- Session 4_Investment Decision Tools

Содержание

- 2. Measuring investment worth Several methods of evaluating investment projects are used by financial managers, including: Payback

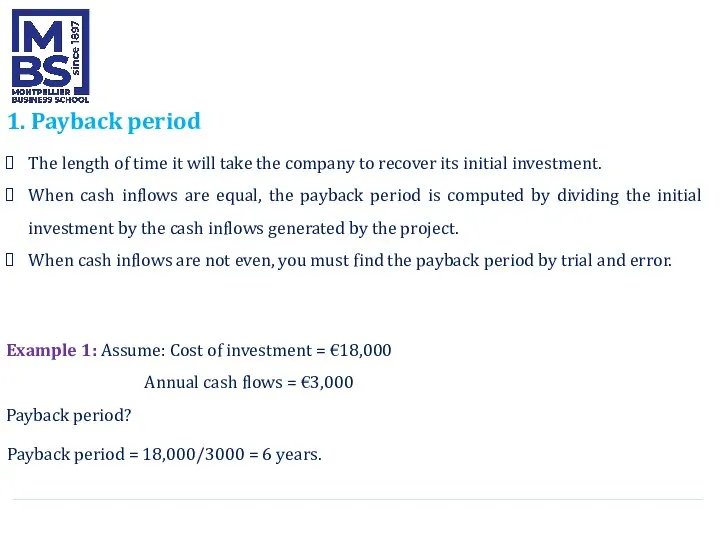

- 3. 1. Payback period The length of time it will take the company to recover its initial

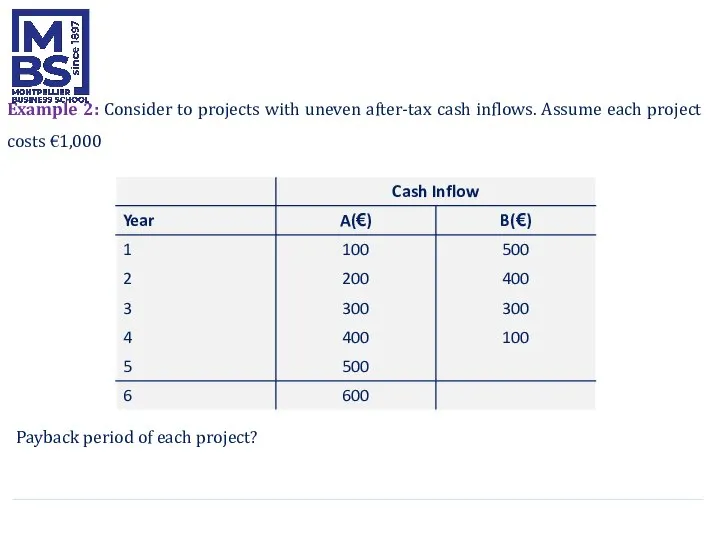

- 4. Example 2: Consider to projects with uneven after-tax cash inflows. Assume each project costs €1,000 Payback

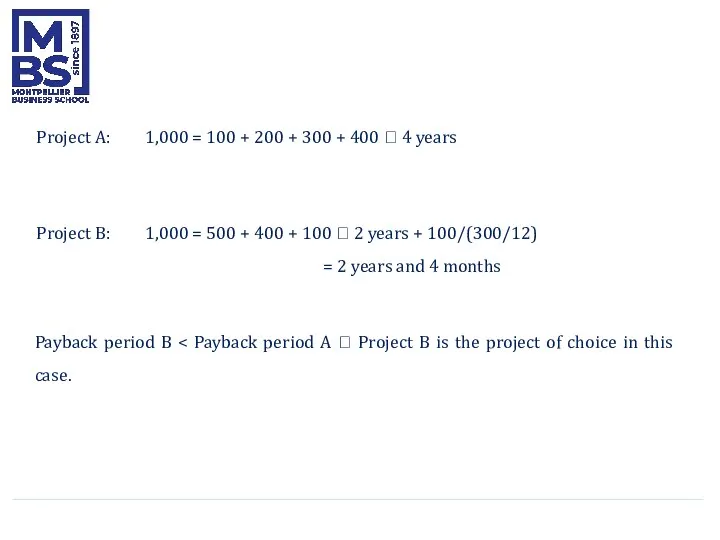

- 5. Project A: 1,000 = 100 + 200 + 300 + 400 ? 4 years Project B:

- 6. 2. Net present Value (NPV) The NPV is the excess of the present value (PV) of

- 7. Example 3: Consider the following investment: Initial investment = €12,950 Estimated life = 10 years, Annual

- 8. 3. Internal rate of return (IRR) The IRR is defined as the rate that equates the

- 10. 3.1. Applying the IRR rule The IRR investment rule will give the correct answer (that is,

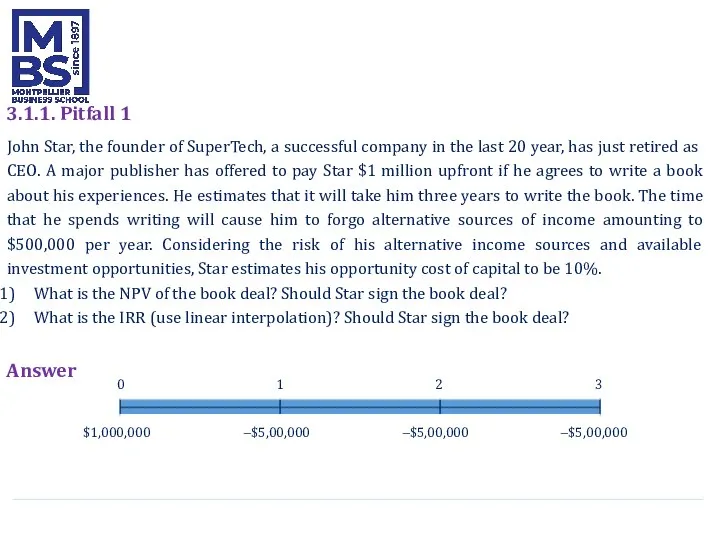

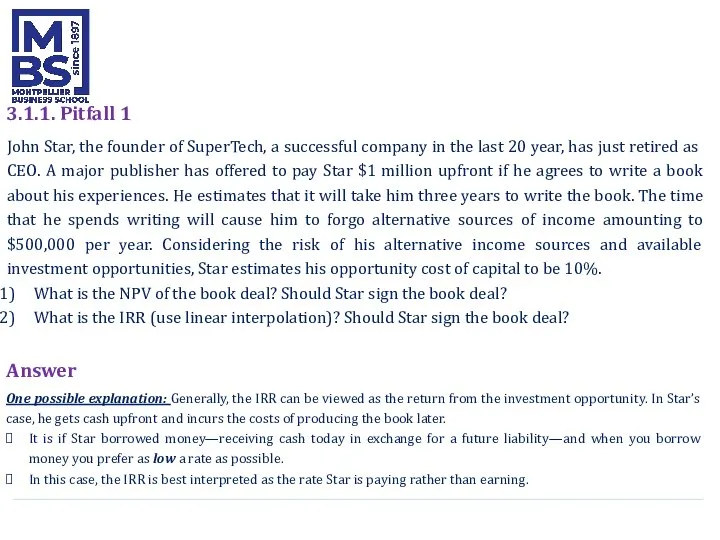

- 11. 3.1.1. Pitfall 1 John Star, the founder of SuperTech, a successful company in the last 20

- 12. 3.1.1. Pitfall 1 John Star, the founder of SuperTech, a successful company in the last 20

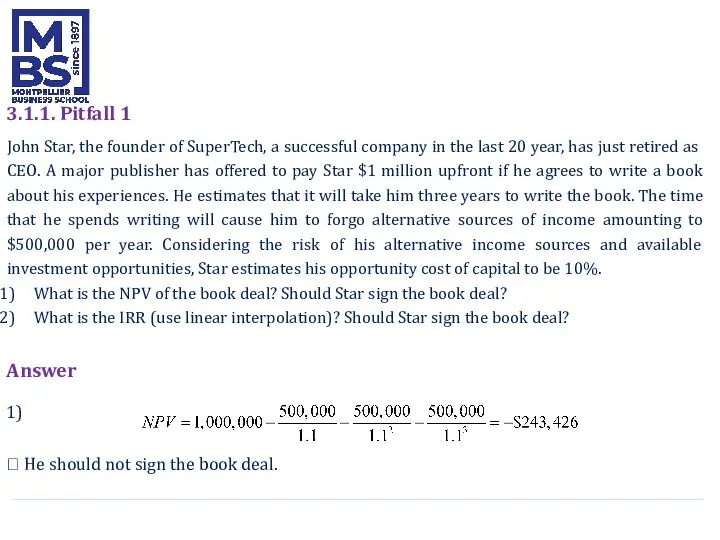

- 13. 3.1.1. Pitfall 1 John Star, the founder of SuperTech, a successful company in the last 20

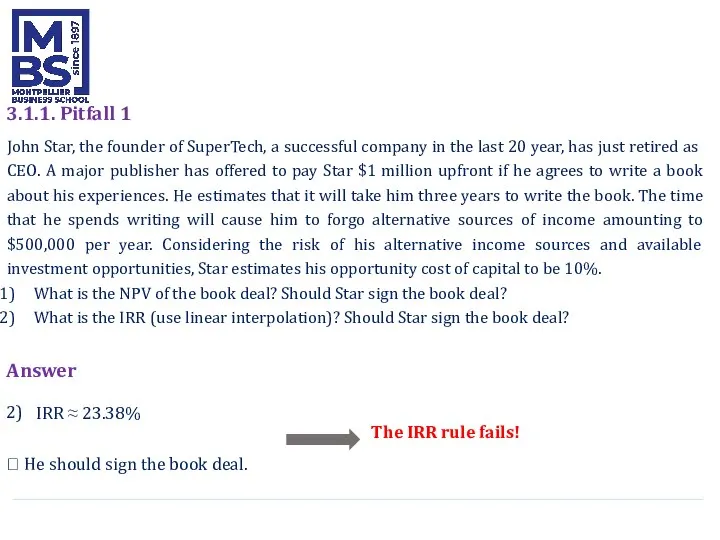

- 14. 3.1.1. Pitfall 1 John Star, the founder of SuperTech, a successful company in the last 20

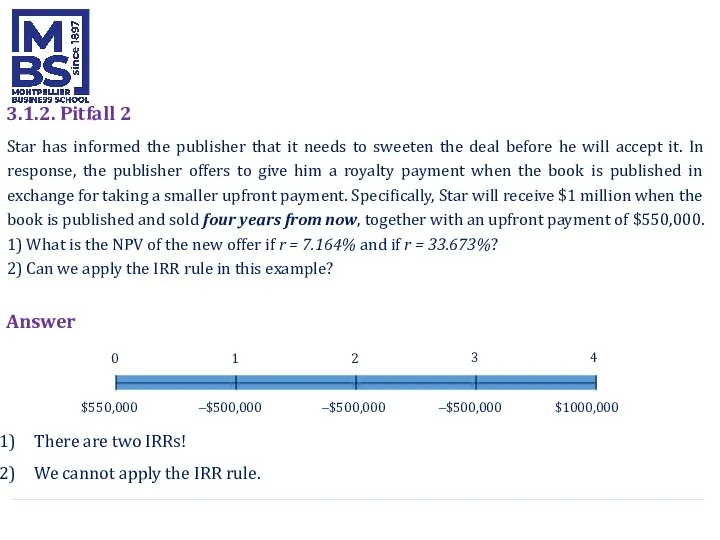

- 15. 3.1.2. Pitfall 2 Star has informed the publisher that it needs to sweeten the deal before

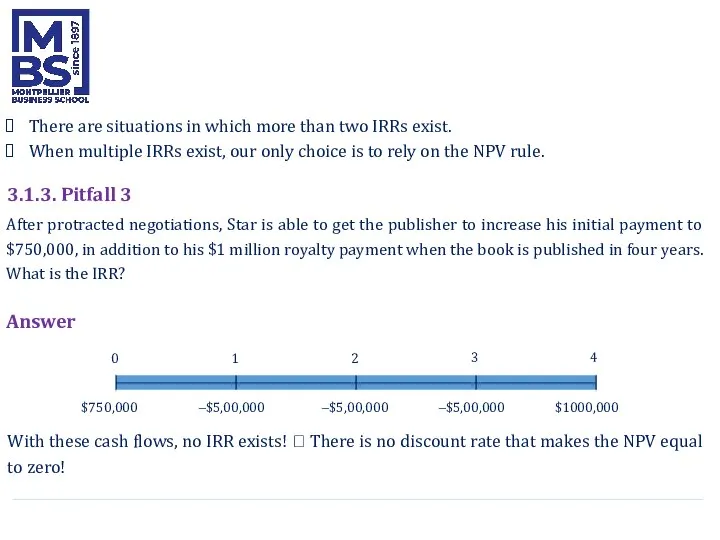

- 16. There are situations in which more than two IRRs exist. When multiple IRRs exist, our only

- 17. Exercise 1 You are considering investing in a project at a cost of $350,000. You expect

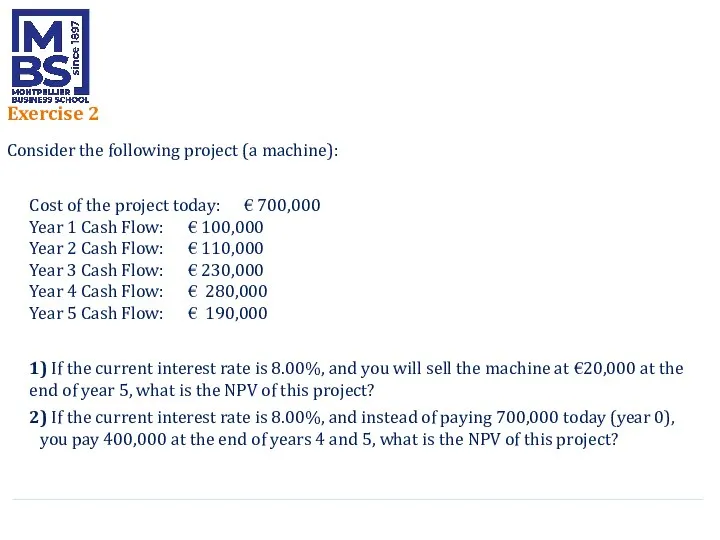

- 18. Exercise 2 Consider the following project (a machine): Cost of the project today: € 700,000 Year

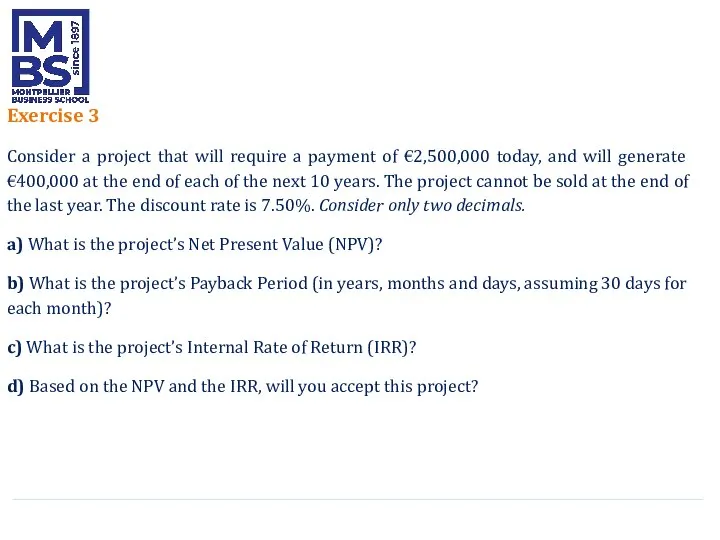

- 19. Exercise 3 Consider a project that will require a payment of €2,500,000 today, and will generate

- 21. Скачать презентацию

Слайд 2Measuring investment worth

Several methods of evaluating investment projects are used by financial

Measuring investment worth

Several methods of evaluating investment projects are used by financial

Слайд 31. Payback period

The length of time it will take the company to

1. Payback period

The length of time it will take the company to

Слайд 4Example 2: Consider to projects with uneven after-tax cash inflows. Assume each

Example 2: Consider to projects with uneven after-tax cash inflows. Assume each

Слайд 5Project A:

1,000 = 100 + 200 + 300 + 400 ? 4

Project A:

1,000 = 100 + 200 + 300 + 400 ? 4

Слайд 62. Net present Value (NPV)

The NPV is the excess of the present

2. Net present Value (NPV)

The NPV is the excess of the present

Слайд 7Example 3: Consider the following investment:

Initial investment = €12,950

Estimated life = 10

Example 3: Consider the following investment:

Initial investment = €12,950

Estimated life = 10

Слайд 83. Internal rate of return (IRR)

The IRR is defined as the rate

3. Internal rate of return (IRR)

The IRR is defined as the rate

Слайд 103.1. Applying the IRR rule

The IRR investment rule will give the correct

3.1. Applying the IRR rule

The IRR investment rule will give the correct

Слайд 113.1.1. Pitfall 1

John Star, the founder of SuperTech, a successful company in

3.1.1. Pitfall 1

John Star, the founder of SuperTech, a successful company in

Слайд 123.1.1. Pitfall 1

John Star, the founder of SuperTech, a successful company in

3.1.1. Pitfall 1

John Star, the founder of SuperTech, a successful company in

Слайд 133.1.1. Pitfall 1

John Star, the founder of SuperTech, a successful company in

3.1.1. Pitfall 1

John Star, the founder of SuperTech, a successful company in

Слайд 143.1.1. Pitfall 1

John Star, the founder of SuperTech, a successful company in

3.1.1. Pitfall 1

John Star, the founder of SuperTech, a successful company in

Слайд 153.1.2. Pitfall 2

Star has informed the publisher that it needs to sweeten

3.1.2. Pitfall 2

Star has informed the publisher that it needs to sweeten

Слайд 16There are situations in which more than two IRRs exist.

When multiple IRRs

There are situations in which more than two IRRs exist.

When multiple IRRs

Слайд 17Exercise 1

You are considering investing in a project at a cost of

Exercise 1

You are considering investing in a project at a cost of

Слайд 18Exercise 2

Consider the following project (a machine):

Cost of the project today:

Exercise 2

Consider the following project (a machine):

Cost of the project today:

Слайд 19Exercise 3

Consider a project that will require a payment of €2,500,000 today,

Exercise 3

Consider a project that will require a payment of €2,500,000 today,

Проект:«Права и обязанности членов семьи»

Проект:«Права и обязанности членов семьи» Презентация на тему Свойства корня n-ой степени (11 класс)

Презентация на тему Свойства корня n-ой степени (11 класс) КМРСО г.Красноярск Солянкина Наталья Леонидовна Голубева Людмила Матвеевна Центр мониторинга качества образования ККИПКиППРО

КМРСО г.Красноярск Солянкина Наталья Леонидовна Голубева Людмила Матвеевна Центр мониторинга качества образования ККИПКиППРО Презентация на тему Обычаи и традиции русского народа

Презентация на тему Обычаи и традиции русского народа Система управления персоналом

Система управления персоналом Презентация на тему Великобритания: конец Викторианской эпохи

Презентация на тему Великобритания: конец Викторианской эпохи  Основные ценности городского сообщества Тольятти Докладчик: Иглин В.Б. Школа № 93. Автозаводской район Тольятти 26 декабря 2010 год

Основные ценности городского сообщества Тольятти Докладчик: Иглин В.Б. Школа № 93. Автозаводской район Тольятти 26 декабря 2010 год Лекция №10-11 (Метод Тестирования) (1)

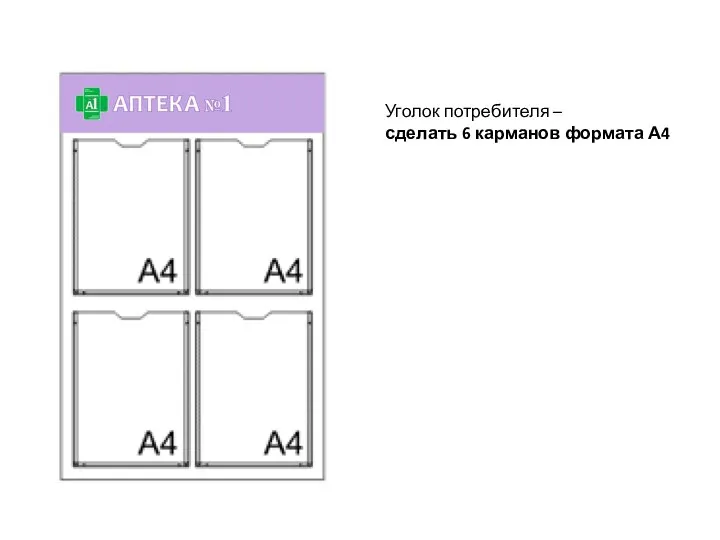

Лекция №10-11 (Метод Тестирования) (1) Уголок потребителя

Уголок потребителя Защита Отечества — священный долг

Защита Отечества — священный долг Монархи-2017

Монархи-2017 Архитектурные элементы здания

Архитектурные элементы здания Консалтинг-центр по НИДШ

Консалтинг-центр по НИДШ Экстремизм - угроза обществу

Экстремизм - угроза обществу Прямое и переносное значение слов

Прямое и переносное значение слов Фоторяд "Дети войны"

Фоторяд "Дети войны" Инструменты, механизмы, приспособления и инвентарь для выполнения штукатурных работ

Инструменты, механизмы, приспособления и инвентарь для выполнения штукатурных работ Александр Сергеевич Пушкин

Александр Сергеевич Пушкин ОСНОВНЫЕ КОМПОНЕНТЫ И УЗЛЫ ЭЛЕКТРОННЫХ УСТРОЙСТВ

ОСНОВНЫЕ КОМПОНЕНТЫ И УЗЛЫ ЭЛЕКТРОННЫХ УСТРОЙСТВ  Методы селекции растений 11 класс

Методы селекции растений 11 класс Музей Ф.М. Достоевского

Музей Ф.М. Достоевского  Альбом «МОЯ СЕМЬЯ»

Альбом «МОЯ СЕМЬЯ» Метеоролог

Метеоролог Каменный лес

Каменный лес Развивающая эстетика – новый предмет в школьном образовании

Развивающая эстетика – новый предмет в школьном образовании Революционное народничество: идеология, практика, последствия.

Революционное народничество: идеология, практика, последствия. 5 этап командный 15.12.2011ТУРНИРкоманд или индивидуальных участников 9-11 классов по решению «монстров С6»

5 этап командный 15.12.2011ТУРНИРкоманд или индивидуальных участников 9-11 классов по решению «монстров С6» Презентация на тему Храмы России

Презентация на тему Храмы России