- Economics of enterprises

Содержание

- 2. Financial results of economic activity (revenue and profit) Effectiveness and Financial diagnostics Lecture 8 Results and

- 3. to read in Ukrainian Економіка підприємства./ За заг. ред. С.Ф. Покропивного – К.: КНЕУ, 2001. –

- 4. Financial results of economic activity. Part 1 Revenue Revenue is the amount of money a company

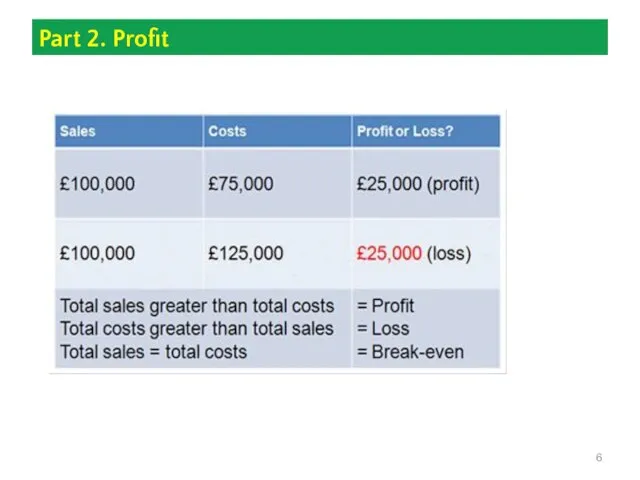

- 5. Part 2. Profit Profit is that money that your business retains after all expenses have been

- 6. Part 2. Profit

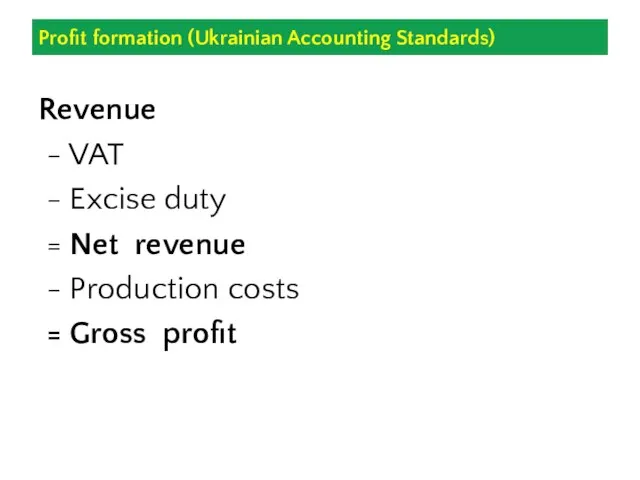

- 7. Profit formation (Ukrainian Accounting Standards) Revenue - VAT - Excise duty = Net revenue - Production

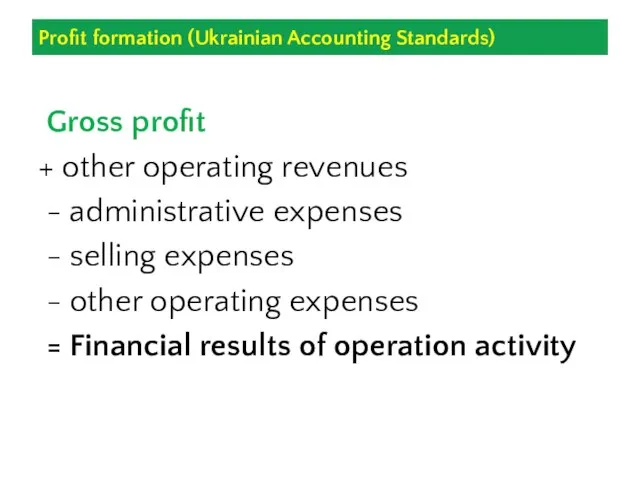

- 8. Profit formation (Ukrainian Accounting Standards) Gross profit + other operating revenues - administrative expenses - selling

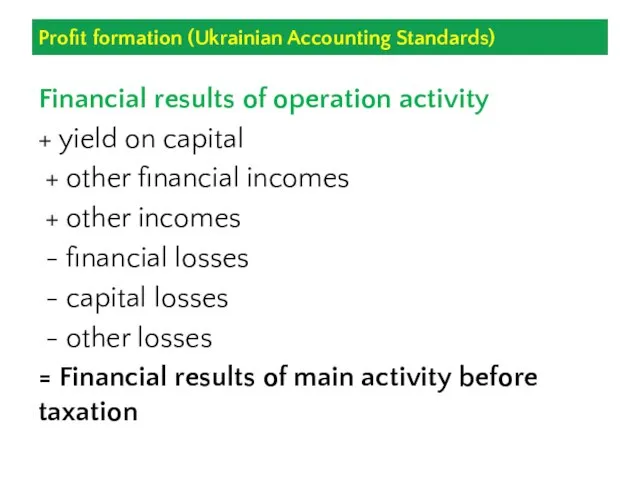

- 9. Profit formation (Ukrainian Accounting Standards) Financial results of operation activity + yield on capital + other

- 10. Profit formation (Ukrainian Accounting Standards) Financial results of main activity before taxation - income tax =

- 11. Gross profit equals sales revenue minus costs of good sold (COGS). Earnings Before Interest, Taxes, Depreciation

- 12. Earnings Before Tax (EBT) or Net Profit Before Tax equals sales revenue minus cost of goods

- 13. Functions of profit Evaluation – characterizes effect of economic activity Distribution – distribution of income between

- 14. What influences profit? Changes in sales structure of assortment prices of goods prices of raw materials

- 15. 2. Financial diagnostics Economic diagnostics – analysis and evaluation of results of activity of the enterprise

- 16. Effective economic activity Enterprise utilizes existing assets effectively Enterprise pays off its debts in time Enterprise

- 17. Financial diagnostics (1) Full-scale financial analysis of results of economic activity of the enterprise Horizontal –

- 18. Forms of financial statements balance sheet income (financial results) statement cash flow statement equity capital statement

- 19. Financial ratios Operational analysis Analysis of operational expenses Analysis of assets management Liquidity analysis Analysis of

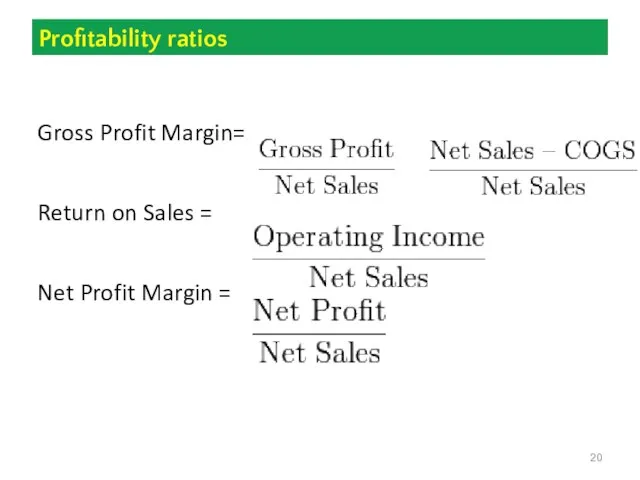

- 20. Profitability ratios Gross Profit Margin= Return on Sales = Net Profit Margin =

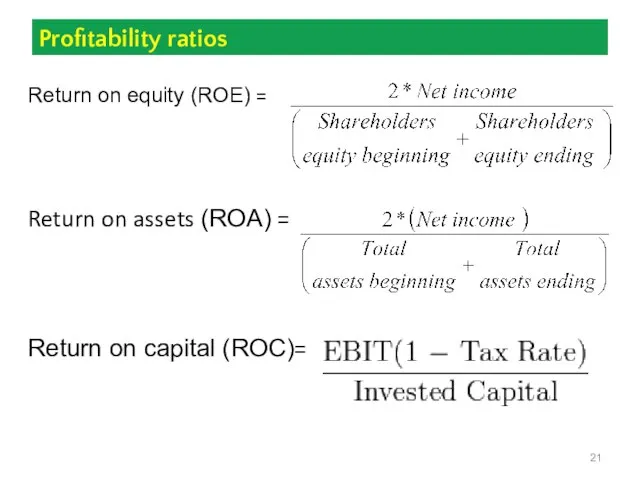

- 21. Profitability ratios Return on equity (ROE) = Return on assets (ROA) = Return on capital (ROC)=

- 23. Скачать презентацию

Слайд 2Financial results of economic activity (revenue and profit)

Effectiveness and Financial diagnostics

Lecture

Financial results of economic activity (revenue and profit)

Effectiveness and Financial diagnostics

Lecture

Слайд 3to read

in Ukrainian

Економіка підприємства./ За заг. ред. С.Ф. Покропивного – К.: КНЕУ,

to read

in Ukrainian

Економіка підприємства./ За заг. ред. С.Ф. Покропивного – К.: КНЕУ,

Слайд 4Financial results of economic activity.

Part 1 Revenue

Revenue

is the amount

Financial results of economic activity.

Part 1 Revenue

Revenue

is the amount

Слайд 5Part 2. Profit

Profit

is that money that your business retains after

Part 2. Profit

Profit

is that money that your business retains after

Слайд 6Part 2. Profit

Part 2. Profit

Слайд 7Profit formation (Ukrainian Accounting Standards)

Revenue

- VAT

- Excise duty

=

Profit formation (Ukrainian Accounting Standards)

Revenue

- VAT

- Excise duty

=

Слайд 8Profit formation (Ukrainian Accounting Standards)

Gross profit

+ other operating revenues

- administrative

Profit formation (Ukrainian Accounting Standards)

Gross profit

+ other operating revenues

- administrative

Слайд 9Profit formation (Ukrainian Accounting Standards)

Financial results of operation activity

+ yield on

Profit formation (Ukrainian Accounting Standards)

Financial results of operation activity

+ yield on

Слайд 10Profit formation (Ukrainian Accounting Standards)

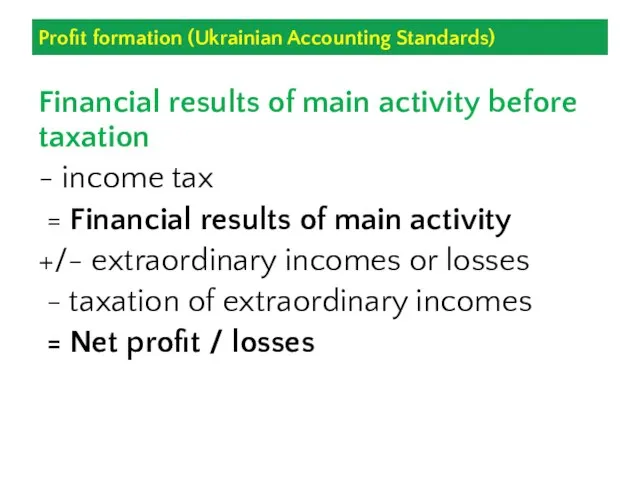

Financial results of main activity before taxation

- income

Profit formation (Ukrainian Accounting Standards)

Financial results of main activity before taxation

- income

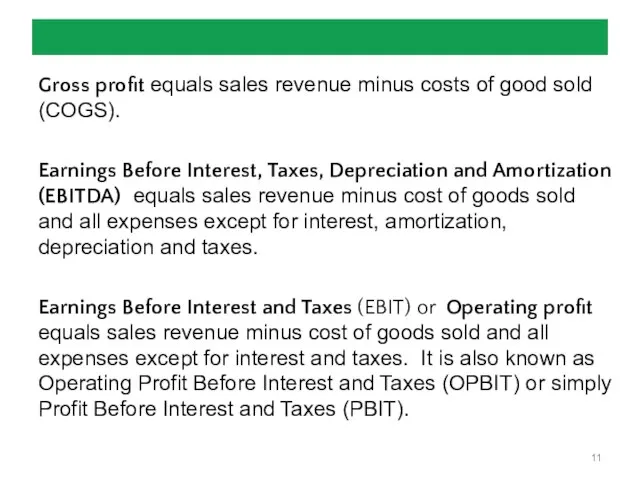

Слайд 11Gross profit equals sales revenue minus costs of good sold (COGS).

Earnings Before

Gross profit equals sales revenue minus costs of good sold (COGS).

Earnings Before

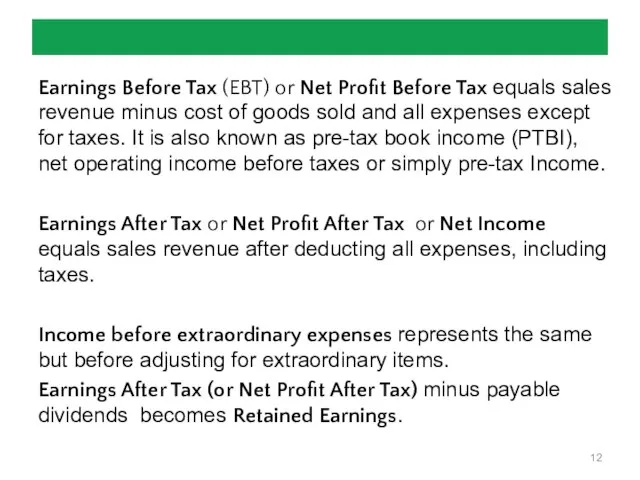

Слайд 12Earnings Before Tax (EBT) or Net Profit Before Tax equals sales revenue

Earnings Before Tax (EBT) or Net Profit Before Tax equals sales revenue

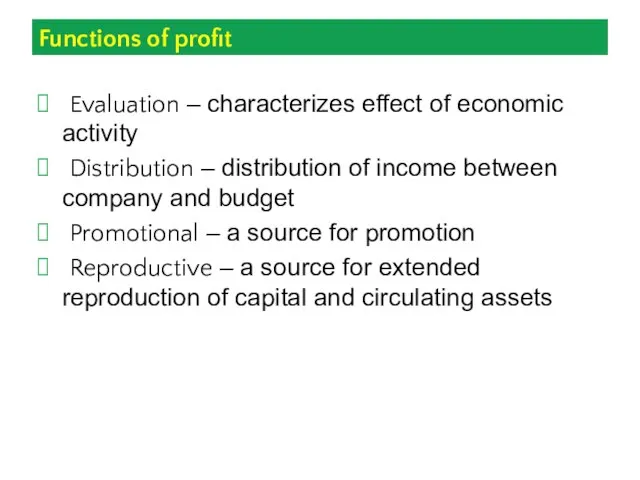

Слайд 13Functions of profit

Evaluation – characterizes effect of economic activity

Distribution

Functions of profit

Evaluation – characterizes effect of economic activity

Distribution

Слайд 14What influences profit?

Changes in

sales

structure of assortment

prices of goods

prices

What influences profit?

Changes in

sales

structure of assortment

prices of goods

prices

Слайд 152. Financial diagnostics

Economic diagnostics – analysis and evaluation of results of activity

2. Financial diagnostics

Economic diagnostics – analysis and evaluation of results of activity

Слайд 16Effective economic activity

Enterprise utilizes existing assets effectively

Enterprise pays off its

Effective economic activity

Enterprise utilizes existing assets effectively

Enterprise pays off its

Слайд 17Financial diagnostics (1)

Full-scale financial analysis of results of economic activity of the

Financial diagnostics (1)

Full-scale financial analysis of results of economic activity of the

Слайд 18Forms of financial statements

balance sheet

income (financial results) statement

cash flow

Forms of financial statements

balance sheet

income (financial results) statement

cash flow

Слайд 19Financial ratios

Operational analysis

Analysis of operational expenses

Analysis of assets management

Financial ratios

Operational analysis

Analysis of operational expenses

Analysis of assets management

Слайд 20Profitability ratios

Gross Profit Margin=

Return on Sales =

Net Profit Margin =

Profitability ratios

Gross Profit Margin=

Return on Sales =

Net Profit Margin =

Слайд 21Profitability ratios

Return on equity (ROE) =

Return on assets (ROA) =

Return on capital

Profitability ratios

Return on equity (ROE) =

Return on assets (ROA) =

Return on capital

Путь к спасению По рассказу Д.Лондона «Любовь к жизни»

Путь к спасению По рассказу Д.Лондона «Любовь к жизни» Structure of the Central Government of the UK

Structure of the Central Government of the UK Безопасность интернет-проектов

Безопасность интернет-проектов О составе отчетности по персонифицированному учету и проверке сведений, учтенных на лицевых счетах застрахованных лиц

О составе отчетности по персонифицированному учету и проверке сведений, учтенных на лицевых счетах застрахованных лиц Анализ 8 главы Федерального закона РФ Об образовании в Российской Федерации

Анализ 8 главы Федерального закона РФ Об образовании в Российской Федерации Презентация на тему Кондратий Федорович Рылеев (1795 — 1826)

Презентация на тему Кондратий Федорович Рылеев (1795 — 1826)  Лот 18, г. Хабаровск, ул. Сысоева, 21, кв. 57

Лот 18, г. Хабаровск, ул. Сысоева, 21, кв. 57 XIX Всероссийский конкурс молодежных авторских проектов Моя страна - моя Россия

XIX Всероссийский конкурс молодежных авторских проектов Моя страна - моя Россия Право в интернете

Право в интернете Критика маркетинга со стороны общественности

Критика маркетинга со стороны общественности Документационное обеспечение управления. Правила написания заявления

Документационное обеспечение управления. Правила написания заявления Гибка заготовок из тонколистового металла и проволоки

Гибка заготовок из тонколистового металла и проволоки Геометрия для самых маленьких. Геометрические фигуры

Геометрия для самых маленьких. Геометрические фигуры Проектирование резервуара вертикального стального объемом 10 000 кубических метров

Проектирование резервуара вертикального стального объемом 10 000 кубических метров Игра «Что лишнее?»Игра на закрепление знаний у детей о бытовой технике

Игра «Что лишнее?»Игра на закрепление знаний у детей о бытовой технике ФИНАЛ!!!!

ФИНАЛ!!!! Проволока

Проволока Письменная литература Древней Руси

Письменная литература Древней Руси Информационный проект нового поколения Электронно-библиотечная система Образовательные и просветительские

Информационный проект нового поколения Электронно-библиотечная система Образовательные и просветительские  Імітаційне моделювання

Імітаційне моделювання Бразилия в ХХ-ХХІ веке

Бразилия в ХХ-ХХІ веке Пылесос. Типы пылесосов

Пылесос. Типы пылесосов Оживи сказку

Оживи сказку Приготовление блюд из фруктов

Приготовление блюд из фруктов Мультимедиа т.5 - Тутынин - 2021

Мультимедиа т.5 - Тутынин - 2021 Торговый эквайринг

Торговый эквайринг Управление затратами и контроллинг

Управление затратами и контроллинг  Презентация на тему Огонь вода и газ (3 класс)

Презентация на тему Огонь вода и газ (3 класс)