- Korean Business and Management: Characteristics of Korean companies

Содержание

- 2. 10– KNOWLEDGE OBJECTIVES Define corporate governance and explain why it is used to monitor and control

- 3. 10– KNOWLEDGE OBJECTIVES (cont’d) Discuss the types of compensation executives receive and their effects on strategic

- 4. 10– Corporate Governance Corporate governance is: A relationship among stakeholders that is used to determine and

- 5. 11 | Risk capital – No guarantee to the stockholders that: They will recoup their investment

- 6. 11 | Stakeholders and Corporate Performance Stakeholders are in an exchange relationship with the company Contributions:

- 7. 11 | Identify stakeholders most critical to survival: Identify which stakeholders The stakeholders’ interests and concerns

- 8. 11 | Profitability, Profit Growth and Stakeholder Claims Participating in a market that is growing Taking

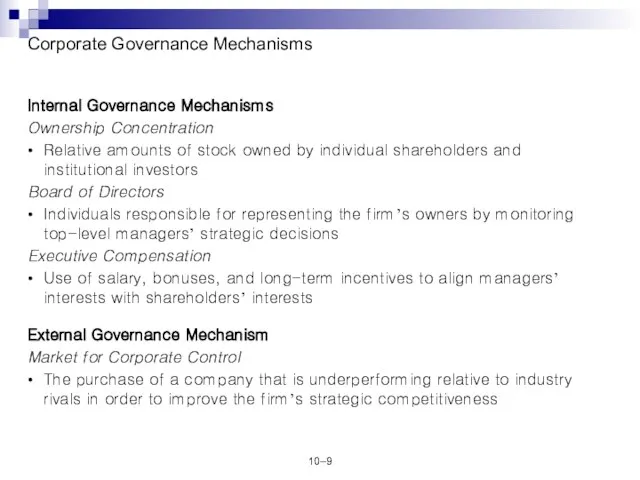

- 9. 10– Corporate Governance Mechanisms Internal Governance Mechanisms Ownership Concentration • Relative amounts of stock owned by

- 10. 11 | Governance Mechanisms Governance mechanisms serve to limit the agency problem by aligning incentives between

- 11. 10– Internal Governance Mechanisms Ownership Concentration Relative amounts of stock owned by individual shareholders and institutional

- 12. 10– Internal Governance Mechanisms (cont’d) Executive Compensation The use of salary, bonuses, and long-term incentives to

- 13. 10– Separation of Ownership and Managerial Control Basis of the modern corporation Shareholders purchase stock, becoming

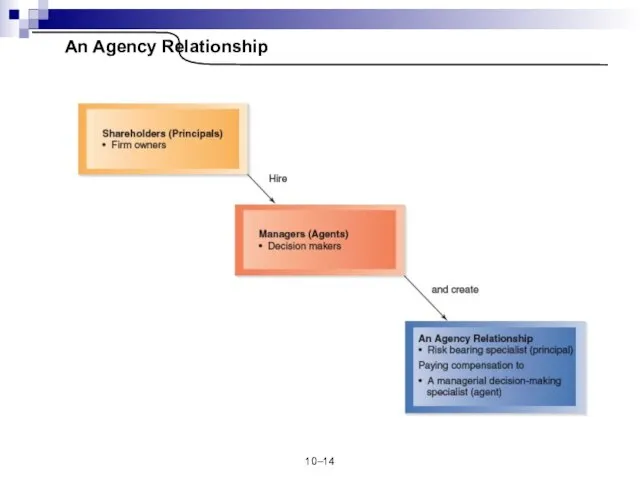

- 14. 10– An Agency Relationship

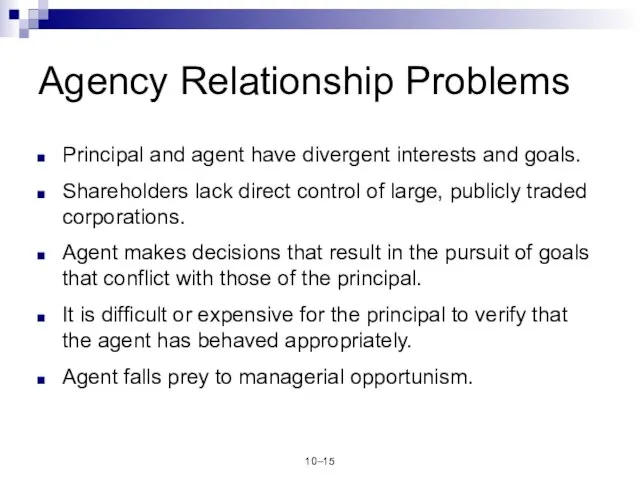

- 15. 10– Agency Relationship Problems Principal and agent have divergent interests and goals. Shareholders lack direct control

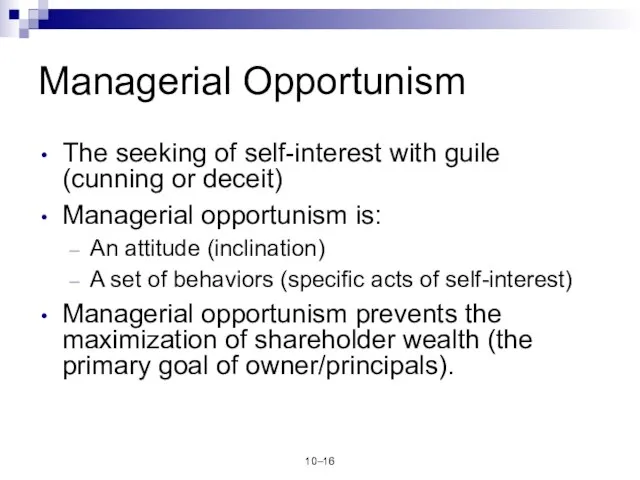

- 16. 10– Managerial Opportunism The seeking of self-interest with guile (cunning or deceit) Managerial opportunism is: An

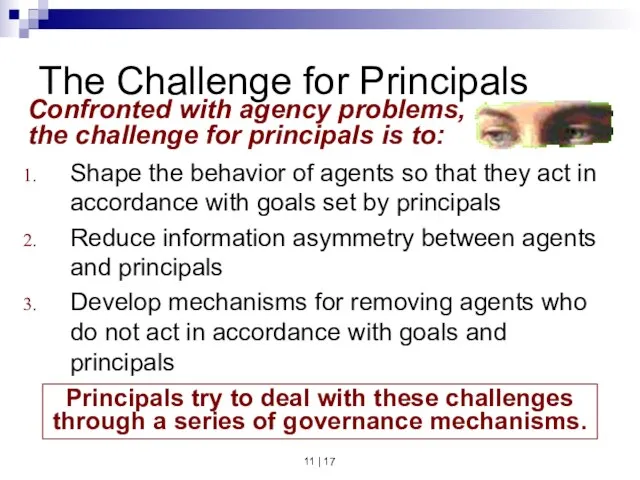

- 17. 11 | The Challenge for Principals Shape the behavior of agents so that they act in

- 18. 10– Response to Managerial Opportunism Principals do not know beforehand which agents will or will not

- 19. 10– Examples of the Agency Problem The Problem of Product Diversification Increased size, and the relationship

- 20. 10– Agency Costs and Governance Mechanisms Agency Costs The sum of incentive costs, monitoring costs, enforcement

- 21. 10– Agency Costs and Governance Mechanisms (cont’d) Boards of Directors have a fiduciary duty to shareholders

- 22. 10– Governance Mechanisms Large block shareholders have a strong incentive to monitor management closely: Their large

- 23. 10– Governance Mechanisms (cont’d) The increasing influence of institutional owners (stock mutual funds and pension funds)

- 24. INCENTIVE COMPENSATION

- 25. 10– Governance Mechanisms (cont’d) Shareholder activism: Shareholders can convene to discuss corporation’s direction. If a consensus

- 26. 10– Governance Mechanisms (cont’d) Board of directors Group of elected individuals that acts in the owners’

- 27. 10– Governance Mechanisms (cont’d) Composition of Boards: Insiders: the firm’s CEO and other top-level managers Related

- 28. 10– Governance Mechanisms (cont’d) Criticisms of Boards of Directors include: Too readily approve managers’ self-serving initiatives

- 29. 10– Governance Mechanisms (cont’d) Enhancing the effectiveness of boards and directors: More diversity in the backgrounds

- 30. 10– Governance Mechanisms (cont’d) Forms of compensation: Salaries, bonuses, long-term performance incentives, stock awards, stock options

- 31. 10– Governance Mechanisms (cont’d) Individuals and firms buy or take over undervalued corporations. Ineffective managers are

- 32. THE MARKET FOR CORPORATE CONTROL

- 33. 10– Governance Mechanisms (cont’d) Managerial defense tactics increase the costs of mounting a takeover Defense tactics

- 34. 10– The General Environment: Segments and Elements Defense strategy Category Popularity Effectiveness Stockholder among firms as

- 35. 10– International Corporate Governance Germany Owner and manager are often the same in private firms. Public

- 36. 10– Responsible for the functions of direction and management Responsible for appointing members to the Vorstand

- 37. 10– International Corporate Governance (cont’d) Japan Important governance factors: Obligation “Family” Consensus Keiretsus: strongly interrelated groups

- 38. 10– International Corporate Governance (cont’d) Japan (cont’d) Other governance characteristics: Powerful government intervention Close relationships between

- 39. CORPORATE GOVERNANCE: U.S VS. JAPAN Owner-manager relationship Manager and shareholder relationship Ownership concentration U.S Adversarial Through

- 40. 10– International Corporate Governance (cont’d) Global Corporate Governance Organizations worldwide are adopting a relatively uniform governance

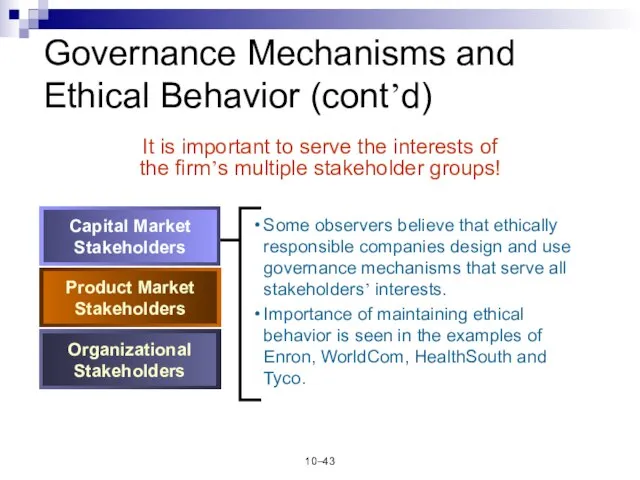

- 41. 10– Governance Mechanisms and Ethical Behavior It is important to serve the interests of the firm’s

- 42. 10– Governance Mechanisms and Ethical Behavior (cont’d) Product market stakeholders (customers, suppliers and host communities) and

- 43. 10– Governance Mechanisms and Ethical Behavior (cont’d) It is important to serve the interests of the

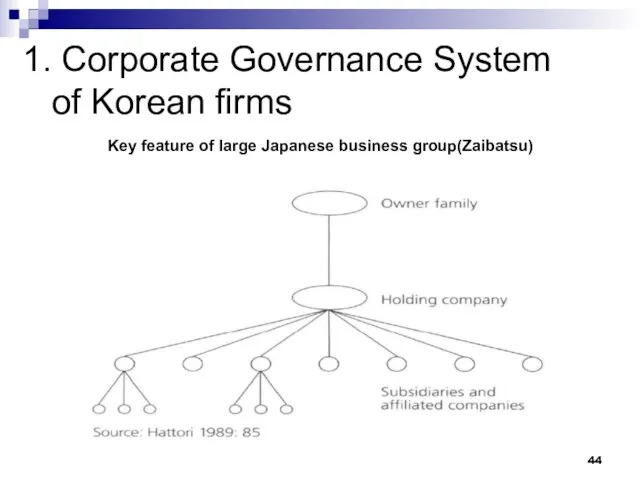

- 44. 1. Corporate Governance System of Korean firms Key feature of large Japanese business group(Zaibatsu)

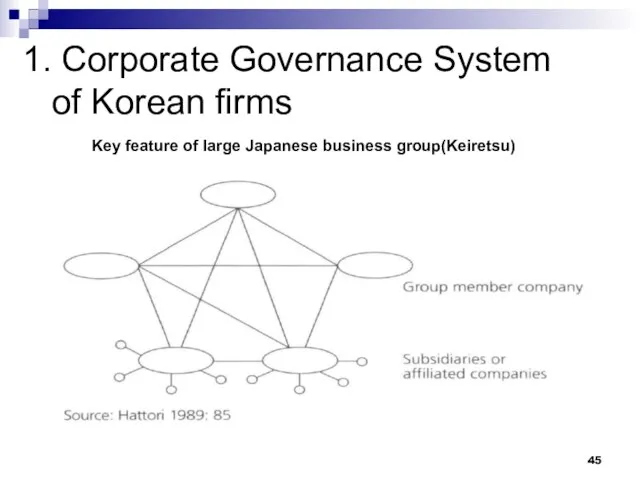

- 45. 1. Corporate Governance System of Korean firms Key feature of large Japanese business group(Keiretsu)

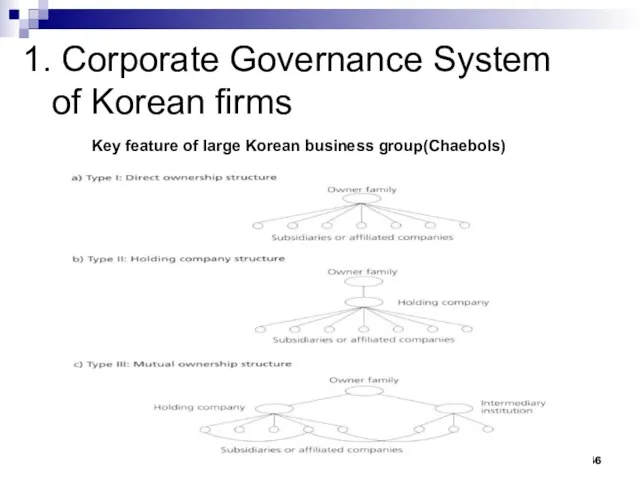

- 46. 1. Corporate Governance System of Korean firms Key feature of large Korean business group(Chaebols)

- 47. 2. Corporate governance issues related to Korean Chaebols What has made Chaebol’s ownership structure survive for

- 48. 3. Controversies around Chaebol corporate governance Chaebol’s family owns on average 3% of ownership of their

- 49. 3. Controversies around Chaebol corporate governance (cont.) Government attitude toward Chaebol recently dramatically changed after the

- 51. Скачать презентацию

Слайд 310–

KNOWLEDGE OBJECTIVES (cont’d)

Discuss the types of compensation executives receive and their effects

10–

KNOWLEDGE OBJECTIVES (cont’d)

Discuss the types of compensation executives receive and their effects

Слайд 410–

Corporate Governance

Corporate governance is:

A relationship among stakeholders that is used to determine

10–

Corporate Governance

Corporate governance is:

A relationship among stakeholders that is used to determine

Слайд 511 |

Risk capital –

No guarantee to the stockholders that:

They

11 |

Risk capital –

No guarantee to the stockholders that:

They

Слайд 611 |

Stakeholders and Corporate Performance

Stakeholders are in an exchange relationship

11 |

Stakeholders and Corporate Performance

Stakeholders are in an exchange relationship

Слайд 711 |

Identify stakeholders most critical to survival:

Identify which stakeholders

The stakeholders’

11 |

Identify stakeholders most critical to survival:

Identify which stakeholders

The stakeholders’

Слайд 811 |

Profitability, Profit Growth and Stakeholder Claims

Participating in a market that

11 |

Profitability, Profit Growth and Stakeholder Claims

Participating in a market that

Слайд 910–

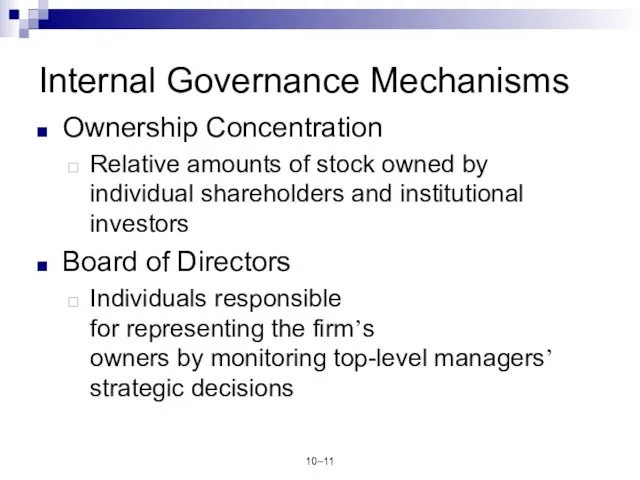

Corporate Governance Mechanisms

Internal Governance Mechanisms

Ownership Concentration

• Relative amounts of stock owned by individual

10–

Corporate Governance Mechanisms

Internal Governance Mechanisms

Ownership Concentration

• Relative amounts of stock owned by individual

Слайд 1011 |

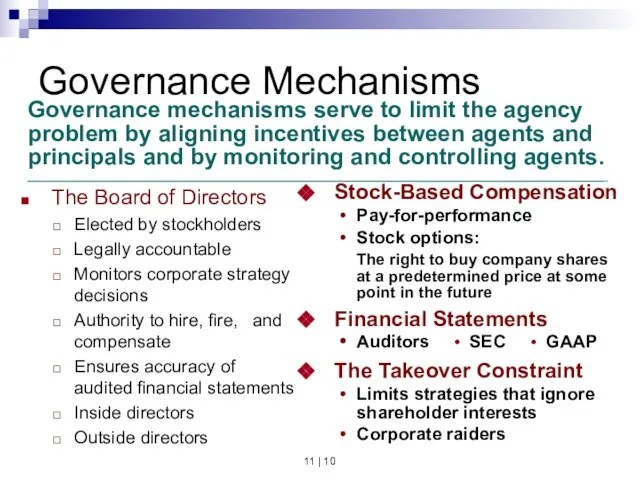

Governance Mechanisms

Governance mechanisms serve to limit the agency problem by

11 |

Governance Mechanisms

Governance mechanisms serve to limit the agency problem by

Слайд 1110–

Internal Governance Mechanisms

Ownership Concentration

Relative amounts of stock owned by individual shareholders and

10–

Internal Governance Mechanisms

Ownership Concentration

Relative amounts of stock owned by individual shareholders and

Слайд 1210–

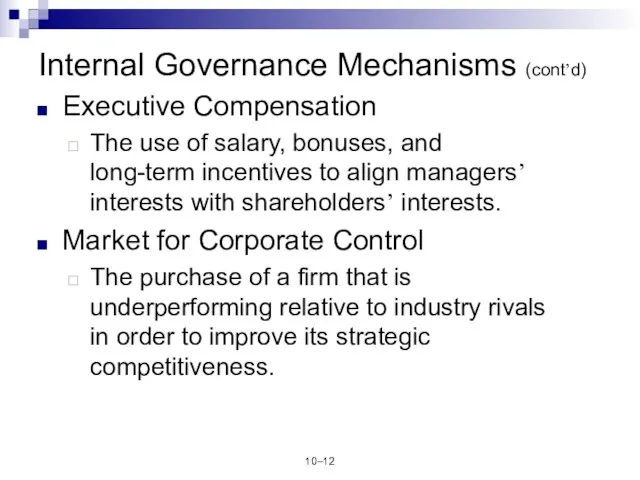

Internal Governance Mechanisms (cont’d)

Executive Compensation

The use of salary, bonuses, and long-term incentives

10–

Internal Governance Mechanisms (cont’d)

Executive Compensation

The use of salary, bonuses, and long-term incentives

Слайд 1310–

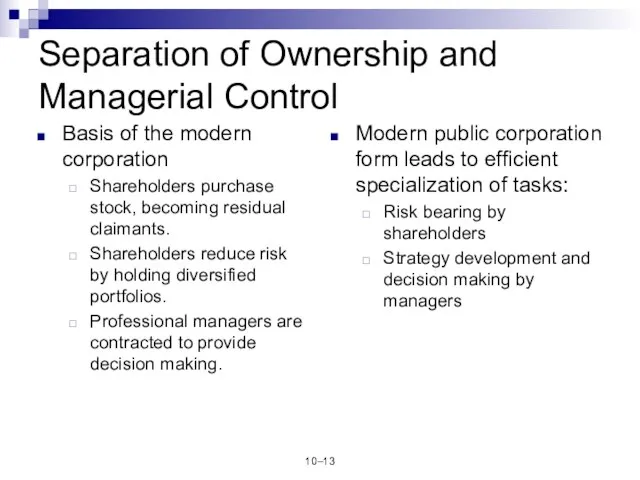

Separation of Ownership and Managerial Control

Basis of the modern corporation

Shareholders purchase stock,

10–

Separation of Ownership and Managerial Control

Basis of the modern corporation

Shareholders purchase stock,

Слайд 1410–

An Agency Relationship

10–

An Agency Relationship

Слайд 1510–

Agency Relationship Problems

Principal and agent have divergent interests and goals.

Shareholders lack direct

10–

Agency Relationship Problems

Principal and agent have divergent interests and goals.

Shareholders lack direct

Слайд 1610–

Managerial Opportunism

The seeking of self-interest with guile (cunning or deceit)

Managerial opportunism is:

An

10–

Managerial Opportunism

The seeking of self-interest with guile (cunning or deceit)

Managerial opportunism is:

An

Слайд 1711 |

The Challenge for Principals

Shape the behavior of agents so that

11 |

The Challenge for Principals

Shape the behavior of agents so that

Слайд 1810–

Response to Managerial Opportunism

Principals do not know beforehand which agents will or

10–

Response to Managerial Opportunism

Principals do not know beforehand which agents will or

Слайд 1910–

Examples of the Agency Problem

The Problem of Product Diversification

Increased size, and the

10–

Examples of the Agency Problem

The Problem of Product Diversification

Increased size, and the

Слайд 2010–

Agency Costs and Governance Mechanisms

Agency Costs

The sum of incentive costs, monitoring costs,

10–

Agency Costs and Governance Mechanisms

Agency Costs

The sum of incentive costs, monitoring costs,

Слайд 2110–

Agency Costs and Governance Mechanisms (cont’d)

Boards of Directors have a fiduciary duty

10–

Agency Costs and Governance Mechanisms (cont’d)

Boards of Directors have a fiduciary duty

Слайд 2210–

Governance Mechanisms

Large block shareholders have a strong incentive to monitor management closely:

Their

10–

Governance Mechanisms

Large block shareholders have a strong incentive to monitor management closely:

Their

Слайд 2310–

Governance Mechanisms (cont’d)

The increasing influence of institutional owners (stock mutual funds and

10–

Governance Mechanisms (cont’d)

The increasing influence of institutional owners (stock mutual funds and

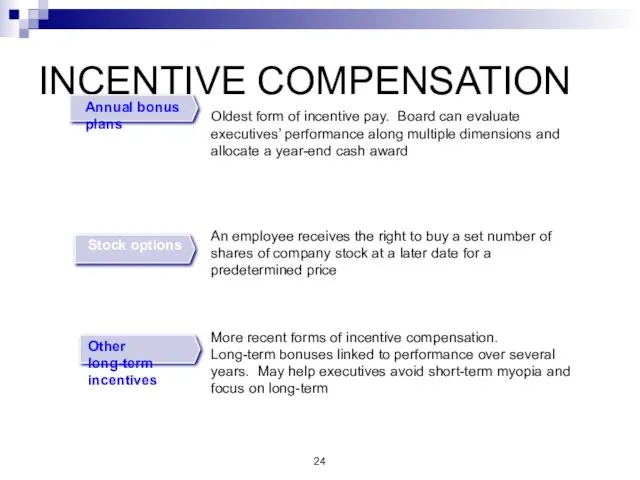

Слайд 24INCENTIVE COMPENSATION

INCENTIVE COMPENSATION

Слайд 2510–

Governance Mechanisms (cont’d)

Shareholder activism:

Shareholders can convene to discuss corporation’s direction.

If a consensus

10–

Governance Mechanisms (cont’d)

Shareholder activism:

Shareholders can convene to discuss corporation’s direction.

If a consensus

Слайд 2610–

Governance Mechanisms (cont’d)

Board of directors

Group of elected individuals that acts in the

10–

Governance Mechanisms (cont’d)

Board of directors

Group of elected individuals that acts in the

Слайд 2710–

Governance Mechanisms (cont’d)

Composition of Boards:

Insiders: the firm’s CEO and other top-level managers

Related

10–

Governance Mechanisms (cont’d)

Composition of Boards:

Insiders: the firm’s CEO and other top-level managers

Related

Слайд 2810–

Governance Mechanisms (cont’d)

Criticisms of Boards of Directors include:

Too readily approve managers’ self-serving

10–

Governance Mechanisms (cont’d)

Criticisms of Boards of Directors include:

Too readily approve managers’ self-serving

Слайд 2910–

Governance Mechanisms (cont’d)

Enhancing the effectiveness of boards and directors:

More diversity in the

10–

Governance Mechanisms (cont’d)

Enhancing the effectiveness of boards and directors:

More diversity in the

Слайд 3010–

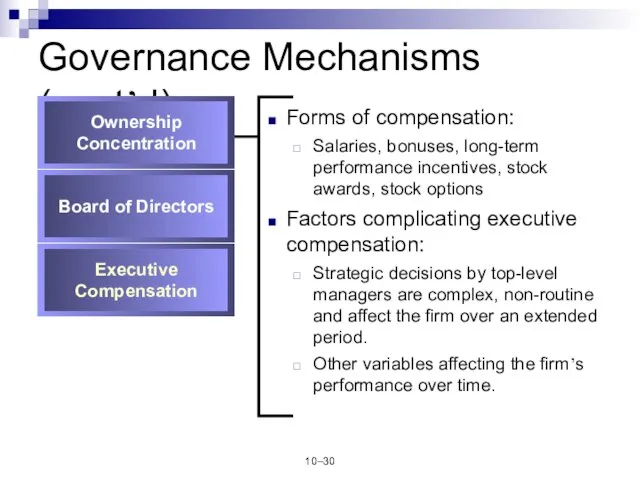

Governance Mechanisms (cont’d)

Forms of compensation:

Salaries, bonuses, long-term performance incentives, stock awards, stock

10–

Governance Mechanisms (cont’d)

Forms of compensation:

Salaries, bonuses, long-term performance incentives, stock awards, stock

Слайд 3110–

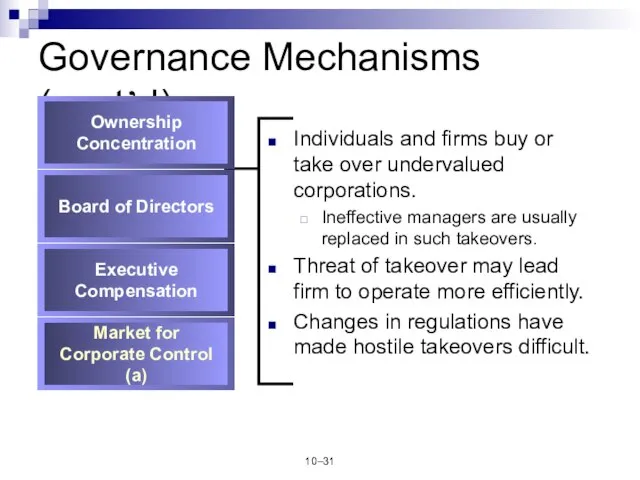

Governance Mechanisms (cont’d)

Individuals and firms buy or take over undervalued corporations.

Ineffective managers

10–

Governance Mechanisms (cont’d)

Individuals and firms buy or take over undervalued corporations.

Ineffective managers

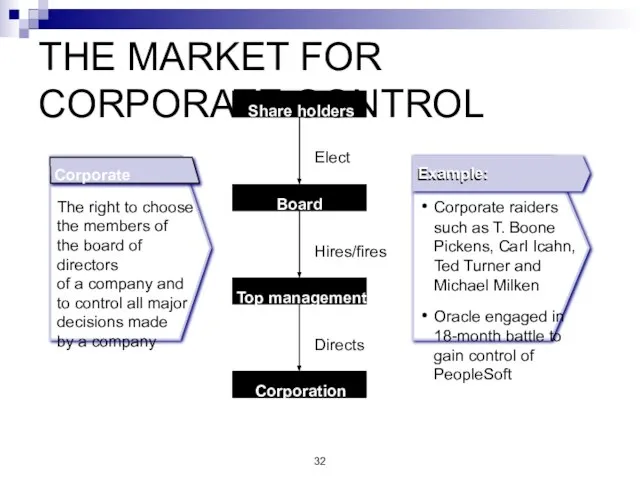

Слайд 32THE MARKET FOR CORPORATE CONTROL

THE MARKET FOR CORPORATE CONTROL

Слайд 3310–

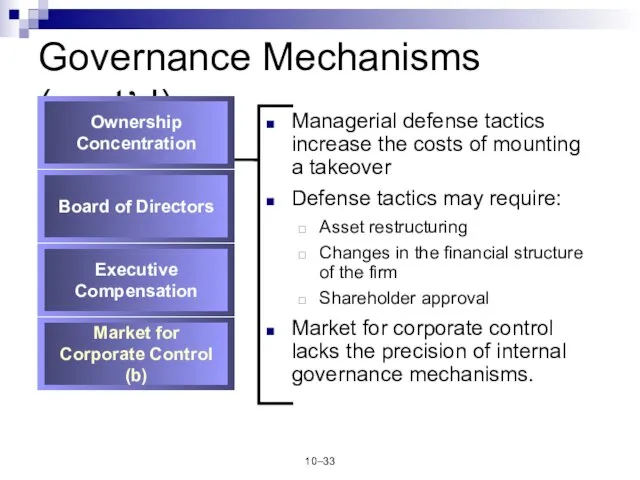

Governance Mechanisms (cont’d)

Managerial defense tactics increase the costs of mounting a takeover

Defense

10–

Governance Mechanisms (cont’d)

Managerial defense tactics increase the costs of mounting a takeover

Defense

Слайд 3410–

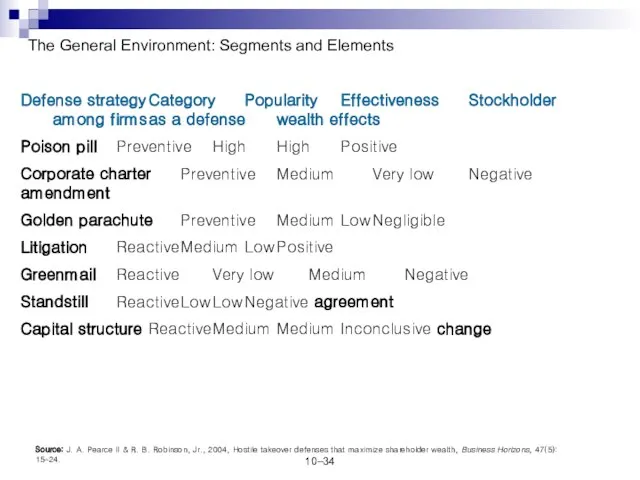

The General Environment: Segments and Elements

Defense strategy Category Popularity Effectiveness Stockholder among firms as a defense wealth effects

Poison pill Preventive

10–

The General Environment: Segments and Elements

Defense strategy Category Popularity Effectiveness Stockholder among firms as a defense wealth effects

Poison pill Preventive

Слайд 3510–

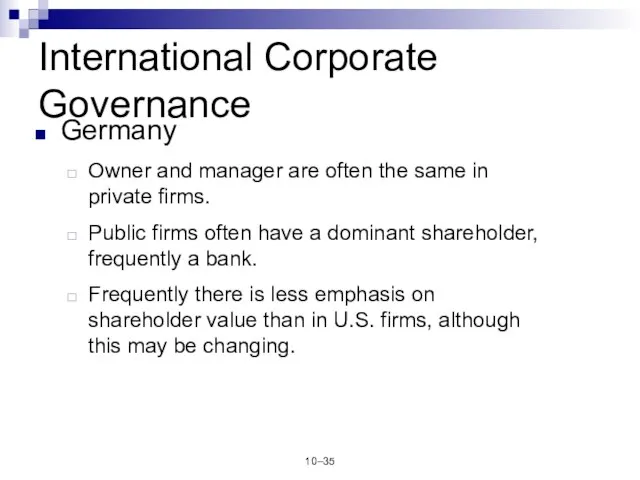

International Corporate Governance

Germany

Owner and manager are often the same in private firms.

Public

10–

International Corporate Governance

Germany

Owner and manager are often the same in private firms.

Public

Слайд 3610–

Responsible for the functions of direction and management

Responsible for appointing members

10–

Responsible for the functions of direction and management

Responsible for appointing members

Слайд 3710–

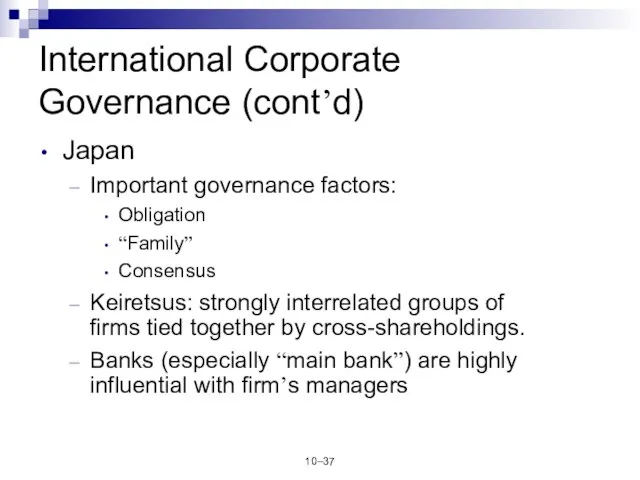

International Corporate Governance (cont’d)

Japan

Important governance factors:

Obligation

“Family”

Consensus

Keiretsus: strongly interrelated groups of firms tied

10–

International Corporate Governance (cont’d)

Japan

Important governance factors:

Obligation

“Family”

Consensus

Keiretsus: strongly interrelated groups of firms tied

Слайд 3810–

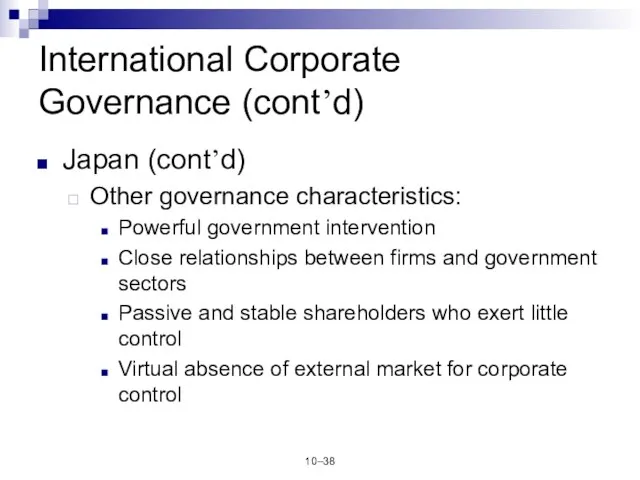

International Corporate Governance (cont’d)

Japan (cont’d)

Other governance characteristics:

Powerful government intervention

Close relationships between firms

10–

International Corporate Governance (cont’d)

Japan (cont’d)

Other governance characteristics:

Powerful government intervention

Close relationships between firms

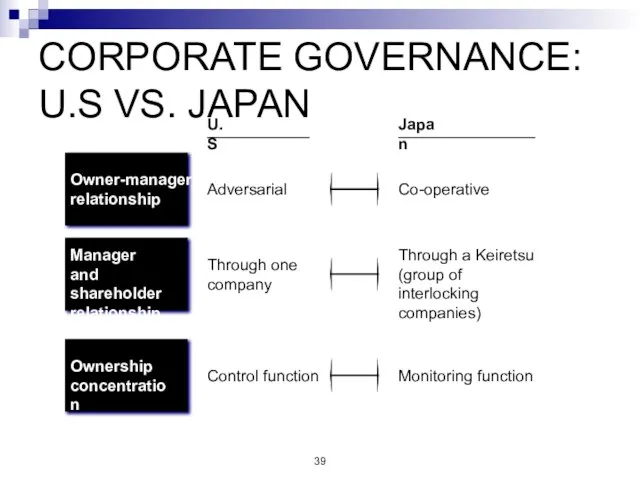

Слайд 39CORPORATE GOVERNANCE: U.S VS. JAPAN

Owner-manager

relationship

Manager and

shareholder

relationship

Ownership

concentration

U.S

Adversarial

Through one

company

Control function

Japan

Co-operative

Through a Keiretsu

(group of

CORPORATE GOVERNANCE: U.S VS. JAPAN

Owner-manager

relationship

Manager and

shareholder

relationship

Ownership

concentration

U.S

Adversarial

Through one

company

Control function

Japan

Co-operative

Through a Keiretsu (group of

Слайд 4010–

International Corporate Governance (cont’d)

Global Corporate Governance

Organizations worldwide are adopting a relatively uniform

10–

International Corporate Governance (cont’d)

Global Corporate Governance

Organizations worldwide are adopting a relatively uniform

Слайд 4110–

Governance Mechanisms and Ethical Behavior

It is important to serve the interests of

10–

Governance Mechanisms and Ethical Behavior

It is important to serve the interests of

Слайд 4210–

Governance Mechanisms and

Ethical Behavior (cont’d)

Product market stakeholders (customers, suppliers and host

10–

Governance Mechanisms and

Ethical Behavior (cont’d)

Product market stakeholders (customers, suppliers and host

Слайд 4310–

Governance Mechanisms and

Ethical Behavior (cont’d)

It is important to serve the interests

10–

Governance Mechanisms and

Ethical Behavior (cont’d)

It is important to serve the interests

Слайд 441. Corporate Governance System of Korean firms

Key feature of large Japanese business

1. Corporate Governance System of Korean firms

Key feature of large Japanese business

Слайд 451. Corporate Governance System of Korean firms

Key feature of large Japanese business

1. Corporate Governance System of Korean firms

Key feature of large Japanese business

Слайд 461. Corporate Governance System of Korean firms

Key feature of large Korean business

1. Corporate Governance System of Korean firms

Key feature of large Korean business

Слайд 472. Corporate governance issues related to Korean Chaebols

What has made Chaebol’s ownership

2. Corporate governance issues related to Korean Chaebols

What has made Chaebol’s ownership

Слайд 483. Controversies around Chaebol corporate governance

Chaebol’s family owns on average 3% of

3. Controversies around Chaebol corporate governance

Chaebol’s family owns on average 3% of

Слайд 493. Controversies around Chaebol corporate governance (cont.)

Government attitude toward Chaebol recently dramatically

3. Controversies around Chaebol corporate governance (cont.)

Government attitude toward Chaebol recently dramatically

Собор Парижской Богоматери. Франция - родина готической архитектуры

Собор Парижской Богоматери. Франция - родина готической архитектуры Паркет Europa

Паркет Europa О подготовке образовательных учреждений города Лангепаса к началу 2012-2013 учебного года

О подготовке образовательных учреждений города Лангепаса к началу 2012-2013 учебного года Тайна Шекспира

Тайна Шекспира Торнадо любви. Направление Личные Цели

Торнадо любви. Направление Личные Цели Who took the cookie from the cookie jar

Who took the cookie from the cookie jar Сказка «Волшебное число»

Сказка «Волшебное число» My giant nerd boyfriend

My giant nerd boyfriend Роль системы развития персонала организации

Роль системы развития персонала организации Цифровая подстанция - важный элемент интеллектуальной энергосистемы

Цифровая подстанция - важный элемент интеллектуальной энергосистемы Как работают экономисты

Как работают экономисты «Вода – капля жизни» Участники: Дети и родители Воспитатели: Андреева Янина Евгеньевна

«Вода – капля жизни» Участники: Дети и родители Воспитатели: Андреева Янина Евгеньевна Жемчужины Республики Марий Эл

Жемчужины Республики Марий Эл Социальная напряжённость

Социальная напряжённость Метрологическое обеспечение технологического процесса изготовления продукции

Метрологическое обеспечение технологического процесса изготовления продукции Технологии разработки проектов, программ и требования к их реализации

Технологии разработки проектов, программ и требования к их реализации Построение чертежа фартука

Построение чертежа фартука Финансовая отчетностьв реальном времени.

Финансовая отчетностьв реальном времени. Кислоты 11 класс

Кислоты 11 класс Внутреннее строение рыб

Внутреннее строение рыб Автоматизация АОСЧ

Автоматизация АОСЧ М.А.Шолохов

М.А.Шолохов Гармония образа

Гармония образа Словарик горнорудных профессий

Словарик горнорудных профессий План «Барбаросса» предполагал «блицкриг» - т.е. рассчитан на молниеносную войну в течение нескольких месяцевБарбароссаблицкриг.

План «Барбаросса» предполагал «блицкриг» - т.е. рассчитан на молниеносную войну в течение нескольких месяцевБарбароссаблицкриг. Гражданское общество и правовое государство. 9 класс

Гражданское общество и правовое государство. 9 класс Конкурс чтецов, посвящённый творчеству Э. Асадова

Конкурс чтецов, посвящённый творчеству Э. Асадова СГУ им. Чернышевского

СГУ им. Чернышевского