- International Taxation

Содержание

- 2. Cross Border Trade - direct sales from country of residence - via independent sales agent (commissioner)

- 3. Cross Border Investment & Business - equity investment for gain or dividends - debt investments for

- 4. Scope of International Tax Law (M. 1) 1. Domestic legislation covering a. foreign income of residents

- 5. Scope of Our International Tax Studies Treaties and Conventions Practice of States (i.e. domestic law) Intra-Governmental

- 6. INTERNATIONAL ORGANIZATIONS AND TAXATION European Union * council of ministers * commission: - directive proposals -

- 7. What is a Treaty (M. 2) A tax treaty is an agreement between two States to

- 8. Types of DTAs - Bilateral > 3,000 - Multilateral Nordic Tax Convention - Comprehensive (income +

- 9. Interpreting a DTA m. 2 The Vienna Convention on the Law of Treaties. The OECD Commentary.

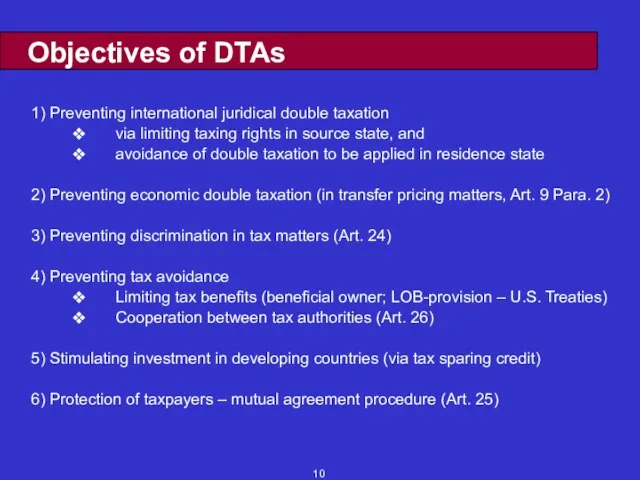

- 10. Objectives of DTAs 1) Preventing international juridical double taxation via limiting taxing rights in source state,

- 11. OECD Model structure Scope (Article 1 and 2) Convention applies to tax resident or one both

- 12. Allocation of rights to tax Taxation of income and capital (Articles 6 to 22): Respective rights

- 13. Source taxation of non-residents Class 1: U n r e s t r i c t

- 14. Source taxation of non-residents Class 3: No t a x a t i o n Business

- 15. DOUBLE TAXATION : Two types Juridical: if one person is taxed twice on same income -

- 16. COMPARISON CLASSICAL SYSTEM FULL IMPUTATION EXEMPTION taxable profit 100 taxable profit 100 taxable profit 100 corporation

- 17. Taxation of dividends from resident companies received by individuals Austria : Mitigated classical; final WHT of

- 18. Taxation of dividends from resident companies received by individuals Norway: : Imputation (full) Portugal : Mitigated

- 19. Terminology Chapter III OECD Model “Shall be taxable only”; exclusive right of residence state. e.g. Art.

- 20. Scope of Tax Treaty Article 1, Persons covered: persons who are residents of one or both

- 21. Partnerships Tax Treatment Treated as a corporate entity (e.g. Spain, Belgium) Consequences: * partners are taxable

- 22. Partnerships (continued) Consequence of different treatment, e.g. partnership in Netherlands : partner residing in Spain: domestic

- 23. Intermediary Use of Convention A. Original Situation No treaty Treaty: WHT 10% No withholding tax on

- 24. Interpretation of Tax Treaties Chapter II OECD Model * Art. 3 OECD Model : Six definitions

- 25. Art. 4, Residence Crucial concept for application of tax treaties * Only residents are entitled to

- 26. Art. 5, Permanent Establishment Art. 7: Business profits shall be taxable only in residence State A

- 27. Art 5, Permanent Establishment Art. 5, § 4: Which activities do not constitute a PE? *

- 28. Art. 5, Permanent Establishment Art. 5, § 5 + 6: Does an agent constitute a PE?

- 29. Electronic Commerce Selling Company X PC Customer PC * Is website a PE of the seller?

- 30. Article 7: Business Profits Country A Company X is non-resident Subsidiary is resident taxpayer in Country

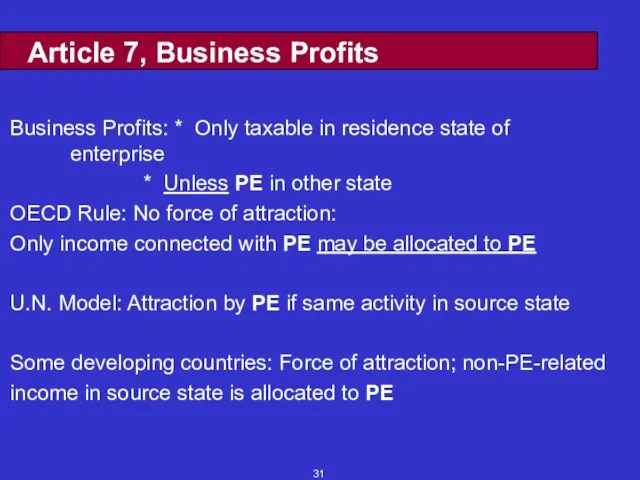

- 31. Article 7, Business Profits Business Profits: * Only taxable in residence state of enterprise * Unless

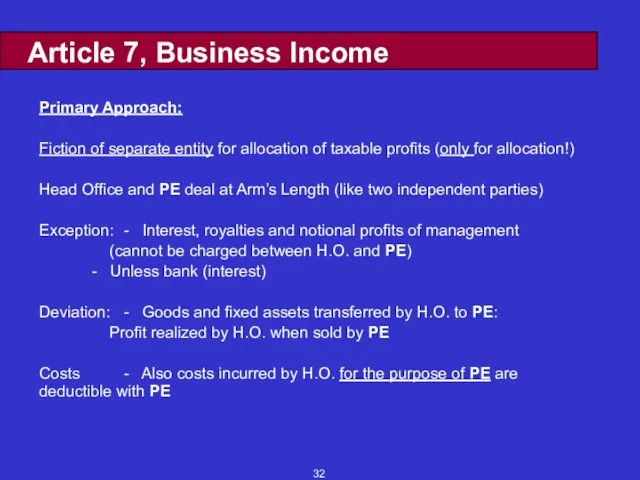

- 32. Article 7, Business Income Primary Approach: Fiction of separate entity for allocation of taxable profits (only

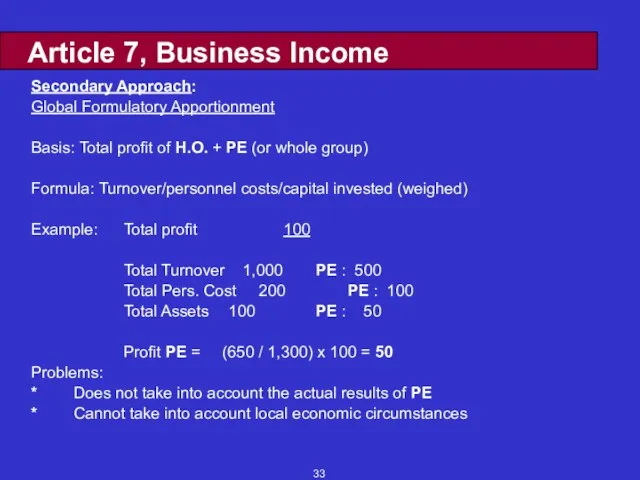

- 33. Article 7, Business Income Secondary Approach: Global Formulatory Apportionment Basis: Total profit of H.O. + PE

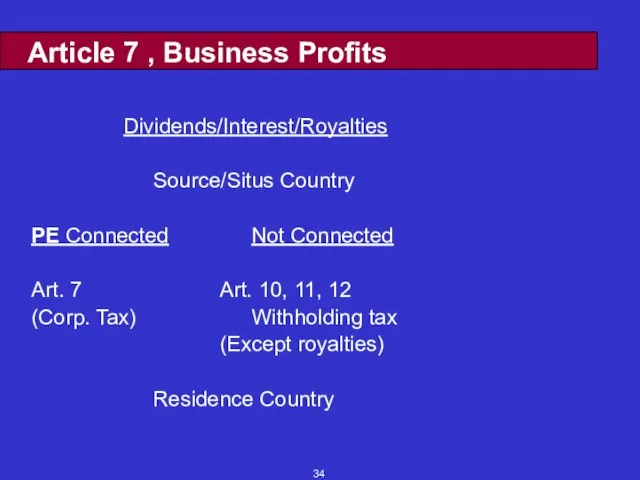

- 34. Article 7 , Business Profits Dividends/Interest/Royalties Source/Situs Country PE Connected Not Connected Art. 7 Art. 10,

- 35. Article 10: Dividends Dividends are profits distributed to shareholders: - officially declared dividends - informal (“constructive”)

- 36. Article 10: Dividends (continued) 4. Only beneficial owner qualifies for reduced withholding tax 5. Note: Art.

- 37. Article 11: Interest Interest is remuneration for money lent Taxable in residence State R of receiver

- 38. Article 12 : Royalties Royalties are payments for use (or right to use) of: -- Copyrights

- 39. Article 15, § 1: Dependent Personal Services - Main rule (§ 1): Salaries, wages and similar

- 40. Article 15, § 2: Dependent Personal Services - Article 15 (§ 2) exception to main rule:

- 41. Article 18: Pensions Private pensions and other similar remuneration for past employment taxable only in State

- 42. Article 21: Other Income Sweeping-up clause: all income not dealt with in the previous articles taxable

- 43. Article 23a: Exemption Method Without Progression: Net “world” income 100,000 Exempt foreign income 40,000 Net domestic

- 44. Article 23b: Credit Method Full Credit: Net “world” income 100,000 Domestic tax 30% 30,000 Foreign tax

- 45. Tax Sparing Credit * included in many treaties between developing and developed countries (not USA) *

- 46. Article 24: Non-discrimination Forbidden: More burdensome treatment of nationals of the other State (§ 1) if

- 47. Article 25: Mutual Agreement Procedure Taxation not in accordance with provisions of convention: * resident may

- 48. Article 26: Exchange of Information 1 Increasing number of international transactions underlines importance of cooperation between

- 49. Article 26: Exchange of Information 2 Forms of Exchange More Recently automatic - simultaneous investigations spontaneous

- 50. European Tax Law Parent-Subsidiary Directive Purpose: avoiding double taxation on profits distributed within EU: no other

- 51. European Tax Law Parent-Subsidiary Directive Qualifying payments: "distribution of profits" (Art. 1, 4 and 5) -

- 52. European Tax Law Parent-Subsidiary Directive Dividends received: 1) exemption method (dividend not included in taxable income):

- 53. European Tax Law Parent-subsidiary directive Dividends paid: - 25% holding requirement (lower threshold allowed) (Art. 5)

- 54. European Tax Law Merger directive Purpose: - to postpone taxation on capital gains, normally realised with

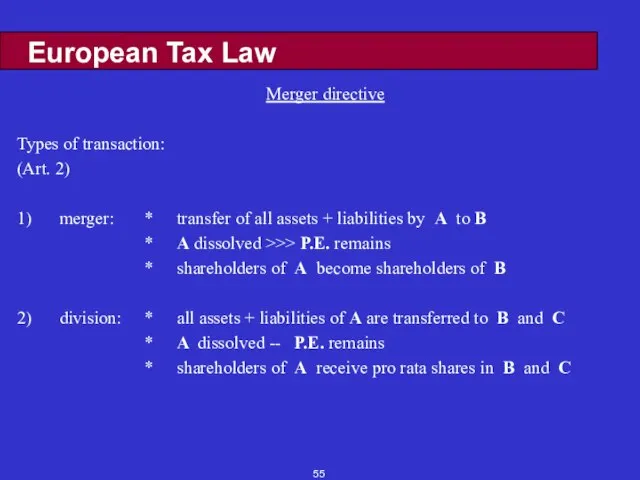

- 55. European Tax Law Merger directive Types of transaction: (Art. 2) 1) merger: * transfer of all

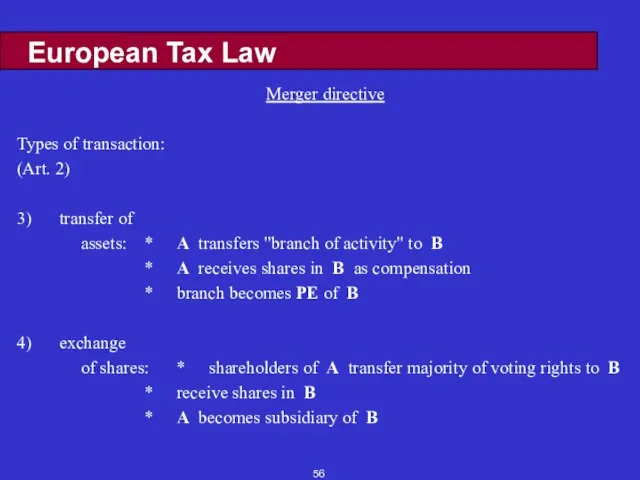

- 56. European Tax Law Merger directive Types of transaction: (Art. 2) 3) transfer of assets: * A

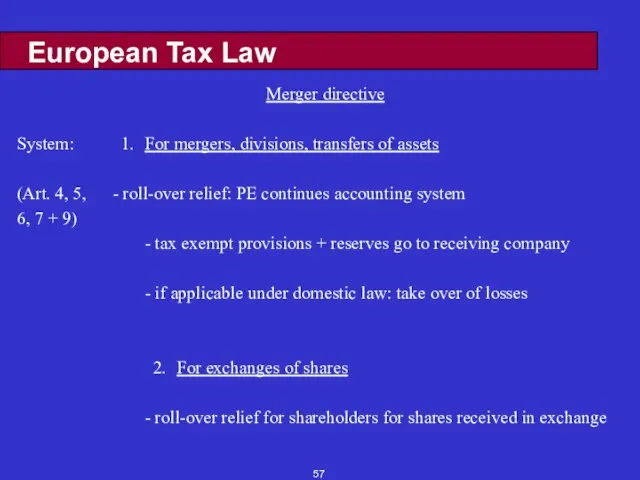

- 57. European Tax Law Merger directive System: 1. For mergers, divisions, transfers of assets (Art. 4, 5,

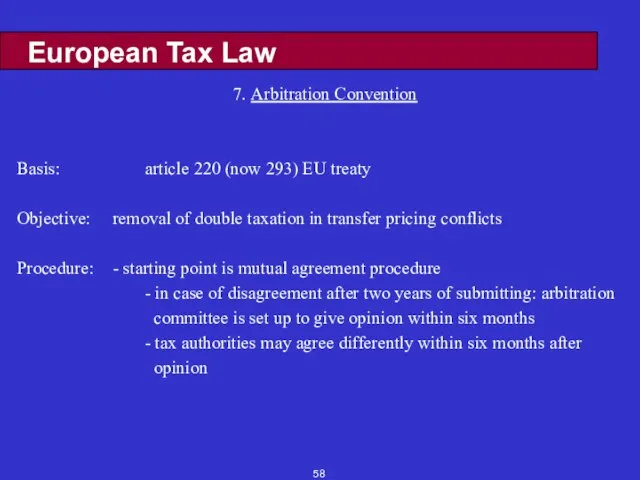

- 58. European Tax Law 7. Arbitration Convention Basis: article 220 (now 293) EU treaty Objective: removal of

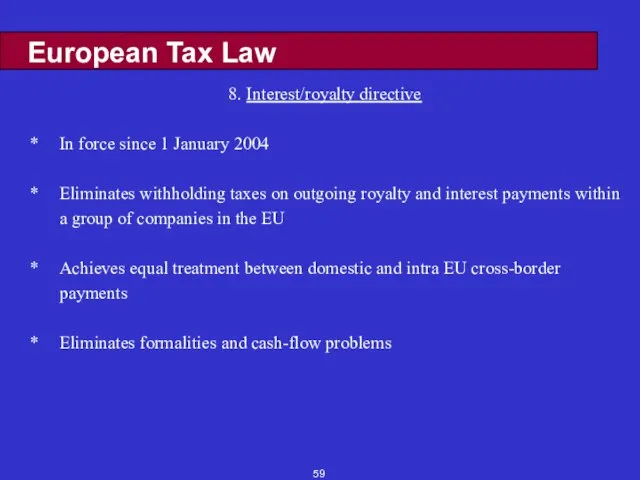

- 59. European Tax Law 8. Interest/royalty directive * In force since 1 January 2004 * Eliminates withholding

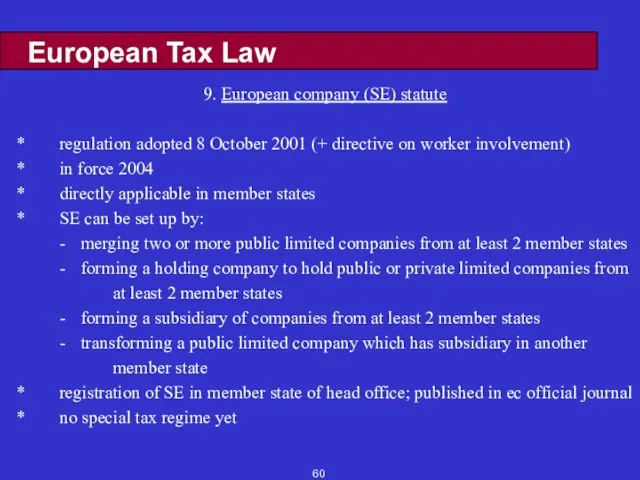

- 60. European Tax Law 9. European company (SE) statute * regulation adopted 8 October 2001 (+ directive

- 62. Скачать презентацию

Слайд 3Cross Border Investment & Business

- equity investment for gain or dividends

- debt investments

Cross Border Investment & Business

- equity investment for gain or dividends

- debt investments

Слайд 4Scope of International Tax Law (M. 1)

1. Domestic legislation covering

a. foreign income of residents

Scope of International Tax Law (M. 1)

1. Domestic legislation covering

a. foreign income of residents

Слайд 5Scope of Our International Tax Studies

Treaties and Conventions

Practice of States (i.e. domestic

Scope of Our International Tax Studies

Treaties and Conventions

Practice of States (i.e. domestic

Слайд 6INTERNATIONAL ORGANIZATIONS AND TAXATION

European Union * council of ministers

* commission: - directive proposals

- actions

INTERNATIONAL ORGANIZATIONS AND TAXATION

European Union * council of ministers

* commission: - directive proposals

- actions

Слайд 7What is a Treaty (M. 2)

A tax treaty is an agreement between

What is a Treaty (M. 2)

A tax treaty is an agreement between

Слайд 8Types of DTAs

- Bilateral > 3,000

- Multilateral Nordic Tax Convention

- Comprehensive (income + capital)

Limited inheritance and gift tax

TIEA

- Non-tax -

Types of DTAs

- Bilateral > 3,000

- Multilateral Nordic Tax Convention

- Comprehensive (income + capital)

Limited inheritance and gift tax

TIEA

- Non-tax -

Слайд 9Interpreting a DTA m. 2

The Vienna Convention on the Law of Treaties.

The

Interpreting a DTA m. 2

The Vienna Convention on the Law of Treaties.

The

Слайд 10Objectives of DTAs

1) Preventing international juridical double taxation

via limiting taxing rights in

Objectives of DTAs

1) Preventing international juridical double taxation

via limiting taxing rights in

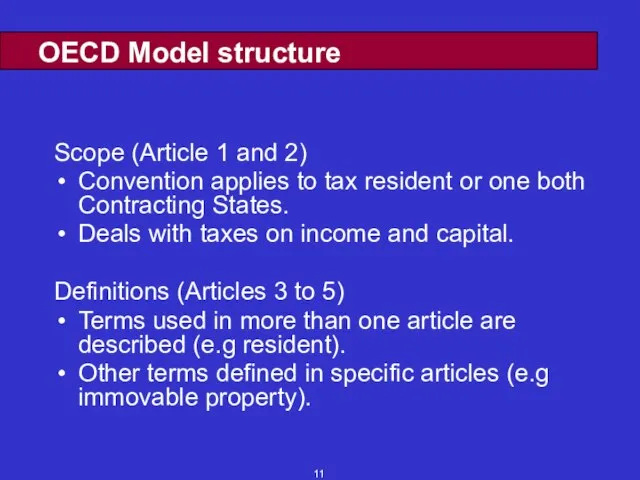

Слайд 11OECD Model structure

Scope (Article 1 and 2)

Convention applies to tax resident or

OECD Model structure

Scope (Article 1 and 2)

Convention applies to tax resident or

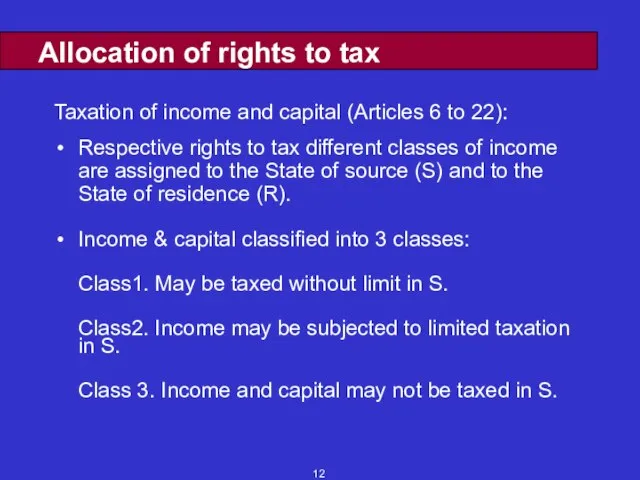

Слайд 12Allocation of rights to tax

Taxation of income and capital (Articles 6 to

Allocation of rights to tax

Taxation of income and capital (Articles 6 to

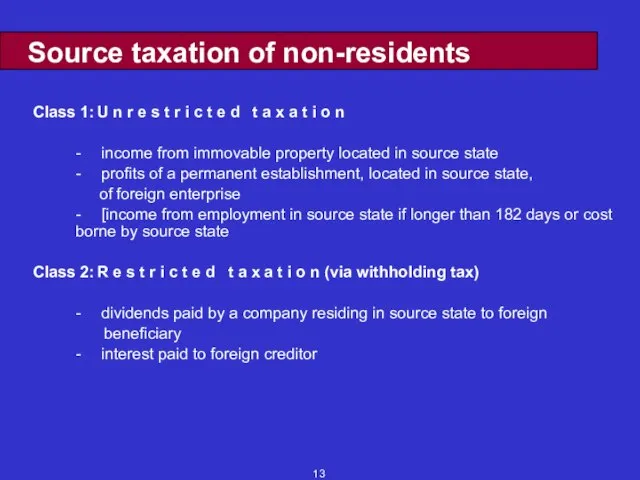

Слайд 13Source taxation of non-residents

Class 1: U n r e s t r i

Source taxation of non-residents

Class 1: U n r e s t r i

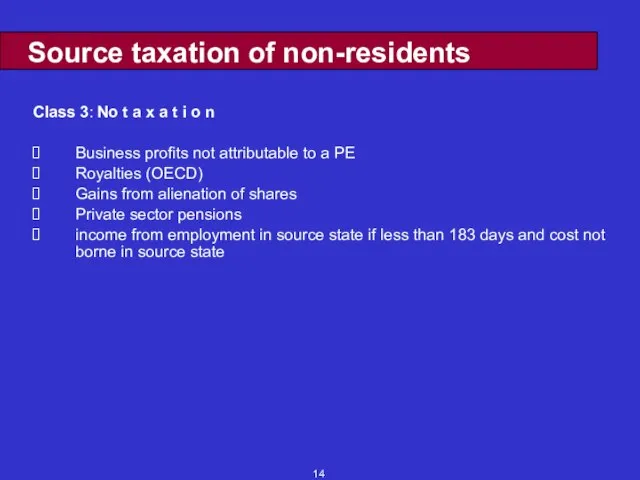

Слайд 14Source taxation of non-residents

Class 3: No t a x a t i o

Source taxation of non-residents

Class 3: No t a x a t i o

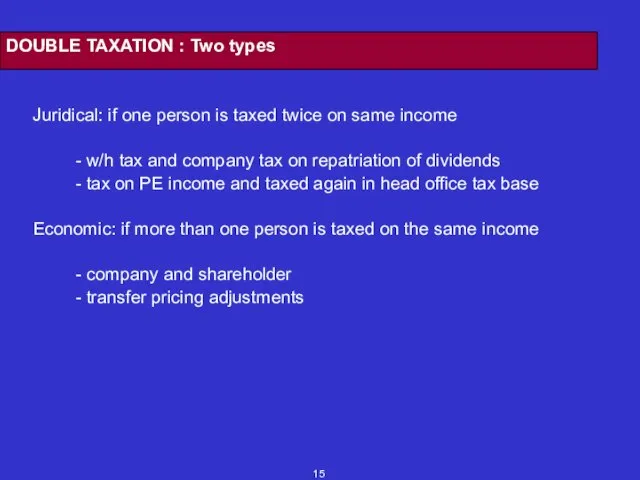

Слайд 15DOUBLE TAXATION : Two types

Juridical: if one person is taxed twice on

DOUBLE TAXATION : Two types

Juridical: if one person is taxed twice on

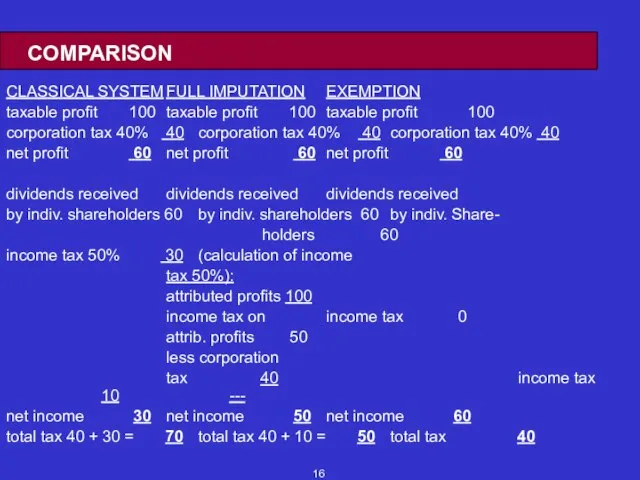

Слайд 16COMPARISON

CLASSICAL SYSTEM FULL IMPUTATION EXEMPTION

taxable profit 100 taxable profit 100 taxable profit 100

corporation tax 40% 40 corporation

COMPARISON

CLASSICAL SYSTEM FULL IMPUTATION EXEMPTION

taxable profit 100 taxable profit 100 taxable profit 100

corporation tax 40% 40 corporation

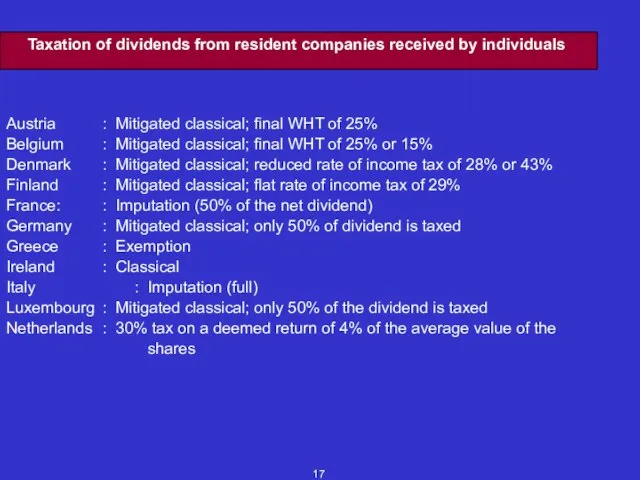

Слайд 17Taxation of dividends from resident companies received by individuals

Austria : Mitigated classical; final

Taxation of dividends from resident companies received by individuals

Austria : Mitigated classical; final

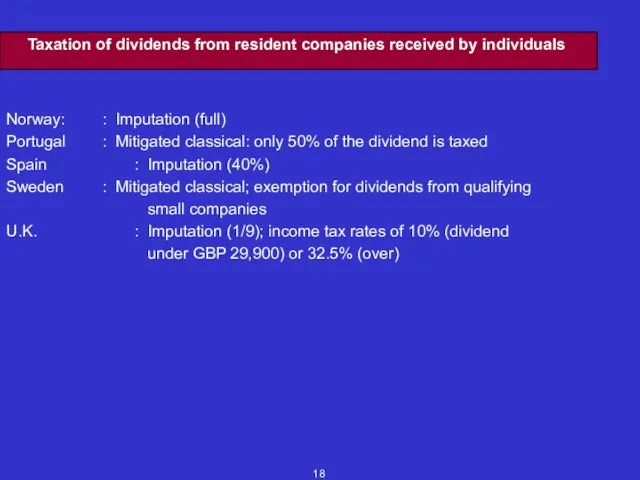

Слайд 18Taxation of dividends from resident companies received by individuals

Norway: : Imputation (full)

Portugal : Mitigated

Taxation of dividends from resident companies received by individuals

Norway: : Imputation (full)

Portugal : Mitigated

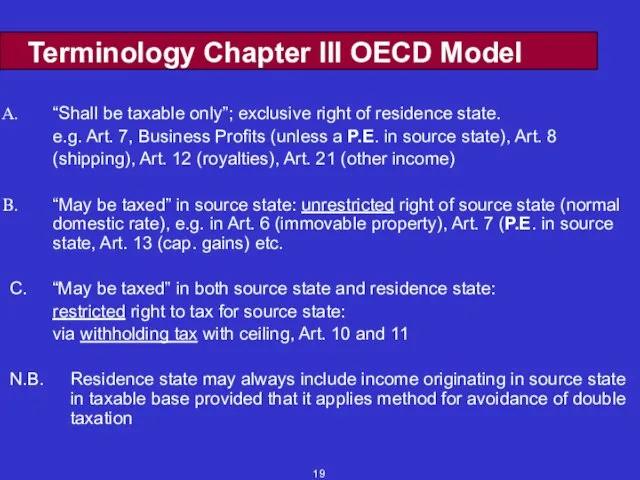

Слайд 19Terminology Chapter III OECD Model

“Shall be taxable only”; exclusive right of residence

Terminology Chapter III OECD Model

“Shall be taxable only”; exclusive right of residence

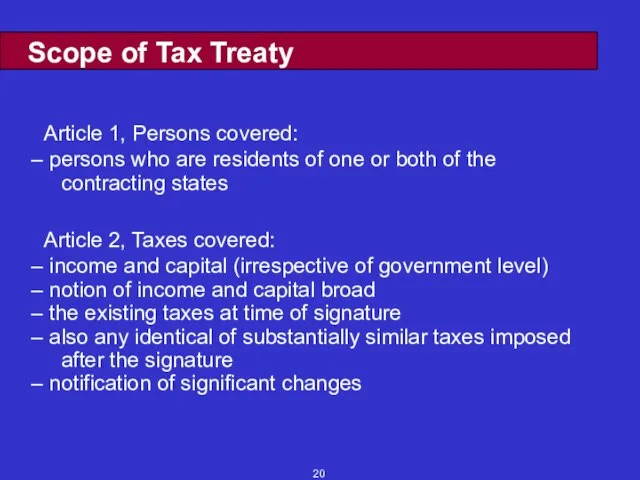

Слайд 20Scope of Tax Treaty

Article 1, Persons covered:

persons who are residents of

Scope of Tax Treaty

Article 1, Persons covered:

persons who are residents of

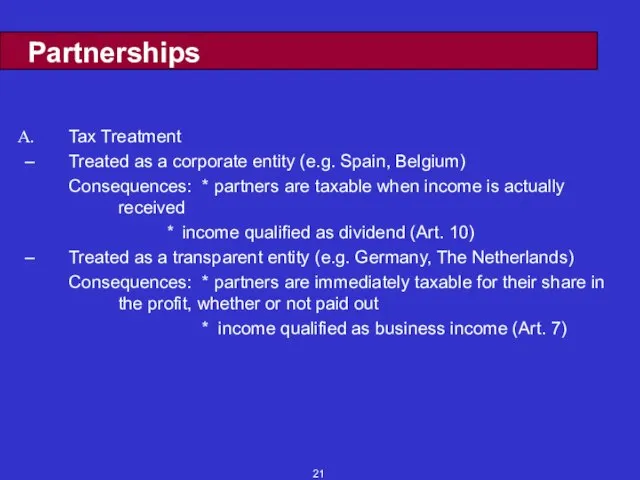

Слайд 21Partnerships

Tax Treatment

Treated as a corporate entity (e.g. Spain, Belgium)

Consequences: * partners are taxable

Partnerships

Tax Treatment

Treated as a corporate entity (e.g. Spain, Belgium)

Consequences: * partners are taxable

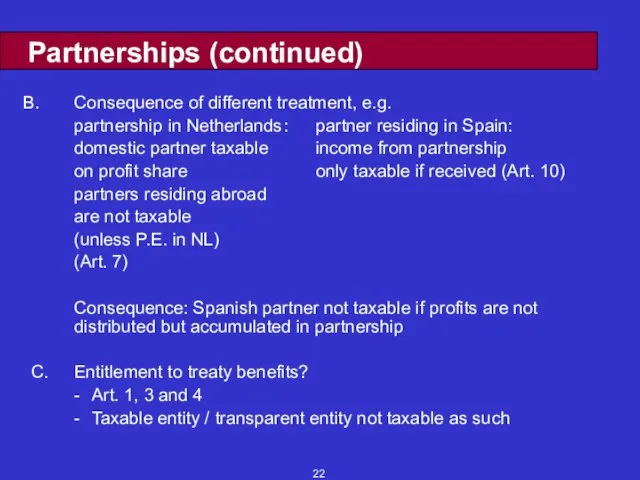

Слайд 22Partnerships (continued)

Consequence of different treatment, e.g.

partnership in Netherlands : partner residing in Spain:

domestic

Partnerships (continued)

Consequence of different treatment, e.g.

partnership in Netherlands : partner residing in Spain:

domestic

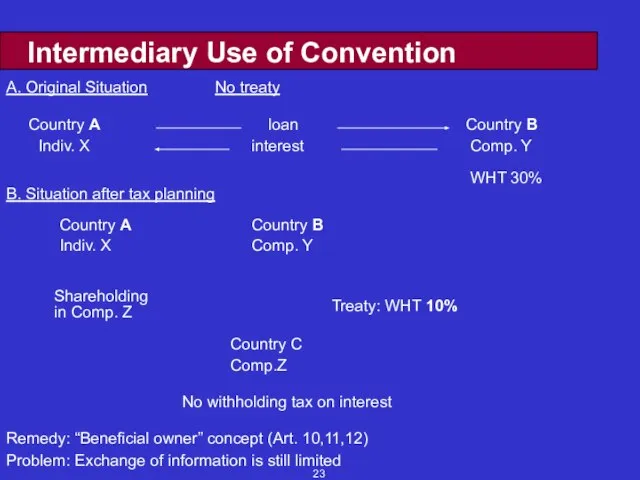

Слайд 23Intermediary Use of Convention

A. Original Situation No treaty

Treaty: WHT 10%

No withholding tax

Intermediary Use of Convention

A. Original Situation No treaty

Treaty: WHT 10%

No withholding tax

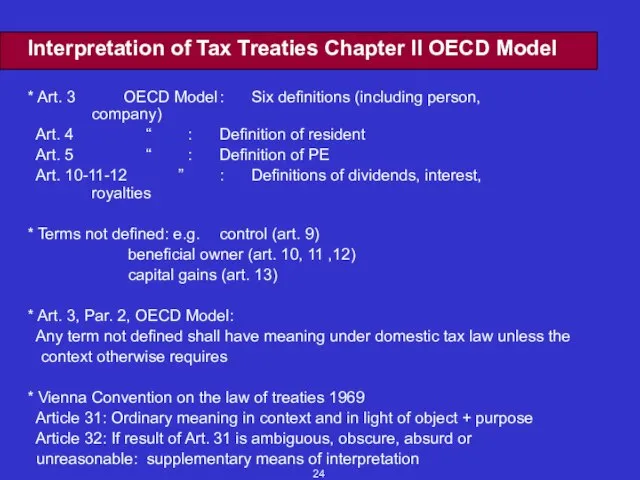

Слайд 24Interpretation of Tax Treaties Chapter II OECD Model

* Art. 3 OECD Model : Six definitions

Interpretation of Tax Treaties Chapter II OECD Model

* Art. 3 OECD Model : Six definitions

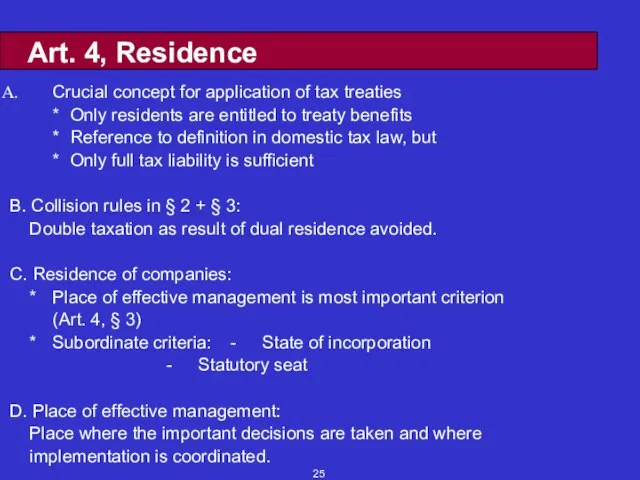

Слайд 25Art. 4, Residence

Crucial concept for application of tax treaties

* Only residents are entitled

Art. 4, Residence

Crucial concept for application of tax treaties

* Only residents are entitled

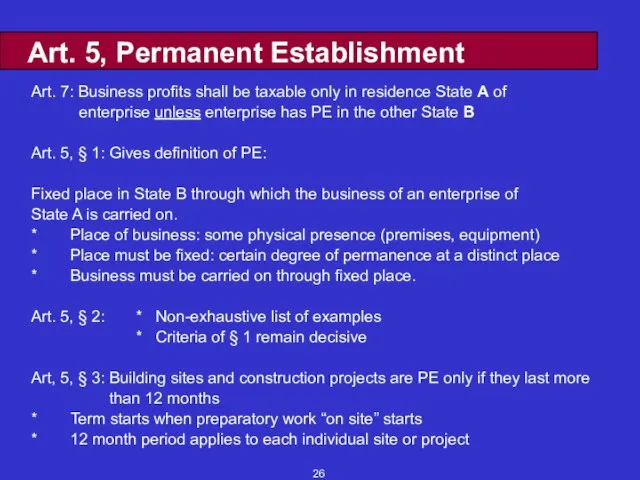

Слайд 26Art. 5, Permanent Establishment

Art. 7: Business profits shall be taxable only in

Art. 5, Permanent Establishment

Art. 7: Business profits shall be taxable only in

Слайд 27Art 5, Permanent Establishment

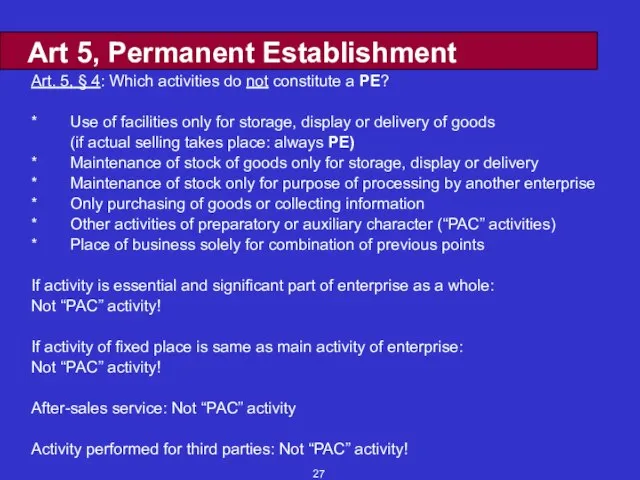

Art. 5, § 4: Which activities do not constitute

Art 5, Permanent Establishment

Art. 5, § 4: Which activities do not constitute

Слайд 28Art. 5, Permanent Establishment

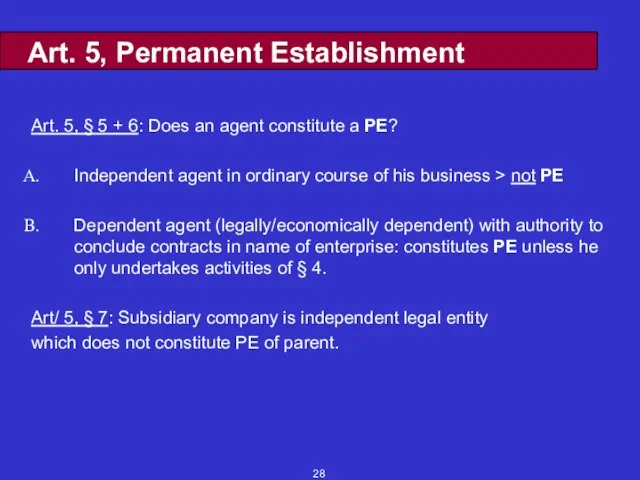

Art. 5, § 5 + 6: Does an agent

Art. 5, Permanent Establishment

Art. 5, § 5 + 6: Does an agent

Слайд 29Electronic Commerce

Selling

Company X

PC

Customer PC

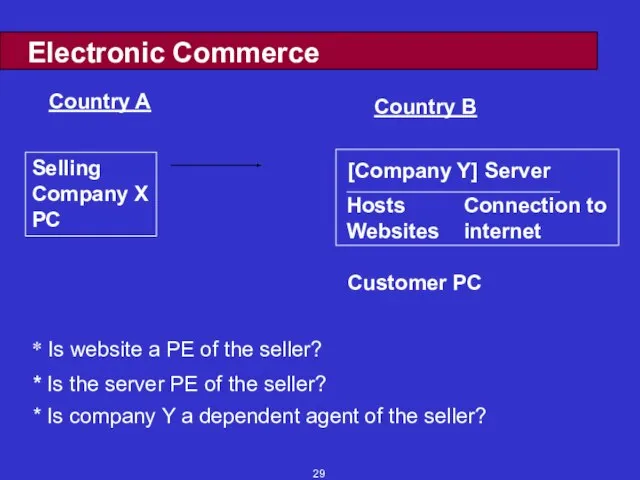

* Is website a PE of the seller?

* Is

Electronic Commerce

Selling

Company X

PC

Customer PC

* Is website a PE of the seller?

* Is

Слайд 30Article 7: Business Profits

Country A

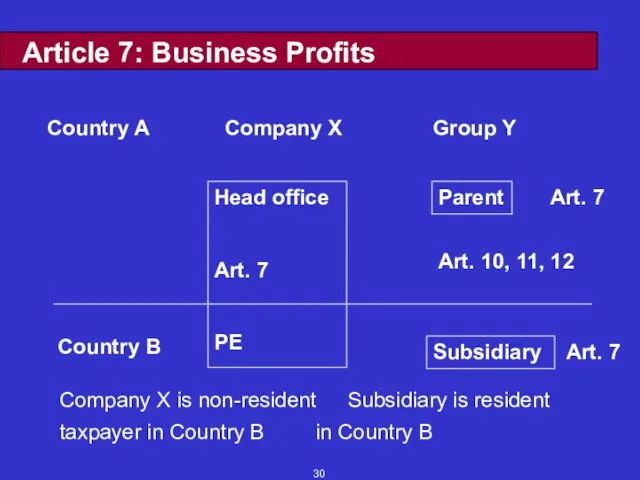

Company X is non-resident Subsidiary is resident

taxpayer in Country

Article 7: Business Profits

Country A

Company X is non-resident Subsidiary is resident

taxpayer in Country

Слайд 31Article 7, Business Profits

Business Profits: * Only taxable in residence state of

Article 7, Business Profits

Business Profits: * Only taxable in residence state of

Слайд 32Article 7, Business Income

Primary Approach:

Fiction of separate entity for allocation of taxable

Article 7, Business Income

Primary Approach:

Fiction of separate entity for allocation of taxable

Слайд 33Article 7, Business Income

Secondary Approach:

Global Formulatory Apportionment

Basis: Total profit of H.O. +

Article 7, Business Income

Secondary Approach:

Global Formulatory Apportionment

Basis: Total profit of H.O. +

Слайд 34Article 7 , Business Profits

Dividends/Interest/Royalties

Source/Situs Country

PE Connected Not Connected

Art. 7 Art. 10, 11,

Article 7 , Business Profits

Dividends/Interest/Royalties

Source/Situs Country

PE Connected Not Connected

Art. 7 Art. 10, 11,

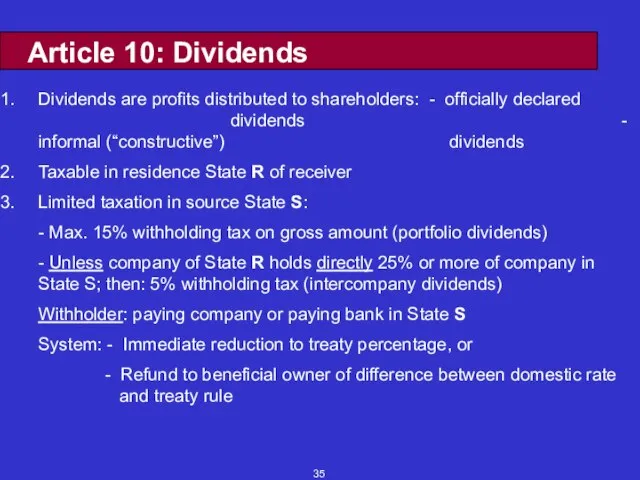

Слайд 35Article 10: Dividends

Dividends are profits distributed to shareholders: - officially declared dividends

Article 10: Dividends

Dividends are profits distributed to shareholders: - officially declared dividends

Слайд 36Article 10: Dividends (continued)

4. Only beneficial owner qualifies for reduced withholding tax

5.

Article 10: Dividends (continued)

4. Only beneficial owner qualifies for reduced withholding tax

5.

Слайд 37Article 11: Interest

Interest is remuneration for money lent

Taxable in residence State R

Article 11: Interest

Interest is remuneration for money lent

Taxable in residence State R

Слайд 38Article 12 : Royalties

Royalties are payments for use (or right to use)

Article 12 : Royalties

Royalties are payments for use (or right to use)

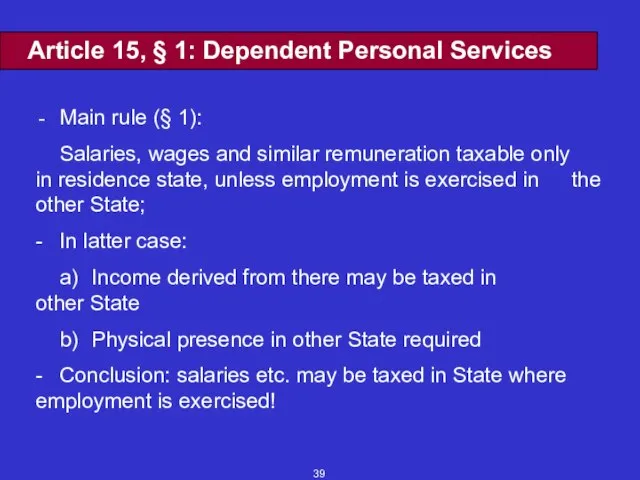

Слайд 39Article 15, § 1: Dependent Personal Services

- Main rule (§ 1):

Salaries, wages

Article 15, § 1: Dependent Personal Services

- Main rule (§ 1):

Salaries, wages

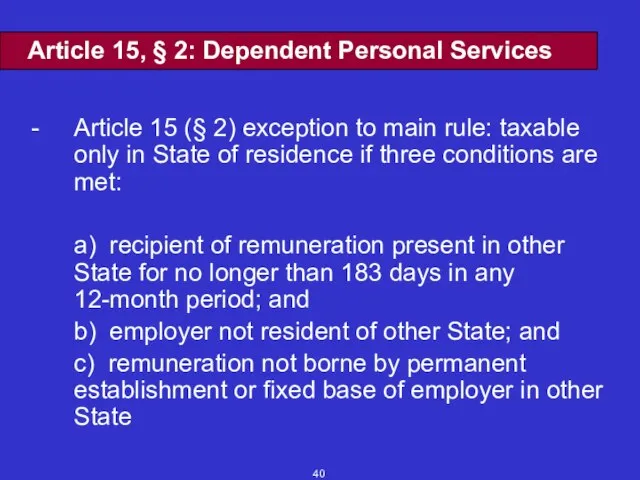

Слайд 40Article 15, § 2: Dependent Personal Services

- Article 15 (§ 2) exception to

Article 15, § 2: Dependent Personal Services

- Article 15 (§ 2) exception to

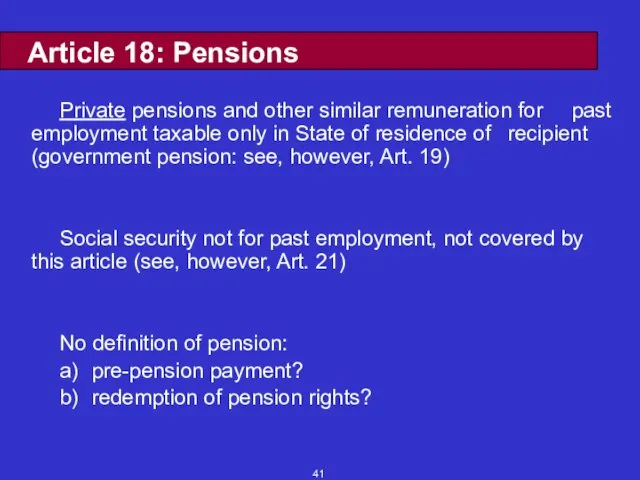

Слайд 41Article 18: Pensions

Private pensions and other similar remuneration for past employment taxable

Article 18: Pensions

Private pensions and other similar remuneration for past employment taxable

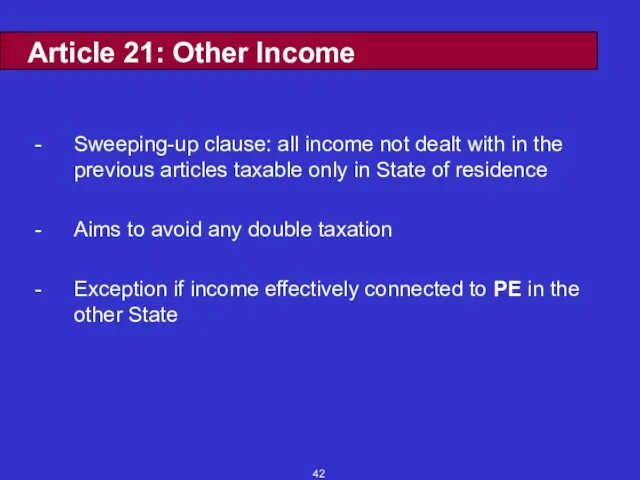

Слайд 42Article 21: Other Income

Sweeping-up clause: all income not dealt with in the

Article 21: Other Income

Sweeping-up clause: all income not dealt with in the

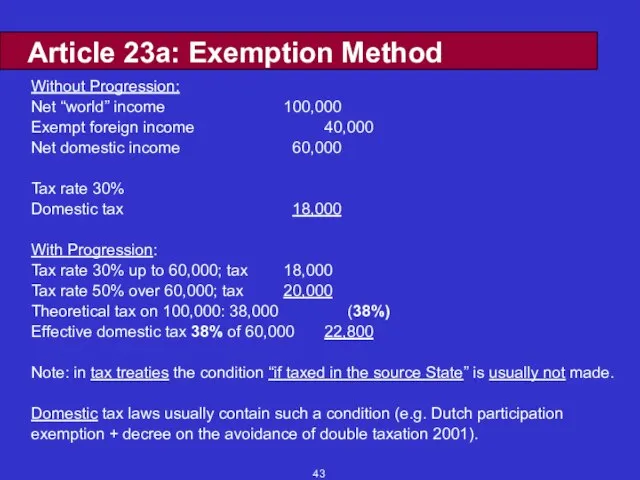

Слайд 43Article 23a: Exemption Method

Without Progression:

Net “world” income 100,000

Exempt foreign income 40,000

Net domestic income

Article 23a: Exemption Method

Without Progression:

Net “world” income 100,000

Exempt foreign income 40,000

Net domestic income

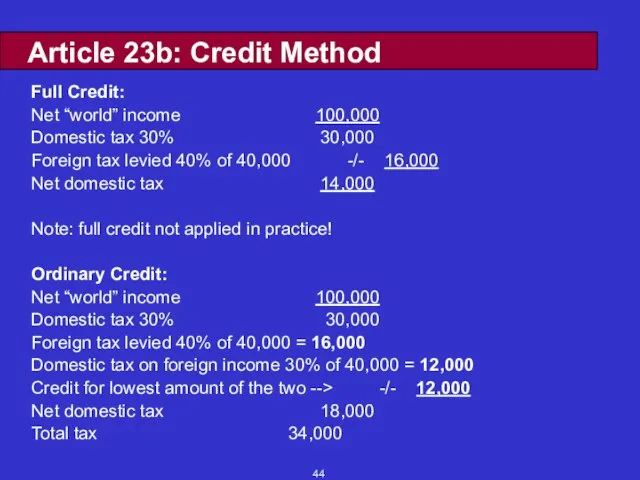

Слайд 44Article 23b: Credit Method

Full Credit:

Net “world” income 100,000

Domestic tax 30% 30,000

Foreign tax levied

Article 23b: Credit Method

Full Credit:

Net “world” income 100,000

Domestic tax 30% 30,000

Foreign tax levied

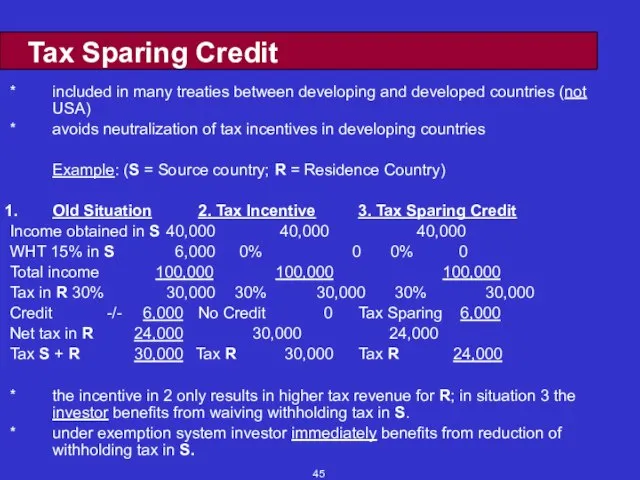

Слайд 45Tax Sparing Credit

* included in many treaties between developing and developed countries (not

Tax Sparing Credit

* included in many treaties between developing and developed countries (not

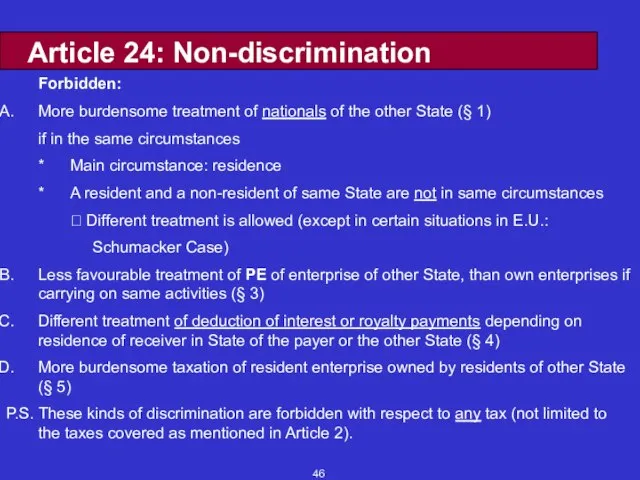

Слайд 46Article 24: Non-discrimination

Forbidden:

More burdensome treatment of nationals of the other State (§

Article 24: Non-discrimination

Forbidden:

More burdensome treatment of nationals of the other State (§

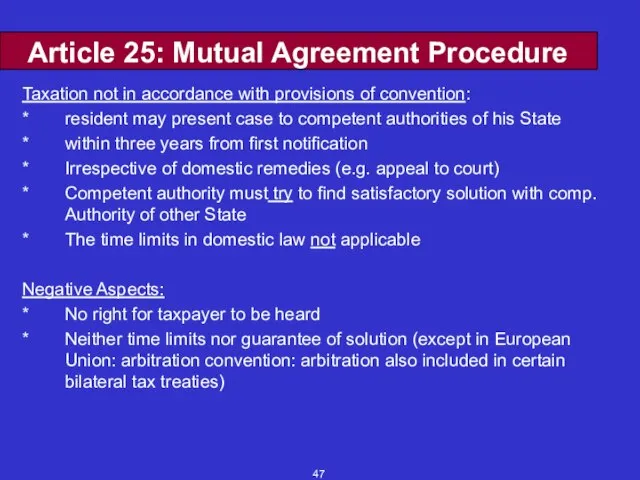

Слайд 47Article 25: Mutual Agreement Procedure

Taxation not in accordance with provisions of convention:

* resident

Article 25: Mutual Agreement Procedure

Taxation not in accordance with provisions of convention:

* resident

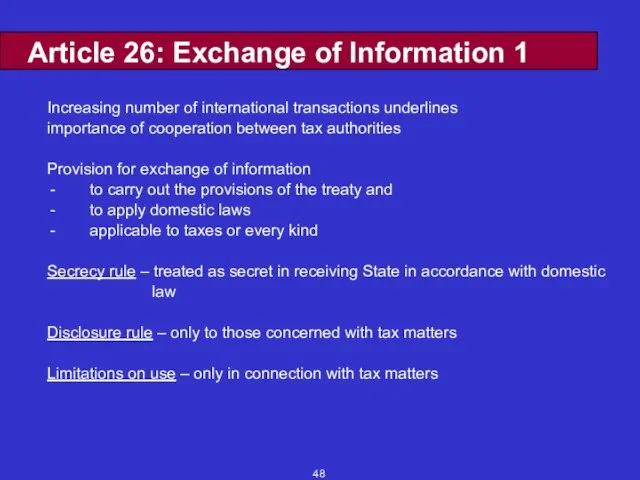

Слайд 48Article 26: Exchange of Information 1

Increasing number of international transactions underlines

importance of

Article 26: Exchange of Information 1

Increasing number of international transactions underlines

importance of

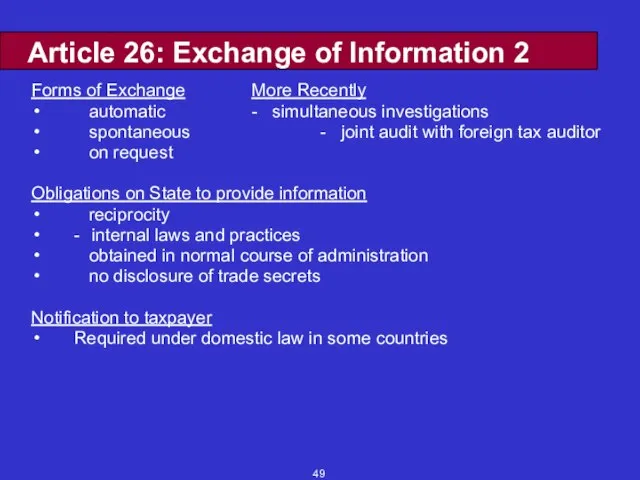

Слайд 49Article 26: Exchange of Information 2

Forms of Exchange More Recently

automatic - simultaneous investigations

Article 26: Exchange of Information 2

Forms of Exchange More Recently

automatic - simultaneous investigations

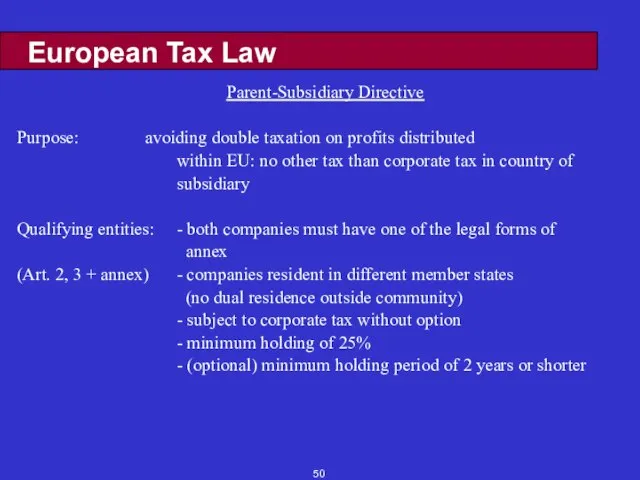

Слайд 50European Tax Law

Parent-Subsidiary Directive

Purpose: avoiding double taxation on profits distributed

within EU: no

European Tax Law

Parent-Subsidiary Directive

Purpose: avoiding double taxation on profits distributed

within EU: no

Слайд 51European Tax Law

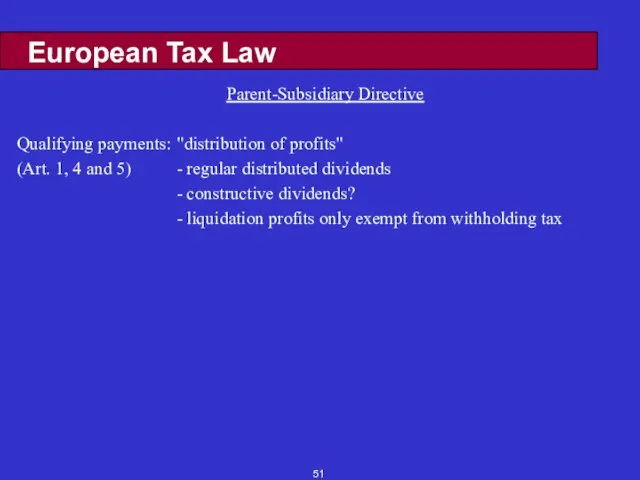

Parent-Subsidiary Directive

Qualifying payments: "distribution of profits"

(Art. 1, 4 and 5) - regular

European Tax Law

Parent-Subsidiary Directive

Qualifying payments: "distribution of profits"

(Art. 1, 4 and 5) - regular

Слайд 52European Tax Law

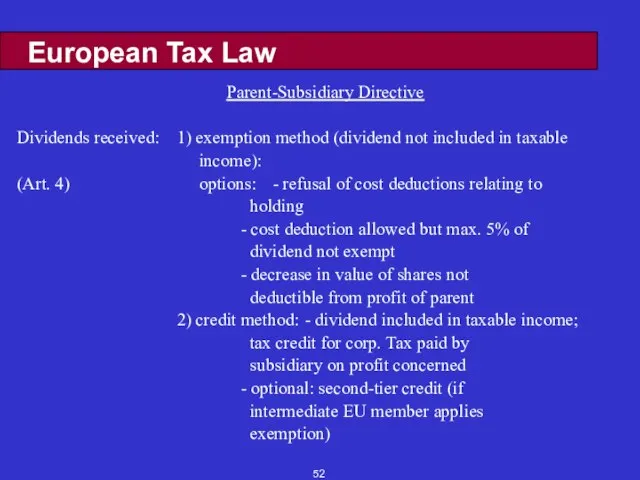

Parent-Subsidiary Directive

Dividends received: 1) exemption method (dividend not included in

European Tax Law

Parent-Subsidiary Directive

Dividends received: 1) exemption method (dividend not included in

Слайд 53European Tax Law

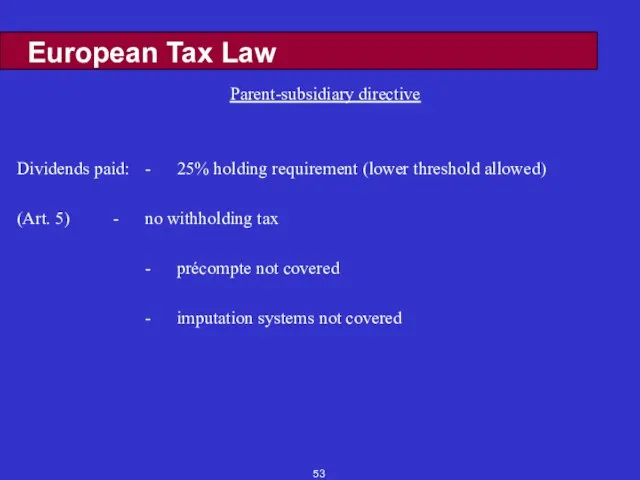

Parent-subsidiary directive

Dividends paid: - 25% holding requirement (lower threshold allowed)

(Art. 5) - no withholding

European Tax Law

Parent-subsidiary directive

Dividends paid: - 25% holding requirement (lower threshold allowed)

(Art. 5) - no withholding

Слайд 54European Tax Law

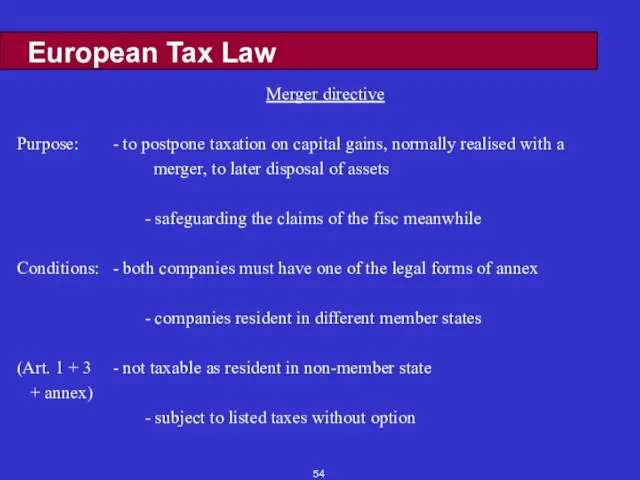

Merger directive

Purpose: - to postpone taxation on capital gains, normally realised

European Tax Law

Merger directive

Purpose: - to postpone taxation on capital gains, normally realised

Слайд 55European Tax Law

Merger directive

Types of transaction:

(Art. 2)

1) merger: * transfer of all assets + liabilities

European Tax Law

Merger directive

Types of transaction:

(Art. 2)

1) merger: * transfer of all assets + liabilities

Слайд 56European Tax Law

Merger directive

Types of transaction:

(Art. 2)

3) transfer of

assets: * A transfers "branch of activity"

European Tax Law

Merger directive

Types of transaction:

(Art. 2)

3) transfer of

assets: * A transfers "branch of activity"

Слайд 57European Tax Law

Merger directive

System: 1. For mergers, divisions, transfers of assets

(Art. 4, 5, -

European Tax Law

Merger directive

System: 1. For mergers, divisions, transfers of assets

(Art. 4, 5, -

Слайд 58European Tax Law

7. Arbitration Convention

Basis: article 220 (now 293) EU treaty

Objective: removal of double

European Tax Law

7. Arbitration Convention

Basis: article 220 (now 293) EU treaty

Objective: removal of double

Слайд 59European Tax Law

8. Interest/royalty directive

* In force since 1 January 2004

* Eliminates

European Tax Law

8. Interest/royalty directive

* In force since 1 January 2004

* Eliminates

Слайд 60European Tax Law

9. European company (SE) statute

* regulation adopted 8 October 2001 (+

European Tax Law

9. European company (SE) statute

* regulation adopted 8 October 2001 (+

Культурное наследие Торопца

Культурное наследие Торопца Экзистенциальные методы психосоциальной работы

Экзистенциальные методы психосоциальной работы Изменения внешней среды деятельности организаций

Изменения внешней среды деятельности организаций Роль общественно – полезного труда в воспитании ребенка

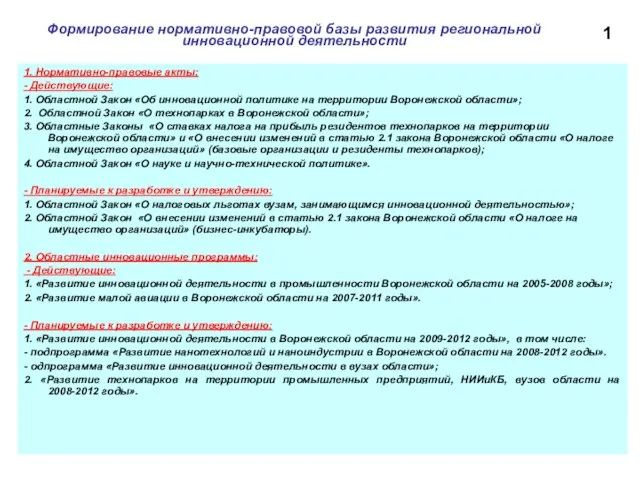

Роль общественно – полезного труда в воспитании ребенка 1

1 Темная материя в Солнечной системе

Темная материя в Солнечной системе Закон инерции- первый закон Ньютона. Место человека во Вселенной

Закон инерции- первый закон Ньютона. Место человека во Вселенной Как управлять временем преподавателю в условиях дистанта. Тайм-менеджмент преподавателя

Как управлять временем преподавателю в условиях дистанта. Тайм-менеджмент преподавателя Урок 1.Тема: Что такое нано?

Урок 1.Тема: Что такое нано? Лепим "Снеговика"

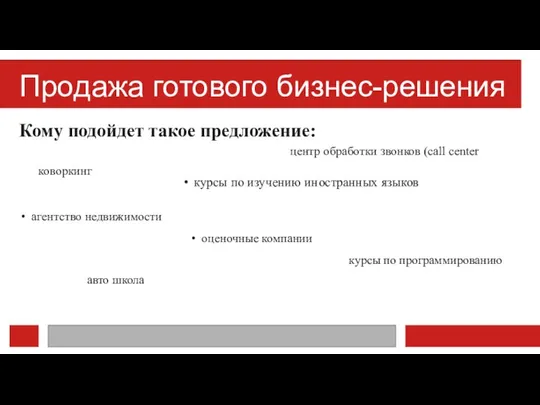

Лепим "Снеговика" Продажа готового бизнес-решения

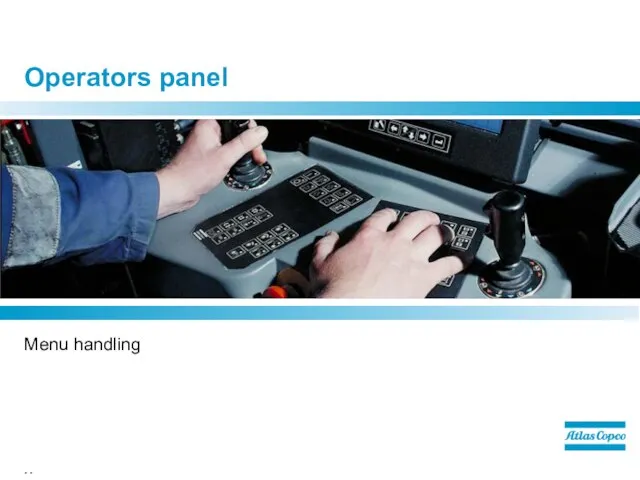

Продажа готового бизнес-решения Operators panel

Operators panel U.S.-Kazakhstan University Partnerships Grants Program. Подготовка учителей во время карантина

U.S.-Kazakhstan University Partnerships Grants Program. Подготовка учителей во время карантина Полигон Банковское дело

Полигон Банковское дело Жизнь леса

Жизнь леса Квадратные уравнения

Квадратные уравнения БВПУ

БВПУ Слава Армии родной, в день её рожденья!

Слава Армии родной, в день её рожденья! Всемирный день иммунитета

Всемирный день иммунитета Кот по кличке Босс

Кот по кличке Босс Современное рыночное хозяйство

Современное рыночное хозяйство Внеурочная деятельность школьников

Внеурочная деятельность школьников Interrelation of cognitive areas

Interrelation of cognitive areas Depression. How to deal with it

Depression. How to deal with it Программа УМНИК. Стимулирование участия молодежи в научно-технической деятельности путем организационной и финансовой поддержки

Программа УМНИК. Стимулирование участия молодежи в научно-технической деятельности путем организационной и финансовой поддержки О проекте стратегии развития медицинской промышленности Российской Федерации. Региональные факторы развития

О проекте стратегии развития медицинской промышленности Российской Федерации. Региональные факторы развития Массаж

Массаж Сретение господне

Сретение господне