercial Paper Volume

Volume of Commercial Paper Outstanding

Money Market Instruments: Commercial Paper Volume

Volume of Commercial Paper Outstanding

Слайд 24Money Market Instruments:

Banker’s Acceptances

An order to pay a specified amount to

Money Market Instruments:

Banker’s Acceptances

An order to pay a specified amount to

Слайд 25Money Market Instruments: Eurodollars

Eurodollars represent Dollar denominated deposits held in foreign banks.

The

Money Market Instruments: Eurodollars

Eurodollars represent Dollar denominated deposits held in foreign banks.

The

Слайд 26Money Market Instruments: Eurodollars Rates

London interbank bid rate (LIBID)

The rate paid by

Money Market Instruments: Eurodollars Rates

London interbank bid rate (LIBID)

The rate paid by

Слайд 27Global: Birth of the Eurodollar

The Eurodollar market is one of the most

Global: Birth of the Eurodollar

The Eurodollar market is one of the most

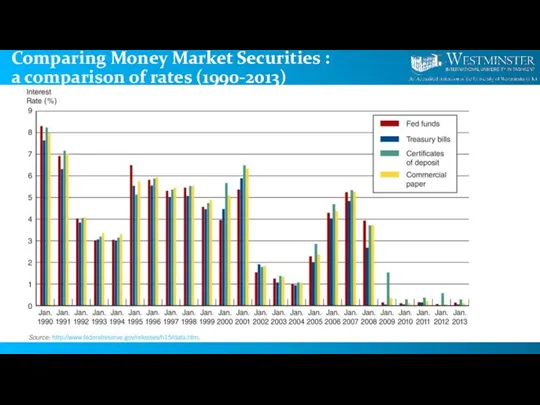

Слайд 28Comparing Money Market Securities : a comparison of rates (1990-2013)

Comparing Money Market Securities : a comparison of rates (1990-2013)

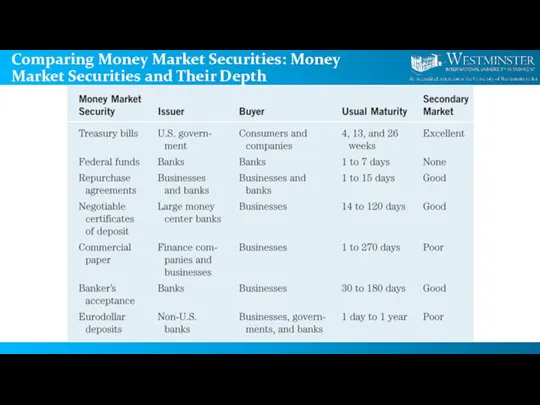

Слайд 29Comparing Money Market Securities: Money Market Securities and Their Depth

Comparing Money Market Securities: Money Market Securities and Their Depth

Фарцовка в СССР

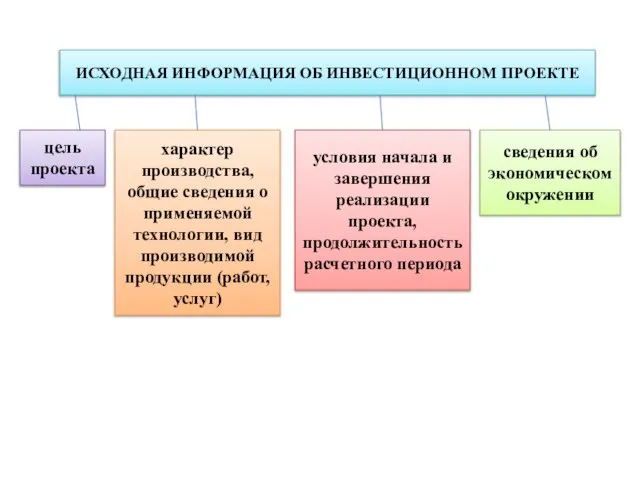

Фарцовка в СССР Исходная информация об инвестиционном проекте

Исходная информация об инвестиционном проекте Организация процесса труда. Нормирование труда

Организация процесса труда. Нормирование труда Конкуренция

Конкуренция Формальные и неформальные группы: внутригрупповое и межгрупповое взаимодействие

Формальные и неформальные группы: внутригрупповое и межгрупповое взаимодействие Информация для потребителя

Информация для потребителя Теоретические основы современных технологий

Теоретические основы современных технологий Основные понятия и сущность: мирового хозяйства, МРТ и мирового рынка. Подготовили Волчкова А.А. и Дёмина И.А.

Основные понятия и сущность: мирового хозяйства, МРТ и мирового рынка. Подготовили Волчкова А.А. и Дёмина И.А. Приоритетные направления инновационного развития

Приоритетные направления инновационного развития Испания и ЕС - 21 век. Региональная политика

Испания и ЕС - 21 век. Региональная политика Решение экономических задач

Решение экономических задач 3 Инфляция и формы ее проявления

3 Инфляция и формы ее проявления Типы экономических систем

Типы экономических систем Рыночное поведение конкурентных фирм

Рыночное поведение конкурентных фирм Экономика, экономическая теория. Тестовые задания

Экономика, экономическая теория. Тестовые задания Последствия безработицы. Государственная политика поддержки занятости. Понятие экономического роста

Последствия безработицы. Государственная политика поддержки занятости. Понятие экономического роста Предпринимательская деятельность

Предпринимательская деятельность Факторы миграции на примере Брянской области в результате Чернобыльской АЭС

Факторы миграции на примере Брянской области в результате Чернобыльской АЭС Экономические циклы. (Тема 5)

Экономические циклы. (Тема 5) Инвестиционный потенциал Алтайского края

Инвестиционный потенциал Алтайского края Учение Чаянова А.В. О трудовом крестьянском хозяйстве

Учение Чаянова А.В. О трудовом крестьянском хозяйстве Этапы развитии хозяйства РФ

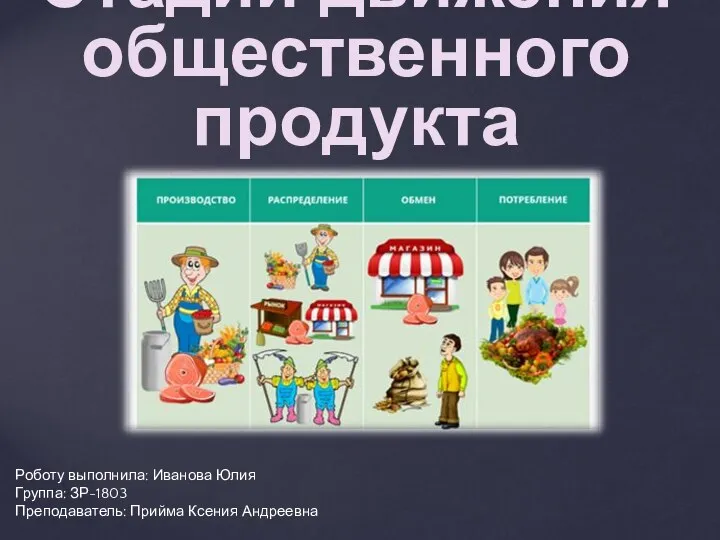

Этапы развитии хозяйства РФ Стадии движения общественного продукта

Стадии движения общественного продукта Хозяйство страны. 8 класс

Хозяйство страны. 8 класс Микроэкономика 1 2021

Микроэкономика 1 2021 Управленческий риск

Управленческий риск Истоки институционализма

Истоки институционализма Использование твердого биотоплива в Германии. Торговля гранулами и брикетами

Использование твердого биотоплива в Германии. Торговля гранулами и брикетами