- BASIC PRINCIPLES OF INTERNATIONAL TAX

Содержание

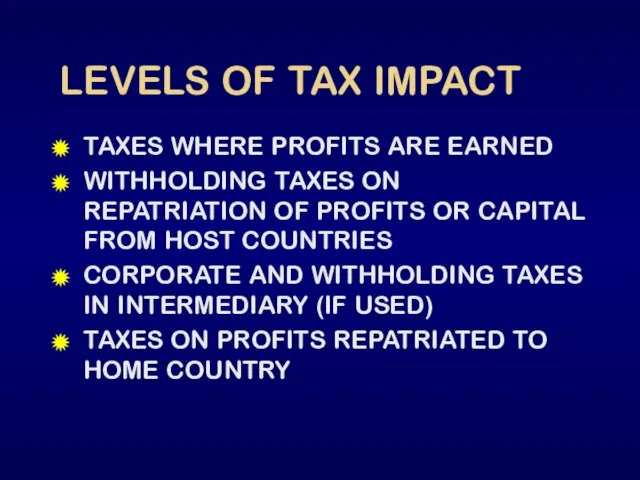

- 2. LEVELS OF TAX IMPACT TAXES WHERE PROFITS ARE EARNED WITHHOLDING TAXES ON REPATRIATION OF PROFITS OR

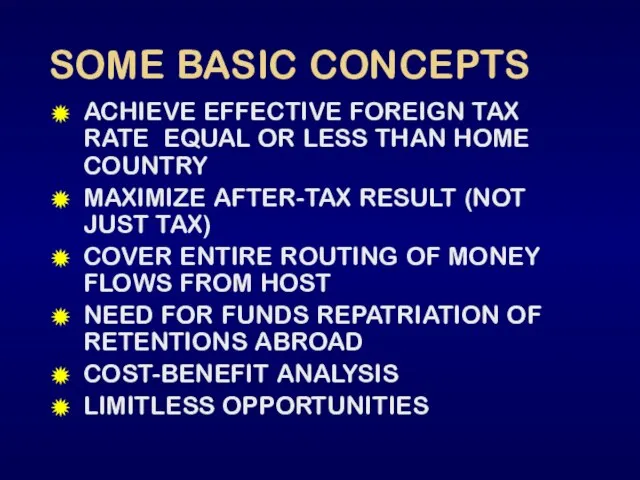

- 3. SOME BASIC CONCEPTS ACHIEVE EFFECTIVE FOREIGN TAX RATE EQUAL OR LESS THAN HOME COUNTRY MAXIMIZE AFTER-TAX

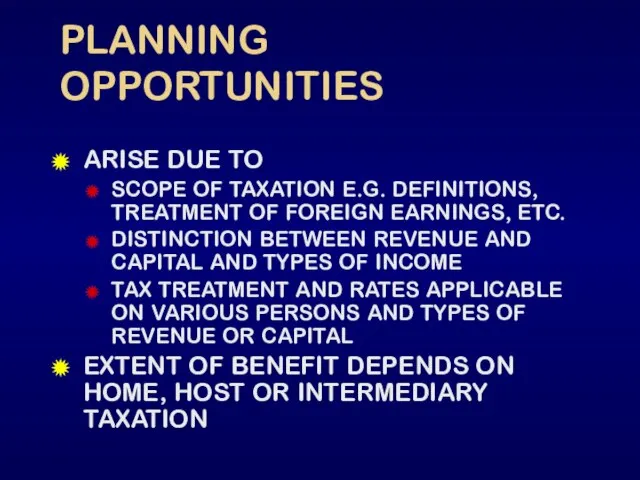

- 4. PLANNING OPPORTUNITIES ARISE DUE TO SCOPE OF TAXATION E.G. DEFINITIONS, TREATMENT OF FOREIGN EARNINGS, ETC. DISTINCTION

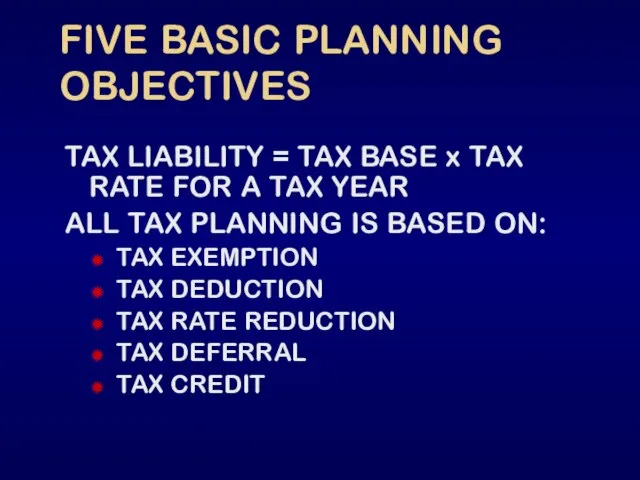

- 5. FIVE BASIC PLANNING OBJECTIVES TAX LIABILITY = TAX BASE x TAX RATE FOR A TAX YEAR

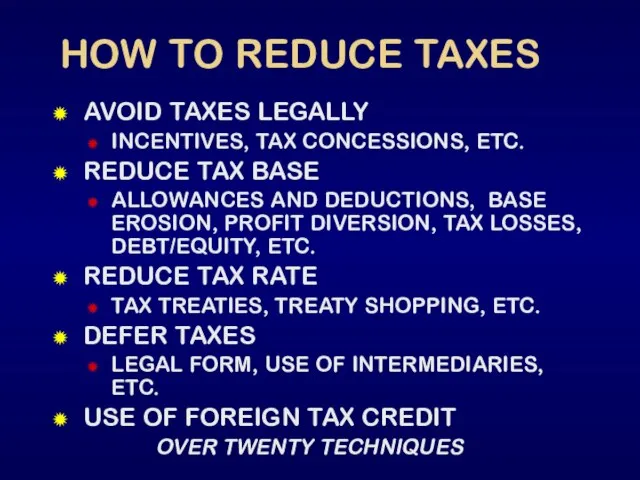

- 6. HOW TO REDUCE TAXES AVOID TAXES LEGALLY INCENTIVES, TAX CONCESSIONS, ETC. REDUCE TAX BASE ALLOWANCES AND

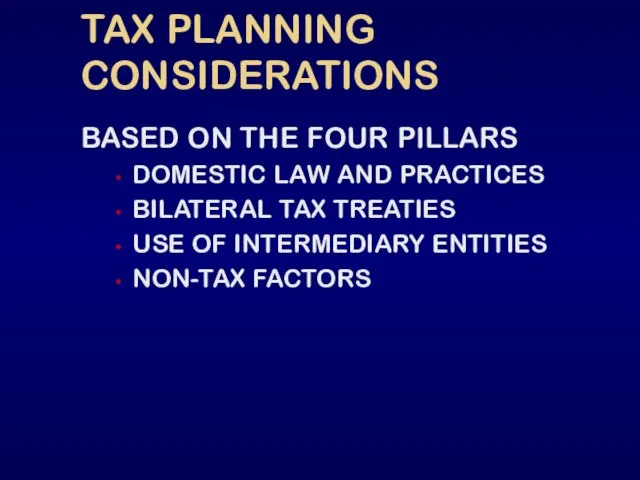

- 7. TAX PLANNING CONSIDERATIONS BASED ON THE FOUR PILLARS DOMESTIC LAW AND PRACTICES BILATERAL TAX TREATIES USE

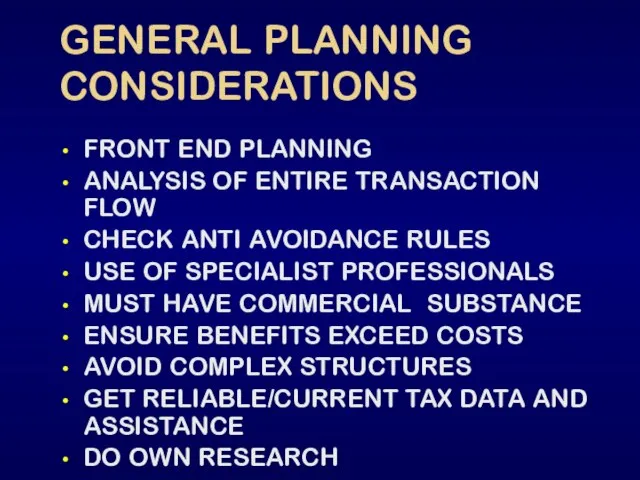

- 8. GENERAL PLANNING CONSIDERATIONS FRONT END PLANNING ANALYSIS OF ENTIRE TRANSACTION FLOW CHECK ANTI AVOIDANCE RULES USE

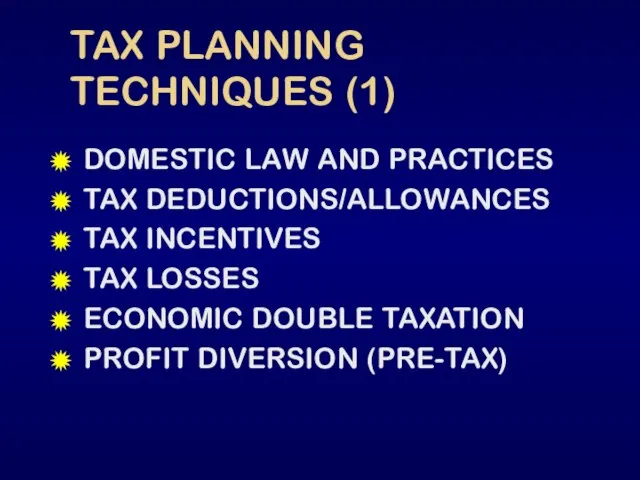

- 9. TAX PLANNING TECHNIQUES (1) DOMESTIC LAW AND PRACTICES TAX DEDUCTIONS/ALLOWANCES TAX INCENTIVES TAX LOSSES ECONOMIC DOUBLE

- 10. TAX PLANNING TECHNIQUES (2) BASE EROSION (PRE-TAX) TAX DEFERRAL FOREIGN TAX CREDITS EXCHANGE RISKS CONNECTING FACTORS

- 11. TAX PLANNING TECHNIQUES (3) TREATY SHOPPING ADVANCE RULINGS TAX ARBITRAGE HOLISTIC PLANNING TAX ADVISORS TAX AVOIDANCE

- 12. A TAX PLANNING METHODOLOGY ANALYZE EXISTING DATA BASE DESIGN TAX PLANNING OPTIONS EVALUATE THE PLAN THE

- 13. A PLANNING APPROACH PLANNING MUST BE HOLISTIC I.E. INCLUDE ENTIRE TRANSACTION FROM HOST TO HOME WITH

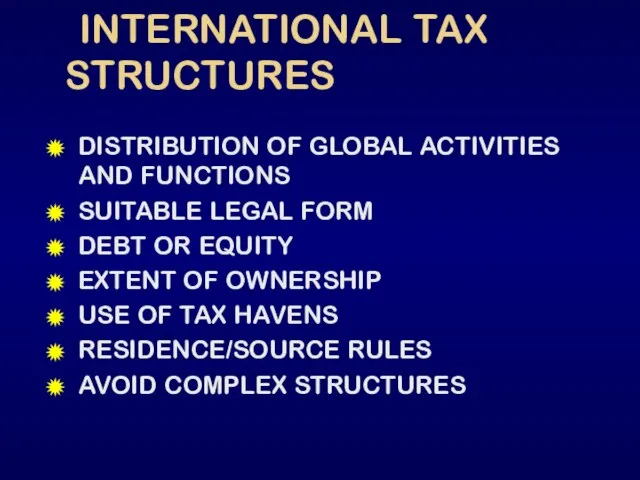

- 14. INTERNATIONAL TAX STRUCTURES DISTRIBUTION OF GLOBAL ACTIVITIES AND FUNCTIONS SUITABLE LEGAL FORM DEBT OR EQUITY EXTENT

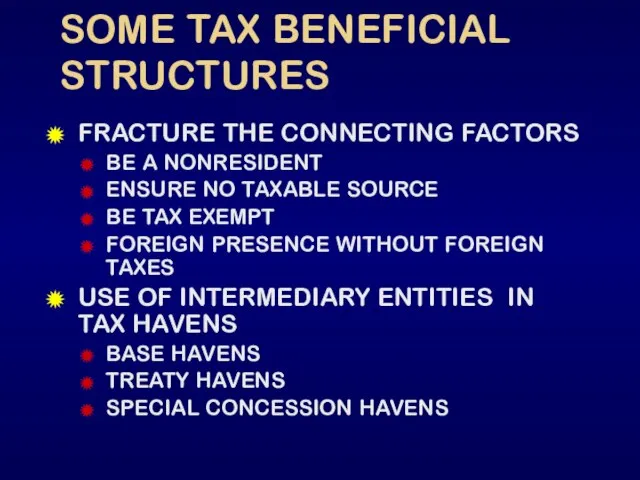

- 15. SOME TAX BENEFICIAL STRUCTURES FRACTURE THE CONNECTING FACTORS BE A NONRESIDENT ENSURE NO TAXABLE SOURCE BE

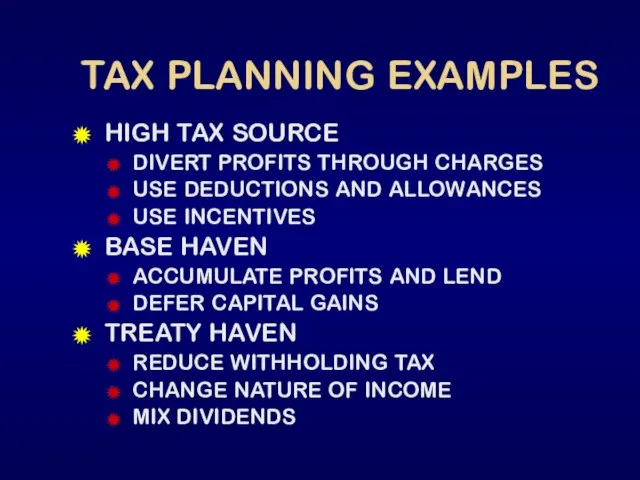

- 16. TAX PLANNING EXAMPLES HIGH TAX SOURCE DIVERT PROFITS THROUGH CHARGES USE DEDUCTIONS AND ALLOWANCES USE INCENTIVES

- 17. INTERNATIONAL TRANSACTIONS INTERNATIONAL TRADE AND FINANCE TRANSFER OF TECHNOLOGY INWARD INVESTMENTS OUTWARD INVESTMENTS MERGERS AND ACQUISITIONS

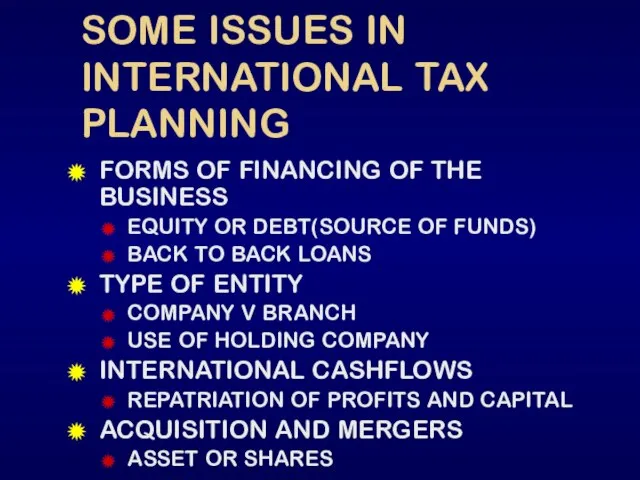

- 18. SOME ISSUES IN INTERNATIONAL TAX PLANNING FORMS OF FINANCING OF THE BUSINESS EQUITY OR DEBT(SOURCE OF

- 19. INTERNATIONAL TAX PLANNING – SOME CONCLUSIONS REQUIRES DETAILED KNOWLEDGE OF LAWS AND PRACTICES COMPLEX BUT FLEXIBLE

- 20. FORM OF LEGAL ENTITY DIRECT SALE AGENCY REPRESENTATIVE OFFICE BRANCH COMPANY SERVICE COMPANY PARTNERSHIP LICENSING OR

- 21. FINANCING OF OVERSEAS ENTITY DEBT OR EQUITY? HYBRIDS? DEBT-EQUITY RATIO IF DEBT - OFFSET AGAINST RELATED

- 22. INTERNATIONAL TAX PLANNING PITFALLS PRACTICAL AND COMMERCIAL CONSIDERATIONS COSTS JURISDICTION CHANGE IN FUTURE NON-TAX FACTORS FRONT-END

- 23. CROSSBORDER TRANSACTIONS INTERNATIONAL TRADE TRANSFER OF TECHNOLOGY CROSSBORDER INVESTMENTS MERGERS AND ACQUISITIONS DISPOSALS OF ASSETS/COMPANY PROFITS/CAPITAL

- 24. TAX PLANNING FOR INDIVIDUALS EXPATRIATES DEPENDENT PERSONAL SERVICES INDEPENDENT PERSONAL SERVICES IMMIGRANT/EMIGRANT OTHERS E.G. HNW OR

- 25. POSSIBILITIES IN TAX PLANNING EXEMPTION PROFIT DIVERSION UPSTREAMING DEDUCTIONS PROFITS EXTRACTION DOWN STREAMING REDUCE THE TAX

- 26. COORDINATION CENTRE EXPENSES (i) PLANNING COORDINATION OF GROUP ACTIVITIES BUDGETARY CONTROL AND FINANCIAL ADVICE ACCOUNTING, AUDITING

- 27. CORDINATION CENTRE EXPENSES (ii) RESEARCH AND DEVELOPMENT ADMINISTER AND PROTECT INTANGIBLES FINANCIAL SERVICES TREASURY MANAGEMENT SUPERVISION

- 28. COORDINATION CENTRE EXPENSES (iii) OTHER SERVICES TRANSPORT MANAGEMENT ADVERTISING ARCHITECTURAL SERVICES QUANTITY SURVEYOR MARKETING

- 29. CONSOLIDATION OF TAX RETURNS LEVEL OF CONSOLIDATION NATIONAL INTERNATIONAL MOVE ASSETS WITHOUT CAPITAL GAINS TAX BALANCE

- 30. METHODS FOR AVOIDING DOUBLE TAX EXEMPTION FULL WITH PROGRESSION CREDIT FULL ORDINARY TAX SPARING INDIRECT DEDUCTION

- 32. Скачать презентацию

Слайд 3SOME BASIC CONCEPTS

ACHIEVE EFFECTIVE FOREIGN TAX RATE EQUAL OR LESS THAN HOME

SOME BASIC CONCEPTS

ACHIEVE EFFECTIVE FOREIGN TAX RATE EQUAL OR LESS THAN HOME

Слайд 4PLANNING OPPORTUNITIES

ARISE DUE TO

SCOPE OF TAXATION E.G. DEFINITIONS, TREATMENT OF FOREIGN EARNINGS,

PLANNING OPPORTUNITIES

ARISE DUE TO

SCOPE OF TAXATION E.G. DEFINITIONS, TREATMENT OF FOREIGN EARNINGS,

Слайд 5FIVE BASIC PLANNING OBJECTIVES

TAX LIABILITY = TAX BASE x TAX RATE FOR

FIVE BASIC PLANNING OBJECTIVES

TAX LIABILITY = TAX BASE x TAX RATE FOR

Слайд 6HOW TO REDUCE TAXES

AVOID TAXES LEGALLY

INCENTIVES, TAX CONCESSIONS, ETC.

REDUCE TAX BASE

ALLOWANCES AND

HOW TO REDUCE TAXES

AVOID TAXES LEGALLY

INCENTIVES, TAX CONCESSIONS, ETC.

REDUCE TAX BASE

ALLOWANCES AND

Слайд 7TAX PLANNING CONSIDERATIONS

BASED ON THE FOUR PILLARS

DOMESTIC LAW AND PRACTICES

BILATERAL TAX TREATIES

USE

TAX PLANNING CONSIDERATIONS

BASED ON THE FOUR PILLARS

DOMESTIC LAW AND PRACTICES

BILATERAL TAX TREATIES

USE

Слайд 8GENERAL PLANNING CONSIDERATIONS

FRONT END PLANNING

ANALYSIS OF ENTIRE TRANSACTION FLOW

CHECK ANTI AVOIDANCE RULES

USE

GENERAL PLANNING CONSIDERATIONS

FRONT END PLANNING

ANALYSIS OF ENTIRE TRANSACTION FLOW

CHECK ANTI AVOIDANCE RULES

USE

Слайд 9TAX PLANNING TECHNIQUES (1)

DOMESTIC LAW AND PRACTICES

TAX DEDUCTIONS/ALLOWANCES

TAX INCENTIVES

TAX LOSSES

ECONOMIC DOUBLE TAXATION

PROFIT

TAX PLANNING TECHNIQUES (1)

DOMESTIC LAW AND PRACTICES

TAX DEDUCTIONS/ALLOWANCES

TAX INCENTIVES

TAX LOSSES

ECONOMIC DOUBLE TAXATION

PROFIT

Слайд 10TAX PLANNING TECHNIQUES (2)

BASE EROSION (PRE-TAX)

TAX DEFERRAL

FOREIGN TAX CREDITS

EXCHANGE RISKS

CONNECTING FACTORS

LEGAL FORM

DEBT

TAX PLANNING TECHNIQUES (2)

BASE EROSION (PRE-TAX)

TAX DEFERRAL

FOREIGN TAX CREDITS

EXCHANGE RISKS

CONNECTING FACTORS

LEGAL FORM

DEBT

Слайд 11TAX PLANNING TECHNIQUES (3)

TREATY SHOPPING

ADVANCE RULINGS

TAX ARBITRAGE

HOLISTIC PLANNING

TAX ADVISORS

TAX AVOIDANCE

EFFECTIVE TAX STRUCTURES

TAX PLANNING TECHNIQUES (3)

TREATY SHOPPING

ADVANCE RULINGS

TAX ARBITRAGE

HOLISTIC PLANNING

TAX ADVISORS

TAX AVOIDANCE

EFFECTIVE TAX STRUCTURES

Слайд 12 A TAX PLANNING METHODOLOGY

ANALYZE EXISTING DATA BASE

DESIGN TAX PLANNING OPTIONS

EVALUATE THE

A TAX PLANNING METHODOLOGY

ANALYZE EXISTING DATA BASE

DESIGN TAX PLANNING OPTIONS

EVALUATE THE

Слайд 13A PLANNING APPROACH

PLANNING MUST BE HOLISTIC I.E. INCLUDE ENTIRE TRANSACTION FROM HOST

A PLANNING APPROACH

PLANNING MUST BE HOLISTIC I.E. INCLUDE ENTIRE TRANSACTION FROM HOST

Слайд 14 INTERNATIONAL TAX STRUCTURES

DISTRIBUTION OF GLOBAL ACTIVITIES AND FUNCTIONS

SUITABLE LEGAL FORM

DEBT

INTERNATIONAL TAX STRUCTURES

DISTRIBUTION OF GLOBAL ACTIVITIES AND FUNCTIONS

SUITABLE LEGAL FORM

DEBT

Слайд 15SOME TAX BENEFICIAL STRUCTURES

FRACTURE THE CONNECTING FACTORS

BE A NONRESIDENT

ENSURE NO TAXABLE SOURCE

BE

SOME TAX BENEFICIAL STRUCTURES

FRACTURE THE CONNECTING FACTORS

BE A NONRESIDENT

ENSURE NO TAXABLE SOURCE

BE

Слайд 16TAX PLANNING EXAMPLES

HIGH TAX SOURCE

DIVERT PROFITS THROUGH CHARGES

USE DEDUCTIONS AND ALLOWANCES

USE INCENTIVES

BASE

TAX PLANNING EXAMPLES

HIGH TAX SOURCE

DIVERT PROFITS THROUGH CHARGES

USE DEDUCTIONS AND ALLOWANCES

USE INCENTIVES

BASE

Слайд 17INTERNATIONAL TRANSACTIONS

INTERNATIONAL TRADE AND FINANCE

TRANSFER OF TECHNOLOGY

INWARD INVESTMENTS

OUTWARD INVESTMENTS

MERGERS AND ACQUISITIONS

DISPOSALS OF

INTERNATIONAL TRANSACTIONS

INTERNATIONAL TRADE AND FINANCE

TRANSFER OF TECHNOLOGY

INWARD INVESTMENTS

OUTWARD INVESTMENTS

MERGERS AND ACQUISITIONS

DISPOSALS OF

Слайд 18SOME ISSUES IN INTERNATIONAL TAX PLANNING

FORMS OF FINANCING OF THE BUSINESS

EQUITY OR

SOME ISSUES IN INTERNATIONAL TAX PLANNING

FORMS OF FINANCING OF THE BUSINESS

EQUITY OR

Слайд 19INTERNATIONAL TAX PLANNING – SOME CONCLUSIONS

REQUIRES DETAILED KNOWLEDGE OF LAWS AND PRACTICES

INTERNATIONAL TAX PLANNING – SOME CONCLUSIONS

REQUIRES DETAILED KNOWLEDGE OF LAWS AND PRACTICES

Слайд 20FORM OF LEGAL ENTITY

DIRECT SALE

AGENCY

REPRESENTATIVE OFFICE

BRANCH

COMPANY

SERVICE COMPANY

PARTNERSHIP

LICENSING OR FRANCHISE

FORM OF LEGAL ENTITY

DIRECT SALE

AGENCY

REPRESENTATIVE OFFICE

BRANCH

COMPANY

SERVICE COMPANY

PARTNERSHIP

LICENSING OR FRANCHISE

Слайд 21FINANCING OF OVERSEAS ENTITY

DEBT OR EQUITY? HYBRIDS?

DEBT-EQUITY RATIO

IF DEBT -

OFFSET AGAINST

FINANCING OF OVERSEAS ENTITY

DEBT OR EQUITY? HYBRIDS?

DEBT-EQUITY RATIO

IF DEBT -

OFFSET AGAINST

Слайд 22INTERNATIONAL TAX PLANNING PITFALLS

PRACTICAL AND COMMERCIAL CONSIDERATIONS

COSTS

JURISDICTION CHANGE IN FUTURE

NON-TAX FACTORS

FRONT-END PLANNING

RELIABLE

INTERNATIONAL TAX PLANNING PITFALLS

PRACTICAL AND COMMERCIAL CONSIDERATIONS

COSTS

JURISDICTION CHANGE IN FUTURE

NON-TAX FACTORS

FRONT-END PLANNING

RELIABLE

Слайд 23CROSSBORDER TRANSACTIONS

INTERNATIONAL TRADE

TRANSFER OF TECHNOLOGY

CROSSBORDER INVESTMENTS

MERGERS AND ACQUISITIONS

DISPOSALS OF ASSETS/COMPANY

PROFITS/CAPITAL REPATRIATION

BRANCH INTO

CROSSBORDER TRANSACTIONS

INTERNATIONAL TRADE

TRANSFER OF TECHNOLOGY

CROSSBORDER INVESTMENTS

MERGERS AND ACQUISITIONS

DISPOSALS OF ASSETS/COMPANY

PROFITS/CAPITAL REPATRIATION

BRANCH INTO

Слайд 24TAX PLANNING FOR INDIVIDUALS

EXPATRIATES

DEPENDENT PERSONAL SERVICES

INDEPENDENT PERSONAL SERVICES

IMMIGRANT/EMIGRANT

OTHERS E.G. HNW OR RETIREES

TAX

TAX PLANNING FOR INDIVIDUALS

EXPATRIATES

DEPENDENT PERSONAL SERVICES

INDEPENDENT PERSONAL SERVICES

IMMIGRANT/EMIGRANT

OTHERS E.G. HNW OR RETIREES

TAX

Слайд 25POSSIBILITIES IN TAX PLANNING

EXEMPTION

PROFIT DIVERSION

UPSTREAMING

DEDUCTIONS

PROFITS EXTRACTION

DOWN STREAMING

REDUCE THE TAX RATE

DEFER THE TAX

POSSIBILITIES IN TAX PLANNING

EXEMPTION

PROFIT DIVERSION

UPSTREAMING

DEDUCTIONS

PROFITS EXTRACTION

DOWN STREAMING

REDUCE THE TAX RATE

DEFER THE TAX

Слайд 26COORDINATION CENTRE EXPENSES (i)

PLANNING

COORDINATION OF GROUP ACTIVITIES

BUDGETARY CONTROL AND FINANCIAL ADVICE

ACCOUNTING, AUDITING

COORDINATION CENTRE EXPENSES (i)

PLANNING

COORDINATION OF GROUP ACTIVITIES

BUDGETARY CONTROL AND FINANCIAL ADVICE

ACCOUNTING, AUDITING

Слайд 27CORDINATION CENTRE EXPENSES (ii)

RESEARCH AND DEVELOPMENT

ADMINISTER AND PROTECT INTANGIBLES

FINANCIAL SERVICES

TREASURY MANAGEMENT

SUPERVISION OF

CORDINATION CENTRE EXPENSES (ii)

RESEARCH AND DEVELOPMENT

ADMINISTER AND PROTECT INTANGIBLES

FINANCIAL SERVICES

TREASURY MANAGEMENT

SUPERVISION OF

Слайд 28COORDINATION CENTRE EXPENSES (iii)

OTHER SERVICES

TRANSPORT

MANAGEMENT

ADVERTISING

ARCHITECTURAL SERVICES

QUANTITY SURVEYOR

MARKETING

COORDINATION CENTRE EXPENSES (iii)

OTHER SERVICES

TRANSPORT

MANAGEMENT

ADVERTISING

ARCHITECTURAL SERVICES

QUANTITY SURVEYOR

MARKETING

Слайд 29CONSOLIDATION OF TAX RETURNS

LEVEL OF CONSOLIDATION

NATIONAL

INTERNATIONAL

MOVE ASSETS WITHOUT CAPITAL GAINS TAX

BALANCE

CONSOLIDATION OF TAX RETURNS

LEVEL OF CONSOLIDATION

NATIONAL

INTERNATIONAL

MOVE ASSETS WITHOUT CAPITAL GAINS TAX

BALANCE

Слайд 30METHODS FOR AVOIDING DOUBLE TAX

EXEMPTION

FULL

WITH PROGRESSION

CREDIT

FULL

ORDINARY

TAX SPARING

INDIRECT

DEDUCTION

TAXABLE INCOME

TAX PAID

METHODS FOR AVOIDING DOUBLE TAX

EXEMPTION

FULL

WITH PROGRESSION

CREDIT

FULL

ORDINARY

TAX SPARING

INDIRECT

DEDUCTION

TAXABLE INCOME

TAX PAID

Конституционно-демократическая партия

Конституционно-демократическая партия Интегрированная система для совместной работыLotus Notes / Domino

Интегрированная система для совместной работыLotus Notes / Domino Предпринимательский риск

Предпринимательский риск Презентация на тему Угарный газ

Презентация на тему Угарный газ  Типология современного урока

Типология современного урока Влияние человечества на эволюцию биосферы. История экологических кризисов.

Влияние человечества на эволюцию биосферы. История экологических кризисов. Ссылки должны работать!

Ссылки должны работать! Этические принципы речевого общения

Этические принципы речевого общения Производство электроэнергии

Производство электроэнергии В. А. Жукуовский

В. А. Жукуовский Проект. Эмоциональный диктант

Проект. Эмоциональный диктант Турецкий Язык. Урок № 1, часть 1. Введение в турецкий язык

Турецкий Язык. Урок № 1, часть 1. Введение в турецкий язык Слуцкий Е. Е. и его вклад в развитие мировой экономики

Слуцкий Е. Е. и его вклад в развитие мировой экономики Интегрированный урок по повести А.С.Пушкина «Метель»

Интегрированный урок по повести А.С.Пушкина «Метель» ЛЕКЦИЯПРЕДСТЕРИЛИЗАЦИОННАЯ ОЧИСТКА ИЗДЕЛИЙ МЕДИЦИНСКОГО НАЗНАЧЕНИЯ И ЕЕ РОЛЬ В ПОДГОТОВКЕ ИЗДЕЛИЙ К СТЕРИЛИЗАЦИИ

ЛЕКЦИЯПРЕДСТЕРИЛИЗАЦИОННАЯ ОЧИСТКА ИЗДЕЛИЙ МЕДИЦИНСКОГО НАЗНАЧЕНИЯ И ЕЕ РОЛЬ В ПОДГОТОВКЕ ИЗДЕЛИЙ К СТЕРИЛИЗАЦИИ Общаемся без конфликтов

Общаемся без конфликтов Пушкин Песнь о вещем Олеге

Пушкин Песнь о вещем Олеге Оздоровительная гимнастика

Оздоровительная гимнастика Медицинский центр Мужское здоровье

Медицинский центр Мужское здоровье Знакомьтесь: фотобанки (микростоки, фотостоки)

Знакомьтесь: фотобанки (микростоки, фотостоки) Соборы, монастыри и скиты на Соловецких острова

Соборы, монастыри и скиты на Соловецких острова Кожа. Надежная защита организма

Кожа. Надежная защита организма Two monument sign panels for Scooter's

Two monument sign panels for Scooter's Организация работы со списками лиц, выходящих на пенсию

Организация работы со списками лиц, выходящих на пенсию Constructions impersonnelles

Constructions impersonnelles Круговорот воды в природе

Круговорот воды в природе Схема. Витебск

Схема. Витебск Экологические проблемы России

Экологические проблемы России