- International Money and Finance

Содержание

- 2. International Money and Finance Reasons to study global finance. Why IM&F studies are important: They give

- 3. International Money and Finance IM&F Development The Gold Standard Stage 1 Paris Conference of 1867 Main

- 4. International Money and Finance IM&F Development The Gold Standard Stage 2 Genova Conference of 1922 Main

- 5. International Money and Finance IM&F Development The Bretton Woods system (BWS) Bretton Woods Conference of 1944

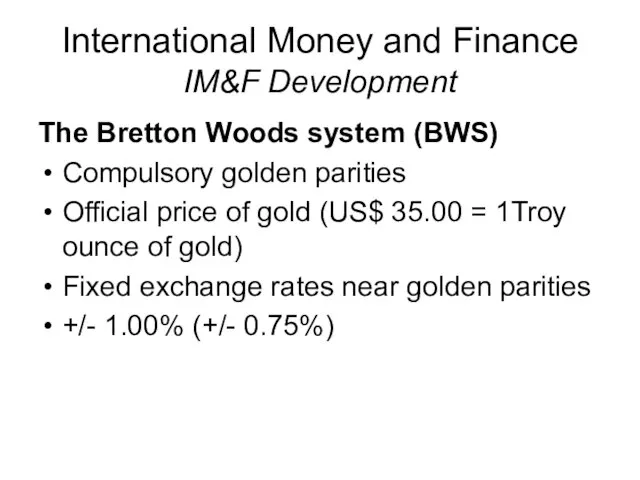

- 6. International Money and Finance IM&F Development The Bretton Woods system (BWS) Compulsory golden parities Official price

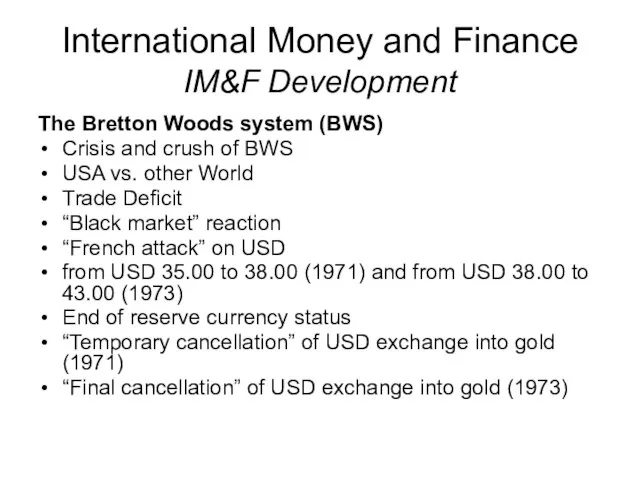

- 7. International Money and Finance IM&F Development The Bretton Woods system (BWS) Crisis and crush of BWS

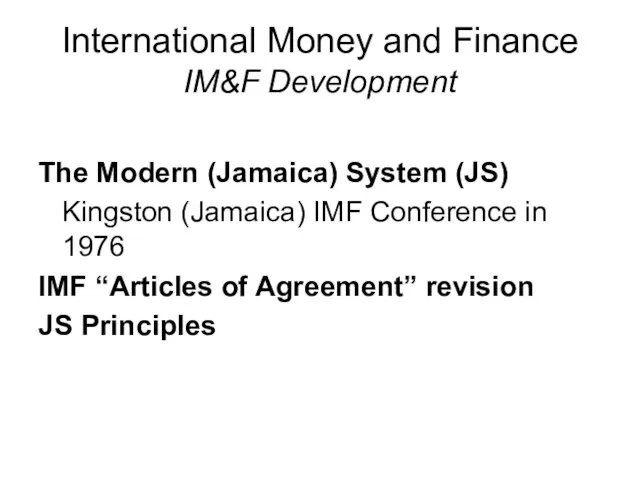

- 8. International Money and Finance IM&F Development The Modern (Jamaica) System (JS) Kingston (Jamaica) IMF Conference in

- 9. International Money and Finance IM&F Development JS Principles: International money – national currencies (free convertible currencies)

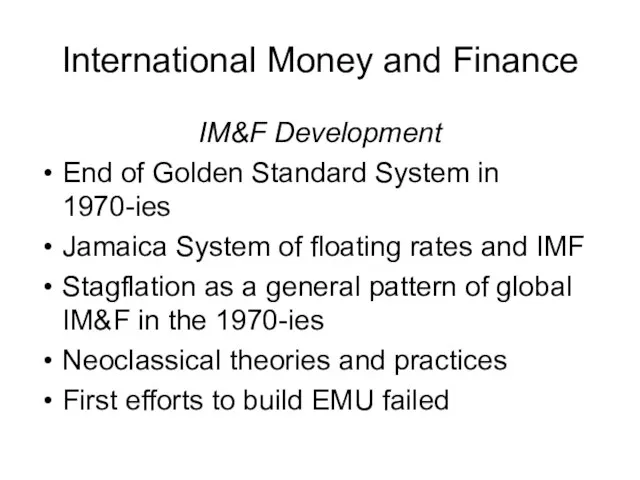

- 10. International Money and Finance IM&F Development End of Golden Standard System in 1970-ies Jamaica System of

- 11. International Money and Finance IM&F Development Start of neoclassical reforms in developed economies: implications for IM&F

- 12. International Money and Finance IM&F Development Creation of global TNCs and globalization of their financial flows

- 13. International Money and Finance IM&F Development “Booming Age” of 1990-2007, boom in financial sector Federal Reserve:

- 14. International Money and Finance IM&F Development Building EMU Maastricht Treaty and its criteria Difficulties in 1995,

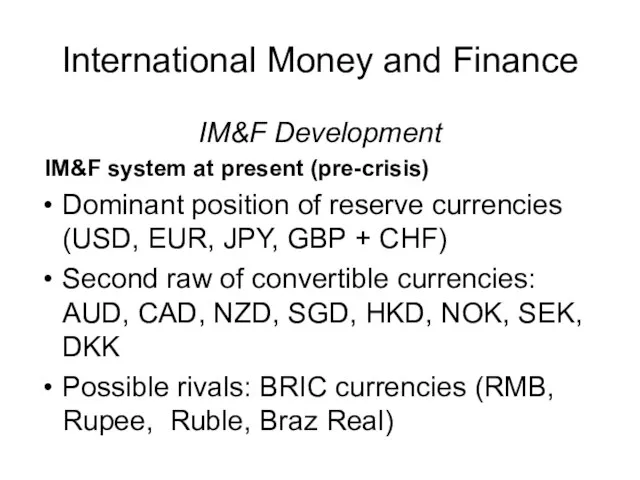

- 15. International Money and Finance IM&F Development IM&F system at present (pre-crisis) Dominant position of reserve currencies

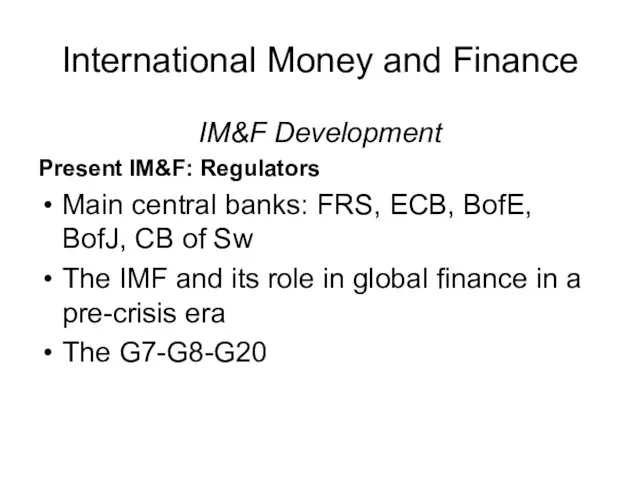

- 16. International Money and Finance IM&F Development Present IM&F: Regulators Main central banks: FRS, ECB, BofE, BofJ,

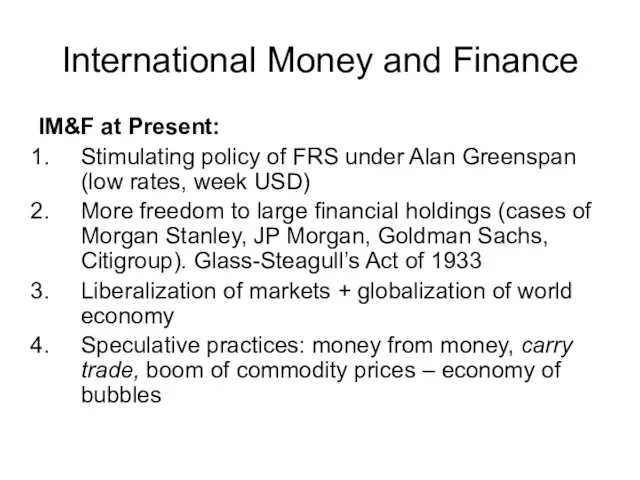

- 17. International Money and Finance IM&F at Present: Stimulating policy of FRS under Alan Greenspan (low rates,

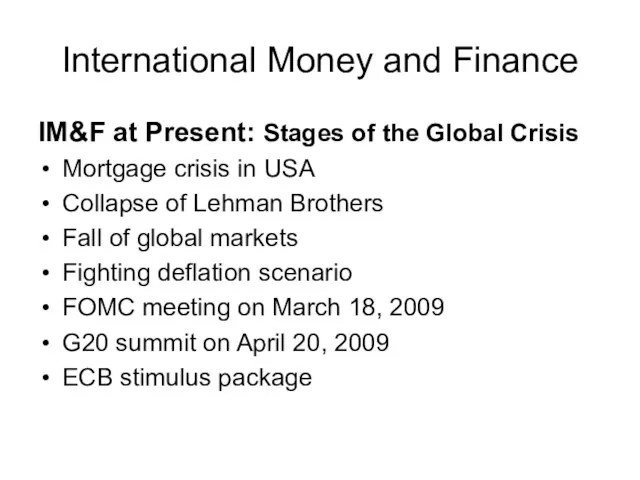

- 18. International Money and Finance IM&F at Present: Stages of the Global Crisis Mortgage crisis in USA

- 19. International Money and Finance International Monetary Fund (IMF) Established 22.07.1944 at Bretton Woods conference, effective 27.12.1945

- 20. International Money and Finance IMF The IMF was established to promote international monetary cooperation, exchange stability,

- 21. International Money and Finance IMF Structure: Governing Bodies: Board of Governors Executive Board (Directorate) Managing Director

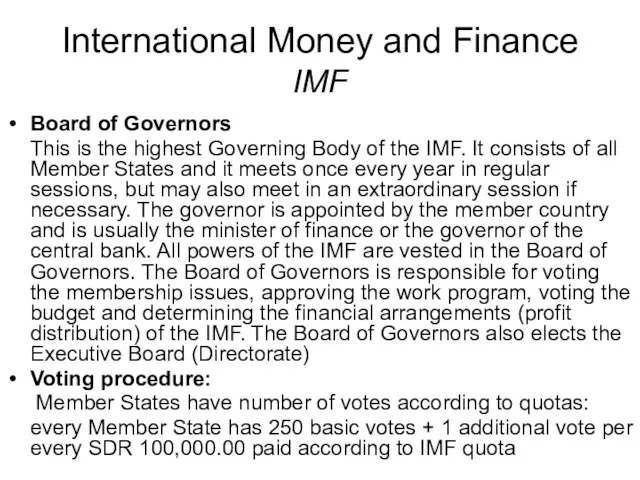

- 22. International Money and Finance IMF Board of Governors This is the highest Governing Body of the

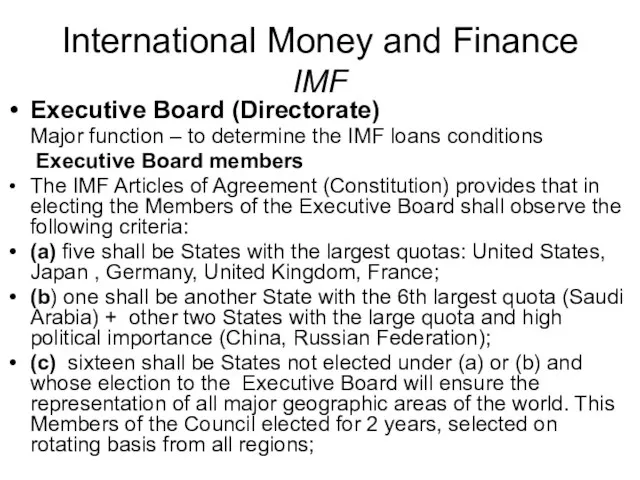

- 23. International Money and Finance IMF Executive Board (Directorate) Major function – to determine the IMF loans

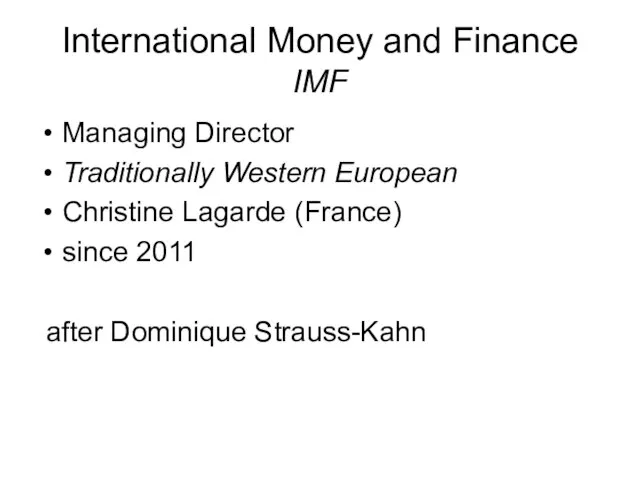

- 24. International Money and Finance IMF Managing Director Traditionally Western European Christine Lagarde (France) since 2011 after

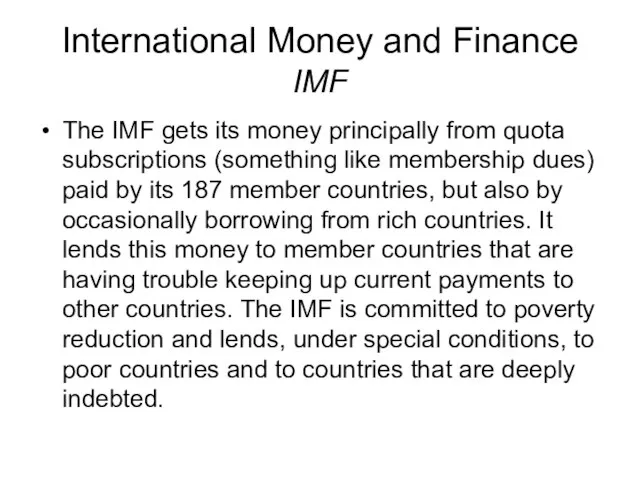

- 25. International Money and Finance IMF The IMF gets its money principally from quota subscriptions (something like

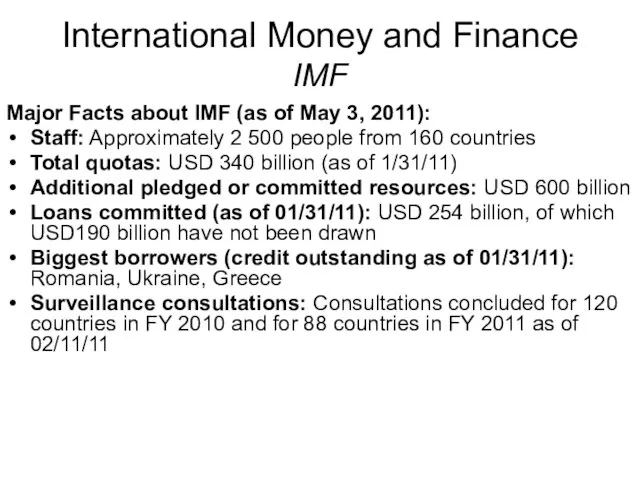

- 26. International Money and Finance IMF Major Facts about IMF (as of May 3, 2011): Staff: Approximately

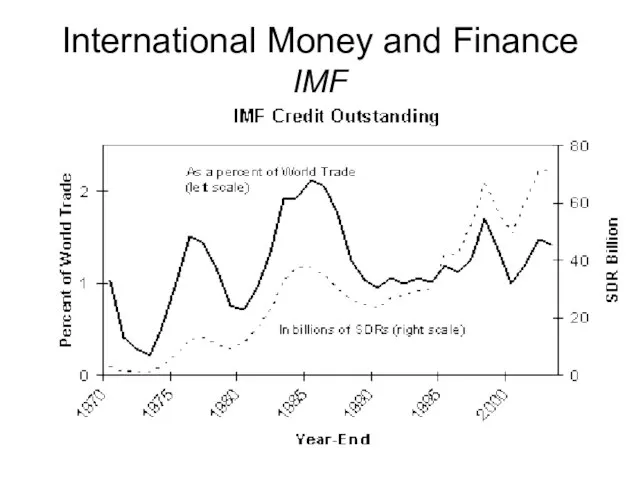

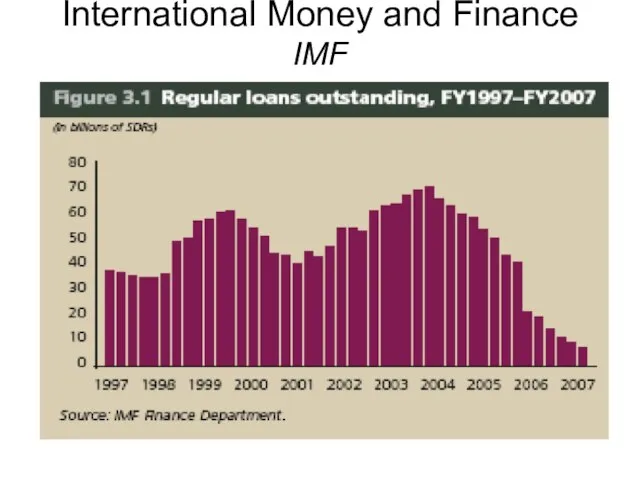

- 27. International Money and Finance IMF

- 28. International Money and Finance IMF

- 29. International Money and Finance IMF The changing nature of IMF lending: The volume of loans provided

- 30. International Money and Finance IMF IMF Lending A core responsibility of the IMF is to provide

- 31. International Money and Finance IMF The process of IMF lending: An IMF loan is usually provided

- 32. International Money and Finance Exchange rate regimes Fixed exchange rate regime based on state regulation. Float

- 33. International Money and Finance Exchange rate regimes Fixed exchange rate regime: Predictability of the rate (+)

- 34. International Money and Finance Exchange rate regimes Float exchange rate regime: More market-driven and effective (+)

- 35. International Money and Finance Exchange rate regimes Factors that determine exchange rate: Purchasing Power Parity (PPP)

- 36. International Money and Finance Exchange rate regimes Purchasing Power Parity (PPP): How much of goods and

- 37. International Money and Finance Exchange rate regimes The same basket of goods and services costs different

- 38. International Money and Finance Exchange rate regimes Trade balance and exchange rate: Low exchange rate leads

- 39. International Money and Finance Balance of payments The balance of payments, (or BOP) measures the payments

- 40. International Money and Finance Balance of payments The balance, like other accounting statements, is prepared in

- 41. International Money and Finance Balance of payments The IMF definition: "Balance of Payments is a statistical

- 42. International Money and Finance Balance of payments Balance of payments identity is a key formula The

- 43. International Money and Finance Balance of payments The basic principle behind the identity is that a

- 44. International Money and Finance Balance of payments A balance of payments equilibrium is defined as a

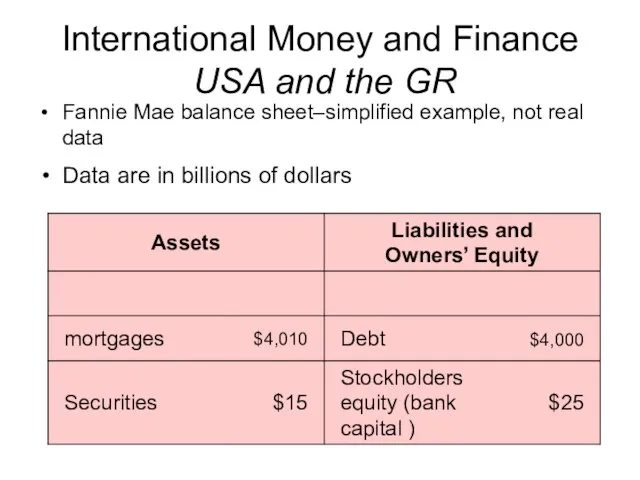

- 45. International Money and Finance USA and the GR Fannie Mae balance sheet–simplified example, not real data

- 46. International Money and Finance USA and the GR The GSEs bought about 50% of the toxic

- 47. International Money and Finance USA and the GR From the current handwringing, you’d think that the

- 48. International Money and Finance USA and the GR Clear need for new regulation and there were

- 49. International Money and Finance USA and the GR General upturn in US economy took place in

- 50. International Money and Finance EU and the Debt Crisis Maastricht Treaty and its Criteria Obligation of

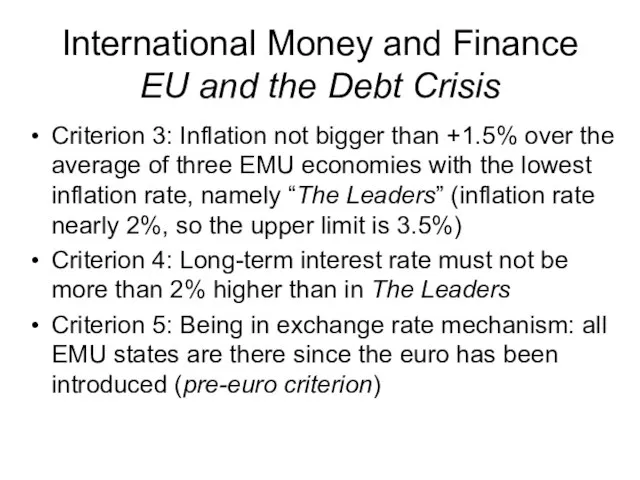

- 51. International Money and Finance EU and the Debt Crisis Criterion 3: Inflation not bigger than +1.5%

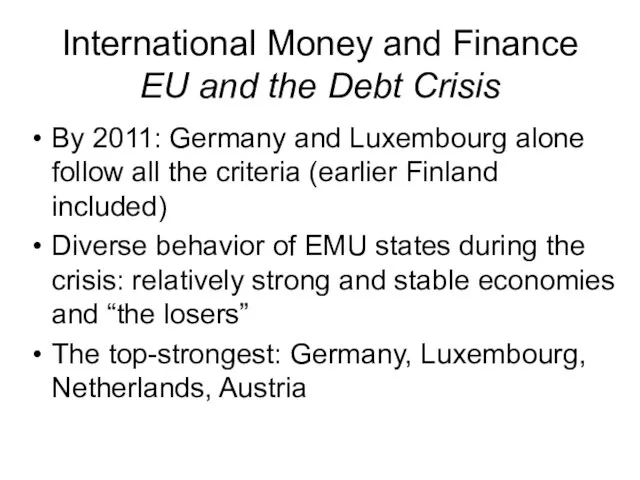

- 52. International Money and Finance EU and the Debt Crisis By 2011: Germany and Luxembourg alone follow

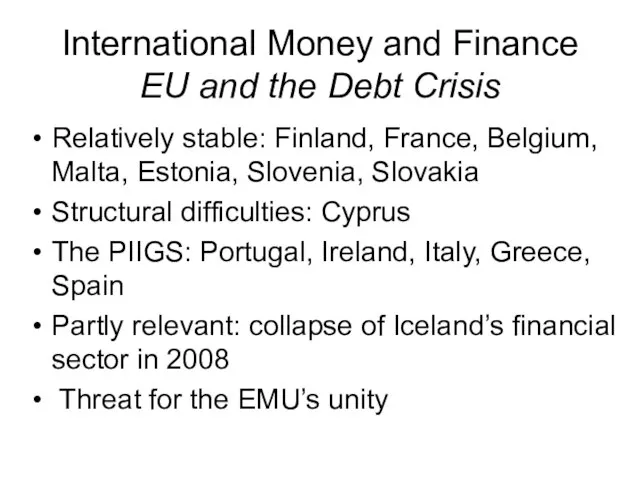

- 53. International Money and Finance EU and the Debt Crisis Relatively stable: Finland, France, Belgium, Malta, Estonia,

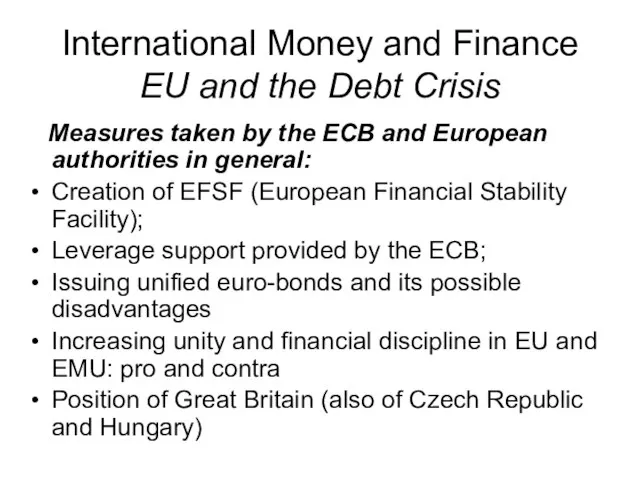

- 54. International Money and Finance EU and the Debt Crisis Measures taken by the ECB and European

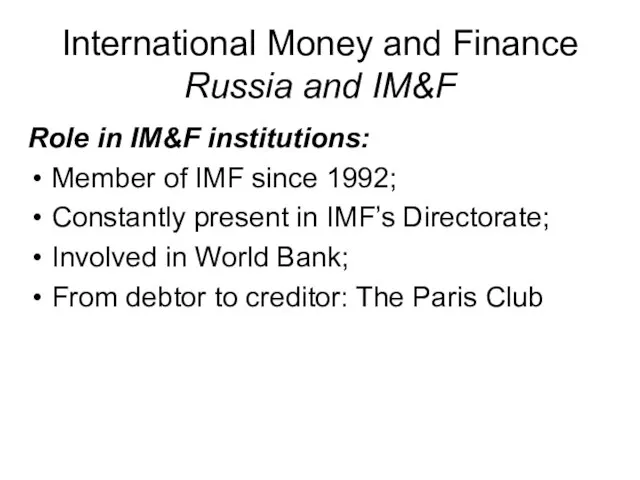

- 55. International Money and Finance Russia and IM&F Role in IM&F institutions: Member of IMF since 1992;

- 56. International Money and Finance Russia and IM&F Russia is an active player in cross-border investment :

- 57. International Money and Finance Russia and IM&F Central Bank (Bank of Russia) regulates monetary cross-border flows

- 59. Скачать презентацию

Слайд 3International Money and Finance IM&F Development

The Gold Standard Stage 1

Paris Conference of

International Money and Finance IM&F Development

The Gold Standard Stage 1

Paris Conference of

Слайд 4International Money and Finance IM&F Development

The Gold Standard Stage 2

Genova Conference of

International Money and Finance IM&F Development

The Gold Standard Stage 2

Genova Conference of

Слайд 5International Money and Finance IM&F Development

The Bretton Woods system (BWS)

Bretton Woods Conference

International Money and Finance IM&F Development

The Bretton Woods system (BWS)

Bretton Woods Conference

Слайд 6International Money and Finance IM&F Development

The Bretton Woods system (BWS)

Compulsory golden parities

Official

International Money and Finance IM&F Development

The Bretton Woods system (BWS)

Compulsory golden parities

Official

Слайд 7International Money and Finance IM&F Development

The Bretton Woods system (BWS)

Crisis and crush

International Money and Finance IM&F Development

The Bretton Woods system (BWS)

Crisis and crush

Слайд 8International Money and Finance IM&F Development

The Modern (Jamaica) System (JS)

Kingston (Jamaica)

International Money and Finance IM&F Development

The Modern (Jamaica) System (JS)

Kingston (Jamaica)

Слайд 9International Money and Finance IM&F Development

JS Principles:

International money – national currencies (free

International Money and Finance IM&F Development

JS Principles:

International money – national currencies (free

Слайд 10International Money and Finance

IM&F Development

End of Golden Standard System in 1970-ies

Jamaica

International Money and Finance

IM&F Development

End of Golden Standard System in 1970-ies

Jamaica

Слайд 11International Money and Finance

IM&F Development

Start of neoclassical reforms in developed economies: implications

International Money and Finance

IM&F Development

Start of neoclassical reforms in developed economies: implications

Слайд 12International Money and Finance

IM&F Development

Creation of global TNCs and globalization of their

International Money and Finance

IM&F Development

Creation of global TNCs and globalization of their

Слайд 13International Money and Finance

IM&F Development

“Booming Age” of 1990-2007, boom in financial sector

Federal

International Money and Finance

IM&F Development

“Booming Age” of 1990-2007, boom in financial sector

Federal

Слайд 14International Money and Finance

IM&F Development

Building EMU

Maastricht Treaty and its criteria

Difficulties in 1995,

International Money and Finance

IM&F Development

Building EMU

Maastricht Treaty and its criteria

Difficulties in 1995,

Слайд 15International Money and Finance

IM&F Development

IM&F system at present (pre-crisis)

Dominant position of

International Money and Finance

IM&F Development

IM&F system at present (pre-crisis)

Dominant position of

Слайд 16International Money and Finance

IM&F Development

Present IM&F: Regulators

Main central banks: FRS, ECB, BofE,

International Money and Finance

IM&F Development

Present IM&F: Regulators

Main central banks: FRS, ECB, BofE,

Слайд 17International Money and Finance

IM&F at Present:

Stimulating policy of FRS under Alan Greenspan

International Money and Finance

IM&F at Present:

Stimulating policy of FRS under Alan Greenspan

Слайд 18International Money and Finance

IM&F at Present: Stages of the Global Crisis

Mortgage crisis

International Money and Finance

IM&F at Present: Stages of the Global Crisis

Mortgage crisis

Слайд 19International Money and Finance International Monetary Fund (IMF)

Established 22.07.1944 at Bretton Woods

International Money and Finance International Monetary Fund (IMF)

Established 22.07.1944 at Bretton Woods

Слайд 20International Money and Finance IMF

The IMF was established to promote international monetary

International Money and Finance IMF

The IMF was established to promote international monetary

Слайд 21International Money and Finance IMF

Structure:

Governing Bodies:

Board of Governors

Executive Board (Directorate)

Managing Director

International Money and Finance IMF

Structure:

Governing Bodies:

Board of Governors

Executive Board (Directorate)

Managing Director

Слайд 22International Money and Finance IMF

Board of Governors

This is the highest Governing Body

International Money and Finance IMF

Board of Governors

This is the highest Governing Body

Слайд 23International Money and Finance IMF

Executive Board (Directorate)

Major function – to determine the

International Money and Finance IMF

Executive Board (Directorate)

Major function – to determine the

Слайд 24International Money and Finance IMF

Managing Director

Traditionally Western European

Christine Lagarde (France)

since 2011

after Dominique

International Money and Finance IMF

Managing Director

Traditionally Western European

Christine Lagarde (France)

since 2011

after Dominique

Слайд 25International Money and Finance IMF

The IMF gets its money principally from quota

International Money and Finance IMF

The IMF gets its money principally from quota

Слайд 26International Money and Finance

IMF

Major Facts about IMF (as of May 3,

International Money and Finance

IMF

Major Facts about IMF (as of May 3,

Слайд 27International Money and Finance IMF

International Money and Finance IMF

Слайд 28International Money and Finance

IMF

International Money and Finance

IMF

Слайд 29International Money and Finance IMF

The changing nature of IMF lending:

The volume

International Money and Finance IMF

The changing nature of IMF lending:

The volume

Слайд 30International Money and Finance IMF

IMF Lending

A core responsibility of the IMF is

International Money and Finance IMF

IMF Lending A core responsibility of the IMF is

Слайд 31International Money and Finance IMF

The process of IMF lending:

An IMF loan is

International Money and Finance IMF

The process of IMF lending:

An IMF loan is

Слайд 32International Money and Finance Exchange rate regimes

Fixed exchange rate regime based

International Money and Finance Exchange rate regimes

Fixed exchange rate regime based

Слайд 33International Money and Finance Exchange rate regimes

Fixed exchange rate regime:

Predictability of

International Money and Finance Exchange rate regimes

Fixed exchange rate regime:

Predictability of

Слайд 34International Money and Finance Exchange rate regimes

Float exchange rate regime:

More

International Money and Finance Exchange rate regimes

Float exchange rate regime:

More

Слайд 35International Money and Finance Exchange rate regimes

Factors that determine exchange rate:

Purchasing Power

International Money and Finance Exchange rate regimes

Factors that determine exchange rate:

Purchasing Power

Слайд 36International Money and Finance

Exchange rate regimes

Purchasing Power Parity (PPP):

How much of

International Money and Finance

Exchange rate regimes

Purchasing Power Parity (PPP):

How much of

Слайд 37International Money and Finance

Exchange rate regimes

The same basket of goods and

International Money and Finance

Exchange rate regimes

The same basket of goods and

Слайд 38International Money and Finance

Exchange rate regimes

Trade balance and exchange rate:

Low exchange

International Money and Finance

Exchange rate regimes

Trade balance and exchange rate:

Low exchange

Слайд 39International Money and Finance

Balance of payments

The balance of payments, (or

International Money and Finance

Balance of payments

The balance of payments, (or

Слайд 40International Money and Finance

Balance of payments

The balance, like other accounting

International Money and Finance

Balance of payments

The balance, like other accounting

Слайд 41International Money and Finance

Balance of payments

The IMF definition: "Balance of Payments

International Money and Finance

Balance of payments

The IMF definition: "Balance of Payments

Слайд 42International Money and Finance

Balance of payments

Balance of payments identity is

International Money and Finance

Balance of payments

Balance of payments identity is

Слайд 43International Money and Finance

Balance of payments

The basic principle behind the identity

International Money and Finance

Balance of payments

The basic principle behind the identity

Слайд 44International Money and Finance

Balance of payments

A balance of payments equilibrium

International Money and Finance

Balance of payments

A balance of payments equilibrium

Слайд 45International Money and Finance

USA and the GR

Fannie Mae balance sheet–simplified example,

International Money and Finance

USA and the GR

Fannie Mae balance sheet–simplified example,

Слайд 46International Money and Finance

USA and the GR

The GSEs bought about 50%

International Money and Finance

USA and the GR

The GSEs bought about 50%

Слайд 47International Money and Finance

USA and the GR

From the current handwringing, you’d

International Money and Finance

USA and the GR

From the current handwringing, you’d

Слайд 48International Money and Finance

USA and the GR

Clear need for new

International Money and Finance

USA and the GR

Clear need for new

Слайд 49International Money and Finance

USA and the GR

General upturn in US economy

International Money and Finance

USA and the GR

General upturn in US economy

Слайд 50International Money and Finance

EU and the Debt Crisis

Maastricht Treaty and its

International Money and Finance

EU and the Debt Crisis

Maastricht Treaty and its

Слайд 51International Money and Finance

EU and the Debt Crisis

Criterion 3: Inflation not

International Money and Finance

EU and the Debt Crisis

Criterion 3: Inflation not

Слайд 52International Money and Finance

EU and the Debt Crisis

By 2011: Germany and

International Money and Finance

EU and the Debt Crisis

By 2011: Germany and

Слайд 53International Money and Finance

EU and the Debt Crisis

Relatively stable: Finland, France,

International Money and Finance

EU and the Debt Crisis

Relatively stable: Finland, France,

Слайд 54International Money and Finance

EU and the Debt Crisis

Measures taken by

International Money and Finance

EU and the Debt Crisis

Measures taken by

Слайд 55International Money and Finance

Russia and IM&F

Role in IM&F institutions:

Member of IMF

International Money and Finance

Russia and IM&F

Role in IM&F institutions:

Member of IMF

Слайд 56International Money and Finance

Russia and IM&F

Russia is an active player in

International Money and Finance

Russia and IM&F

Russia is an active player in

Слайд 57International Money and Finance

Russia and IM&F

Central Bank (Bank of Russia)

International Money and Finance

Russia and IM&F

Central Bank (Bank of Russia)

Презентация по основам предпринимательства

Презентация по основам предпринимательства Ориентировочные режимы сушки строительных материалов, изделий и конструкций

Ориентировочные режимы сушки строительных материалов, изделий и конструкций Технические испытания колец LLC “NPK” “BO” - ООО “НПК” “БО”

Технические испытания колец LLC “NPK” “BO” - ООО “НПК” “БО” Аллергия

Аллергия Мадагаскар

Мадагаскар www.nikita.ru

www.nikita.ru Современный урок в начальной школе в условиях ФГОС

Современный урок в начальной школе в условиях ФГОС Детские годы Ломоносова М.В.

Детские годы Ломоносова М.В. Нормативно-правовое обеспечение деятельности частного образовательного учреждения на территории МО Котлас

Нормативно-правовое обеспечение деятельности частного образовательного учреждения на территории МО Котлас Зажигательное оружие

Зажигательное оружие Питчинг. Важность ораторского искусства

Питчинг. Важность ораторского искусства Sistema dei documenti di bilancio e iter di approvazione

Sistema dei documenti di bilancio e iter di approvazione Постный майонез

Постный майонез Решение математических и экономических задач средствами MATLAB

Решение математических и экономических задач средствами MATLAB Архитектурный облик Венеции

Архитектурный облик Венеции Основы брендинга

Основы брендинга Матричные модели качества на примере оценки деятельности кафедр

Матричные модели качества на примере оценки деятельности кафедр Звездный час

Звездный час Презентация на тему Воспитание культуры поведения

Презентация на тему Воспитание культуры поведения География как наука (1)

География как наука (1) Спортивная командная игра баскетбол

Спортивная командная игра баскетбол Политика и власть

Политика и власть Детство!

Детство! Иконы двунадесятых православных праздников

Иконы двунадесятых православных праздников Искусство общения

Искусство общения Зачем животным нужны хвосты? 5 класс

Зачем животным нужны хвосты? 5 класс Металлы и сплавы — материалы для древних

Металлы и сплавы — материалы для древних