- Financial Statements and Cash Flows

Содержание

- 2. Contents Balance sheet statement and its managerial applications; Income statement and its managerial applications; The concept

- 3. Balance Sheet reflects the financial position of a firm By “financial position” we mean: Assets Liabilities

- 4. Liabilities are obligations of the entity to outside parties (“creditors”): Result from past transactions (purchase through

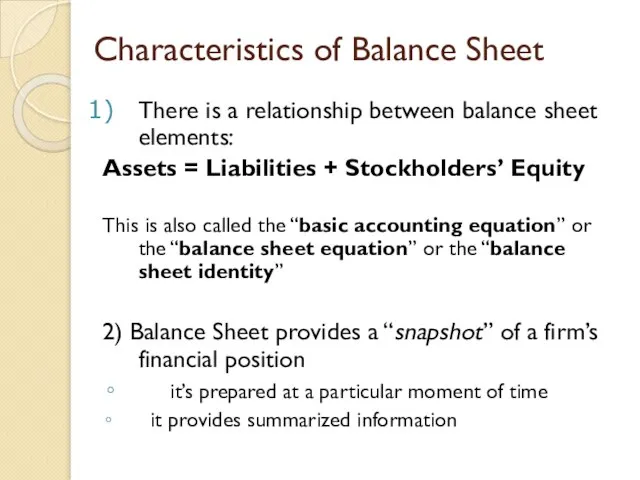

- 5. Characteristics of Balance Sheet There is a relationship between balance sheet elements: Assets = Liabilities +

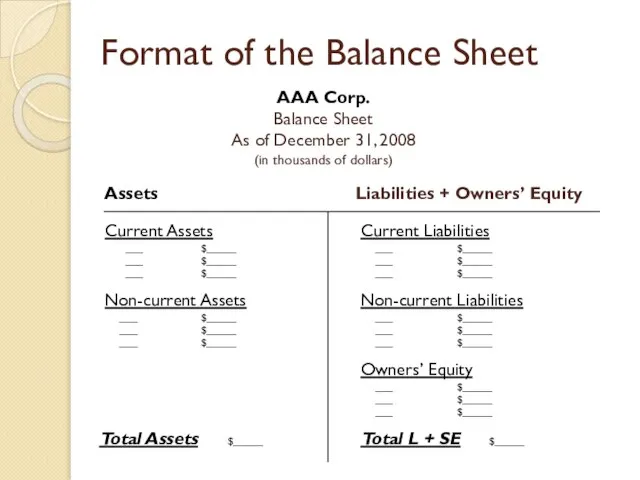

- 6. Format of the Balance Sheet AAA Corp. Balance Sheet As of December 31, 2008 (in thousands

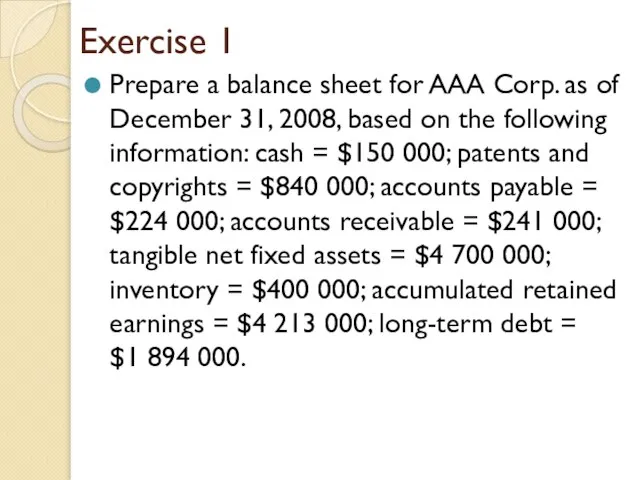

- 7. Exercise 1 Prepare a balance sheet for AAA Corp. as of December 31, 2008, based on

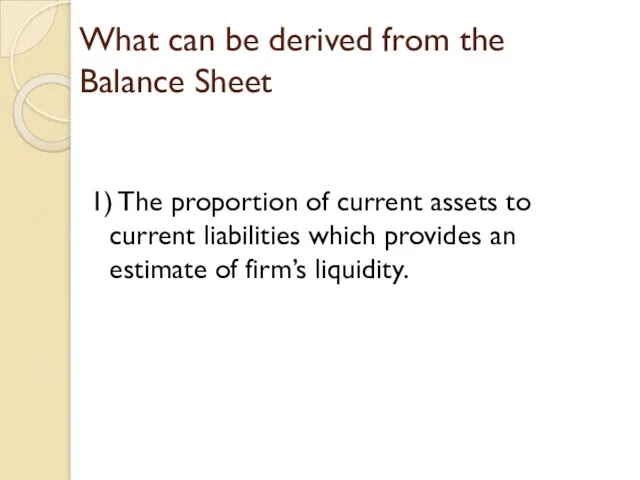

- 8. What can be derived from the Balance Sheet 1) The proportion of current assets to current

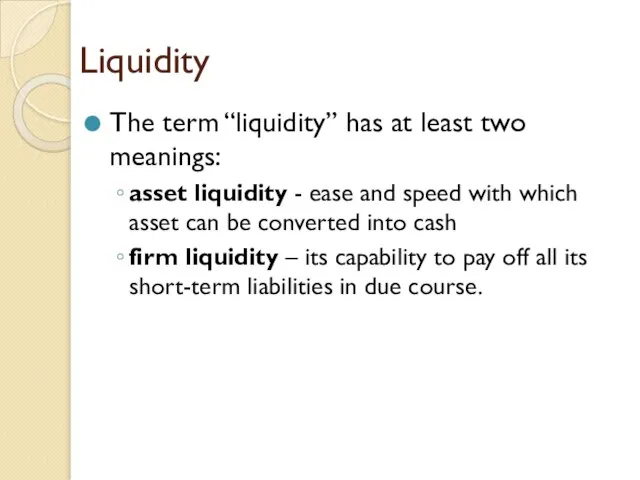

- 9. Liquidity The term “liquidity” has at least two meanings: asset liquidity - ease and speed with

- 10. The assessment of firm’s liquidity ABC Corp. Balance Sheet As of December 31, 2008 (in thousands

- 11. Exercise 1I XYZ company has the following assets and liabilities: cash = $2,000, manufacturing equipment =

- 12. Exercise 1I Shareholders’ equity = 13,500+2,000+2,400+5,000-4,000-3,000=15,900 Working capital in accounting sense=2,000+2,400+5,000-4,000-3,000=2,400 Working capital in economic sense=2,000+2,400+5,000-4,000=5,400

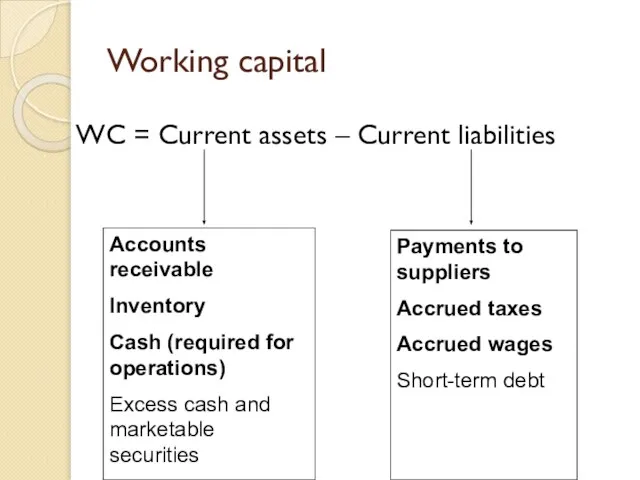

- 13. Working capital Working capital (WC) is a difference between firm’s current assets and current liabilities Working

- 14. Working capital WC = Current assets – Current liabilities Accounts receivable Inventory Cash (required for operations)

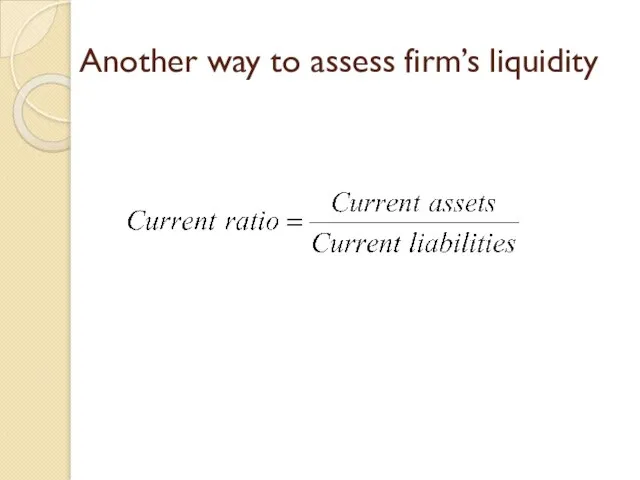

- 15. Another way to assess firm’s liquidity

- 16. What can be derived from the Balance Sheet 2) The proportion in which debt and equity

- 17. The income statement provides an assessment of firm’s performance over a particular period of time The

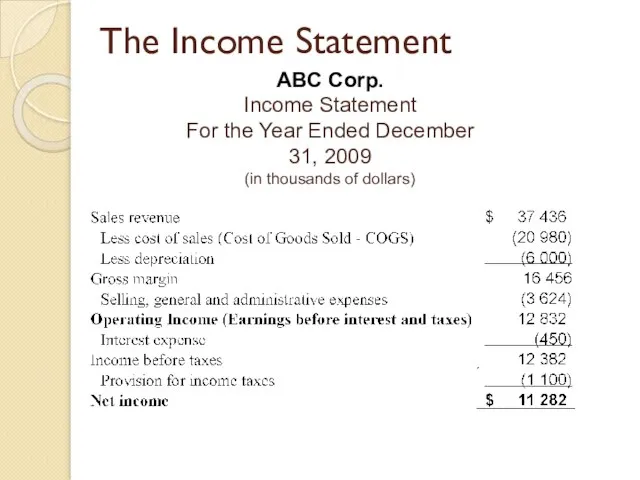

- 18. The Income Statement ABC Corp. Income Statement For the Year Ended December 31, 2009 (in thousands

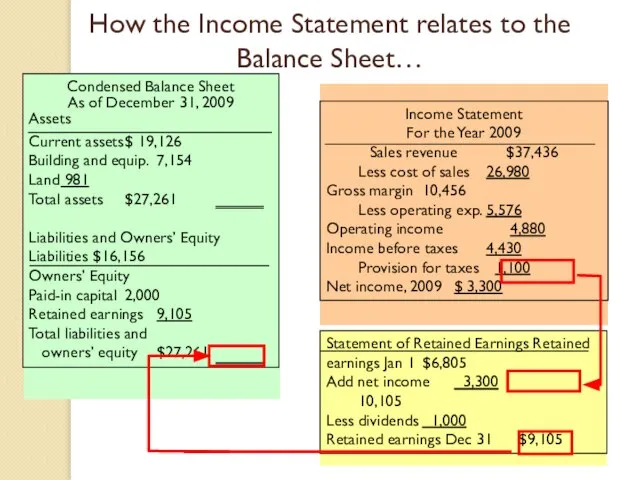

- 19. How the Income Statement relates to the Balance Sheet…

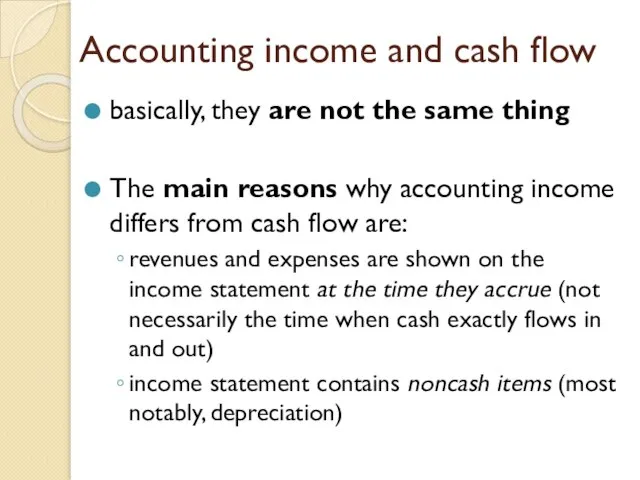

- 20. Accounting income and cash flow basically, they are not the same thing The main reasons why

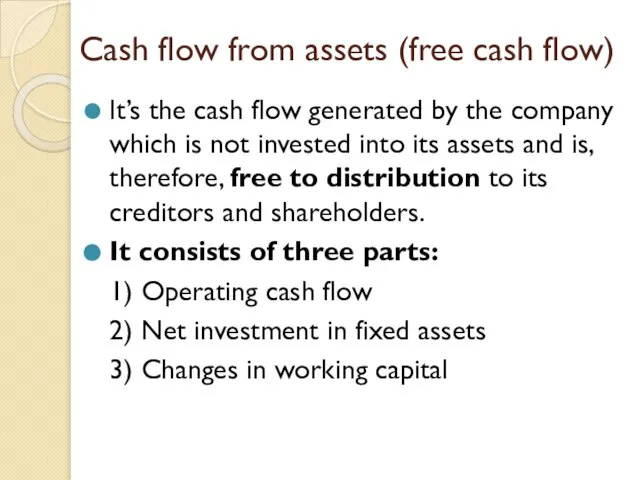

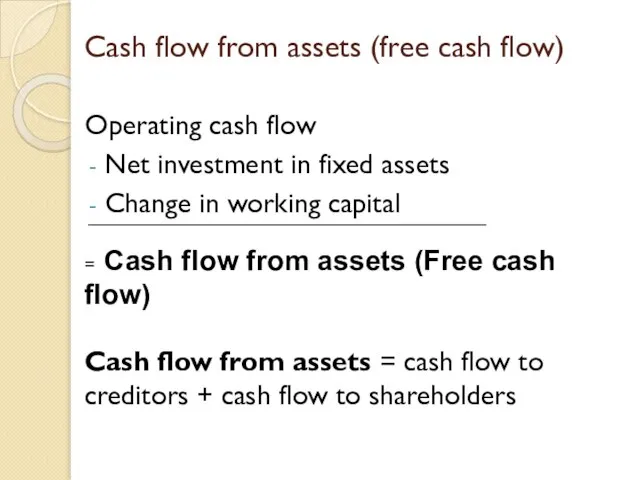

- 21. Сash flow from assets (free cash flow) It’s the cash flow generated by the company which

- 22. Cash flow from assets (free cash flow) Operating cash flow Net investment in fixed assets Change

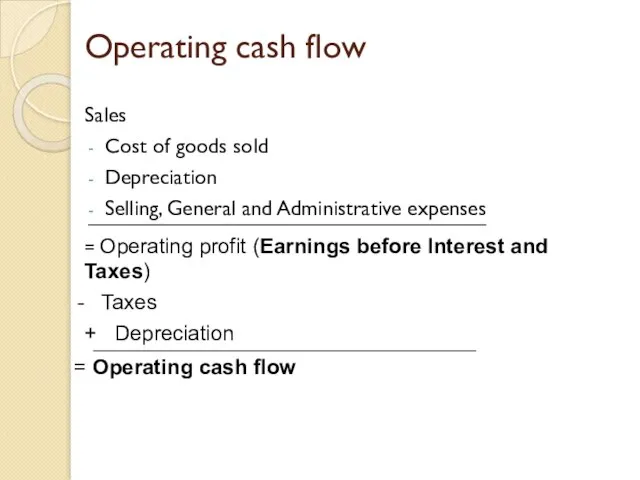

- 23. Operating cash flow Sales Cost of goods sold Depreciation Selling, General and Administrative expenses = Operating

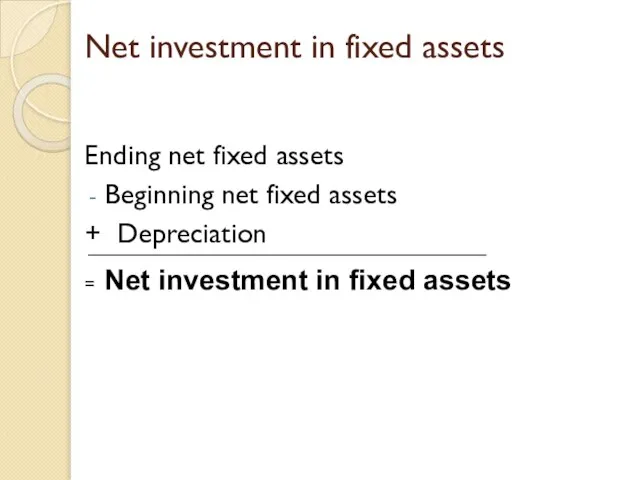

- 24. Net investment in fixed assets Ending net fixed assets Beginning net fixed assets + Depreciation =

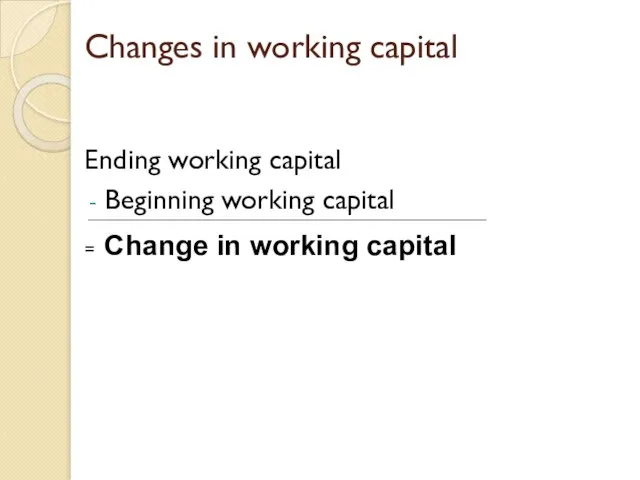

- 25. Changes in working capital Ending working capital Beginning working capital = Change in working capital

- 26. Cash flow to creditors Interest paid New net borrowing = Cash flow to creditors

- 28. Скачать презентацию

Слайд 2Contents

Balance sheet statement and its managerial applications;

Income statement and its managerial applications;

The

Contents

Balance sheet statement and its managerial applications;

Income statement and its managerial applications;

The

Слайд 3Balance Sheet reflects the financial position of a firm

By “financial position” we

Balance Sheet reflects the financial position of a firm

By “financial position” we

Слайд 4Liabilities are obligations of the entity to outside parties (“creditors”):

Result from past

Liabilities are obligations of the entity to outside parties (“creditors”):

Result from past

Слайд 5Characteristics of Balance Sheet

There is a relationship between balance sheet elements:

Assets =

Characteristics of Balance Sheet

There is a relationship between balance sheet elements:

Assets =

Слайд 6Format of the Balance Sheet

AAA Corp.

Balance Sheet

As of December 31, 2008

(in thousands

Format of the Balance Sheet

AAA Corp.

Balance Sheet

As of December 31, 2008

(in thousands

Слайд 7Exercise 1

Prepare a balance sheet for AAA Corp. as of December 31,

Exercise 1

Prepare a balance sheet for AAA Corp. as of December 31,

Слайд 8What can be derived from the Balance Sheet

1) The proportion of current

What can be derived from the Balance Sheet

1) The proportion of current

Слайд 9Liquidity

The term “liquidity” has at least two meanings:

asset liquidity - ease and

Liquidity

The term “liquidity” has at least two meanings:

asset liquidity - ease and

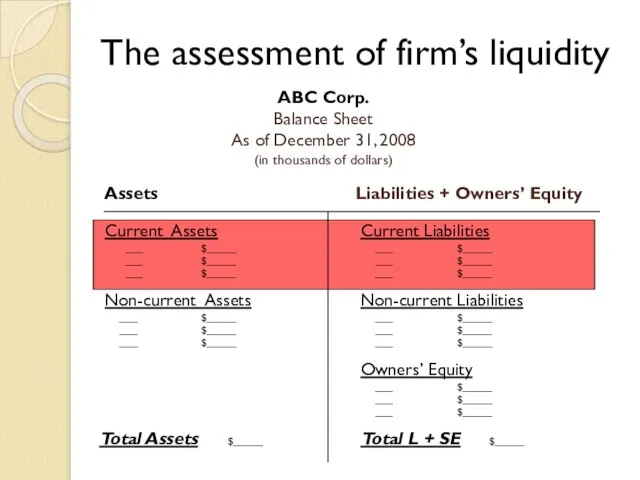

Слайд 10The assessment of firm’s liquidity

ABC Corp.

Balance Sheet

As of December 31, 2008

(in thousands

The assessment of firm’s liquidity

ABC Corp.

Balance Sheet

As of December 31, 2008

(in thousands

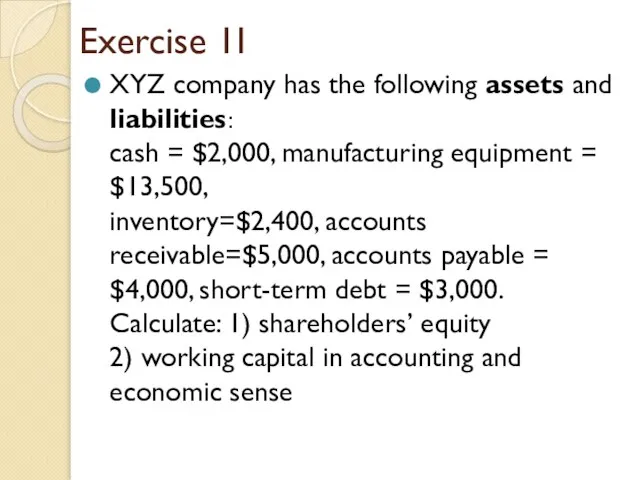

Слайд 11Exercise 1I

XYZ company has the following assets and liabilities:

cash = $2,000, manufacturing

Exercise 1I

XYZ company has the following assets and liabilities:

cash = $2,000, manufacturing

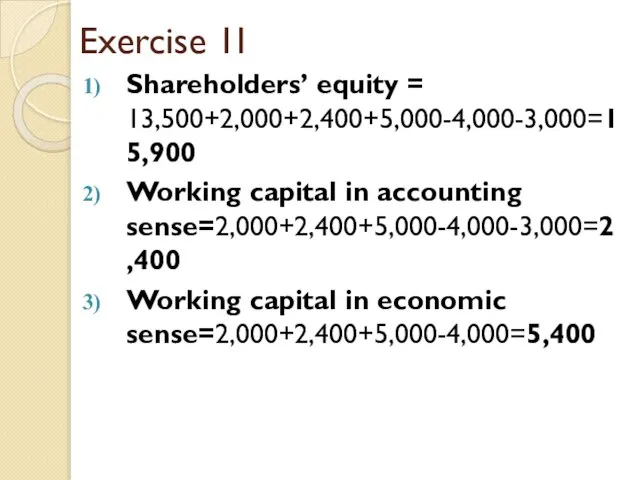

Слайд 12Exercise 1I

Shareholders’ equity = 13,500+2,000+2,400+5,000-4,000-3,000=15,900

Working capital in accounting sense=2,000+2,400+5,000-4,000-3,000=2,400

Working capital in economic

Exercise 1I

Shareholders’ equity = 13,500+2,000+2,400+5,000-4,000-3,000=15,900

Working capital in accounting sense=2,000+2,400+5,000-4,000-3,000=2,400

Working capital in economic

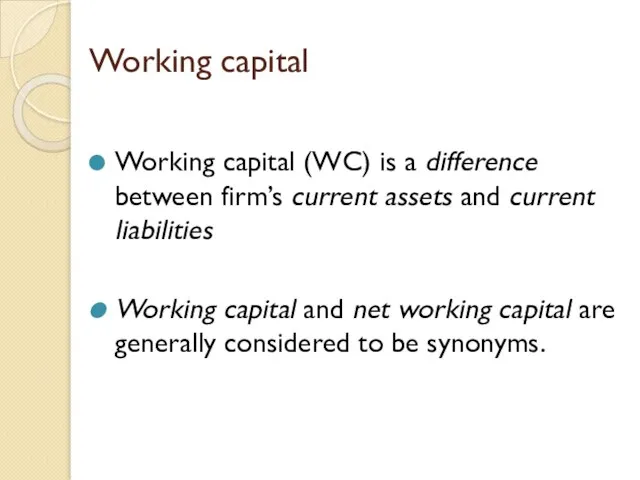

Слайд 13Working capital

Working capital (WC) is a difference between firm’s current assets and

Working capital

Working capital (WC) is a difference between firm’s current assets and

Слайд 14Working capital

WC = Current assets – Current liabilities

Accounts receivable

Inventory

Cash (required for operations)

Excess

Working capital

WC = Current assets – Current liabilities

Accounts receivable

Inventory

Cash (required for operations)

Excess

Слайд 15Another way to assess firm’s liquidity

Another way to assess firm’s liquidity

Слайд 16What can be derived from the Balance Sheet

2) The proportion in which

What can be derived from the Balance Sheet

2) The proportion in which

Слайд 17The income statement

provides an assessment of firm’s performance over a particular period

The income statement

provides an assessment of firm’s performance over a particular period

Слайд 18The Income Statement

ABC Corp.

Income Statement

For the Year Ended December 31, 2009

(in thousands

The Income Statement

ABC Corp.

Income Statement

For the Year Ended December 31, 2009

(in thousands

Слайд 19How the Income Statement relates to the Balance Sheet…

How the Income Statement relates to the Balance Sheet…

Слайд 20Accounting income and cash flow

basically, they are not the same thing

The main

Accounting income and cash flow

basically, they are not the same thing

The main

Слайд 21Сash flow from assets (free cash flow)

It’s the cash flow generated by

Сash flow from assets (free cash flow)

It’s the cash flow generated by

Слайд 22Cash flow from assets (free cash flow)

Operating cash flow

Net investment in fixed

Cash flow from assets (free cash flow)

Operating cash flow

Net investment in fixed

Слайд 23Operating cash flow

Sales

Cost of goods sold

Depreciation

Selling, General and Administrative expenses

= Operating profit

Operating cash flow

Sales

Cost of goods sold

Depreciation

Selling, General and Administrative expenses

= Operating profit

Слайд 24Net investment in fixed assets

Ending net fixed assets

Beginning net fixed assets

Net investment in fixed assets

Ending net fixed assets

Beginning net fixed assets

Слайд 25Changes in working capital

Ending working capital

Beginning working capital

= Change in working capital

Changes in working capital

Ending working capital

Beginning working capital

= Change in working capital

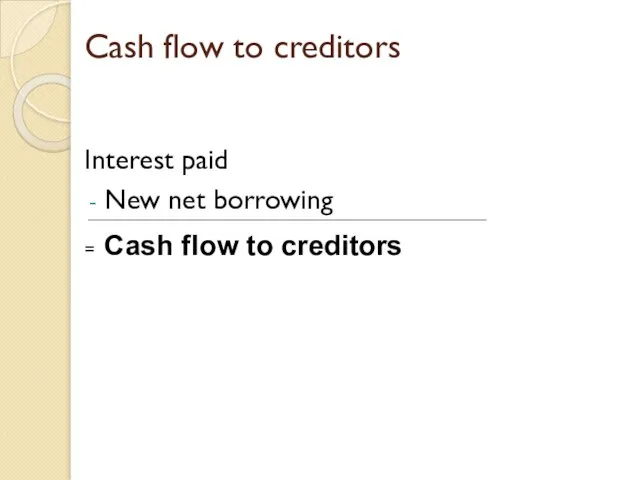

Слайд 26Cash flow to creditors

Interest paid

New net borrowing

= Cash flow to creditors

Cash flow to creditors

Interest paid

New net borrowing

= Cash flow to creditors

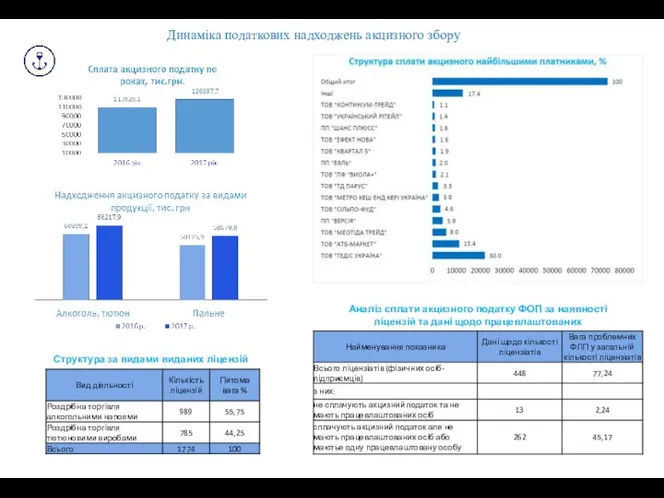

Динаміка податкових надходжень акцизного збору

Динаміка податкових надходжень акцизного збору Презентация на тему Жизнь леса. Лес – природное сообщество (4 класс)

Презентация на тему Жизнь леса. Лес – природное сообщество (4 класс) Презентация на тему Почва – среда жизни организмов. Состав почвы

Презентация на тему Почва – среда жизни организмов. Состав почвы New Media: 2.0 в пользу вашего бизнесаКак использовать социальные сети для продвижения продуктов и брендов?

New Media: 2.0 в пользу вашего бизнесаКак использовать социальные сети для продвижения продуктов и брендов? Аффектогенные образы в рекламе: психотехнический анализ

Аффектогенные образы в рекламе: психотехнический анализ МОУ СОШ № 12

МОУ СОШ № 12 Урок 4 різці та їх загострення

Урок 4 різці та їх загострення Классный час«О дружбе»2 «А» класс

Классный час«О дружбе»2 «А» класс Истоки архитектуры

Истоки архитектуры Крыша

Крыша Презентация на тему Современные мастера, прославившие Россию в XVIII-XXI веках

Презентация на тему Современные мастера, прославившие Россию в XVIII-XXI веках Фовизм

Фовизм Принципы финансов

Принципы финансов Основы логики и логические основы компьютера

Основы логики и логические основы компьютера Алгоритм построения сечения

Алгоритм построения сечения Сетевое сообщество молодых учителей Сеченовского муниципального района

Сетевое сообщество молодых учителей Сеченовского муниципального района Частотные преобразователи для горной промышленности

Частотные преобразователи для горной промышленности Правописание Н и НН во всех частях речи

Правописание Н и НН во всех частях речи Транспорт Москвы Алекси Парккила & Вилле Мякинен школа восточной финляндии Лаппеенранта & Йоенсуу

Транспорт Москвы Алекси Парккила & Вилле Мякинен школа восточной финляндии Лаппеенранта & Йоенсуу Презентация на тему Язык и речь

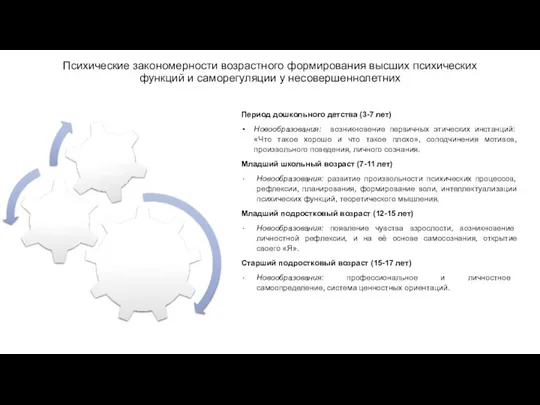

Презентация на тему Язык и речь Психические закономерности возрастного формирования высших психических функций и саморегуляции у несовершеннолетних

Психические закономерности возрастного формирования высших психических функций и саморегуляции у несовершеннолетних Шар. Елка. Снеговик

Шар. Елка. Снеговик Участие граждан в политической жизни

Участие граждан в политической жизни Умножение и деление многозначных чисел

Умножение и деление многозначных чисел Применение информационных технологий при обучении иностранным языкам

Применение информационных технологий при обучении иностранным языкам Индивидуальный маршрут карьерного роста

Индивидуальный маршрут карьерного роста IV Национальный чемпионат по профессиональному мастерству среди лиц с ограниченными возможностями здоровья Абилимпикс

IV Национальный чемпионат по профессиональному мастерству среди лиц с ограниченными возможностями здоровья Абилимпикс ИСТОРИЯ ОРИГАМИ

ИСТОРИЯ ОРИГАМИ