- Financial Innovation and Financial Engineering

Содержание

- 2. LITERATURE: Financial markets and institutions / Peter Howells and Keith Bain. — Pearson Education. — 5th

- 3. Financial market. Revision Financial market is a mechanism that allows people to easily buy and sell

- 4. The financial markets can be divided into different subtypes: 1. Capital markets which consist of: *

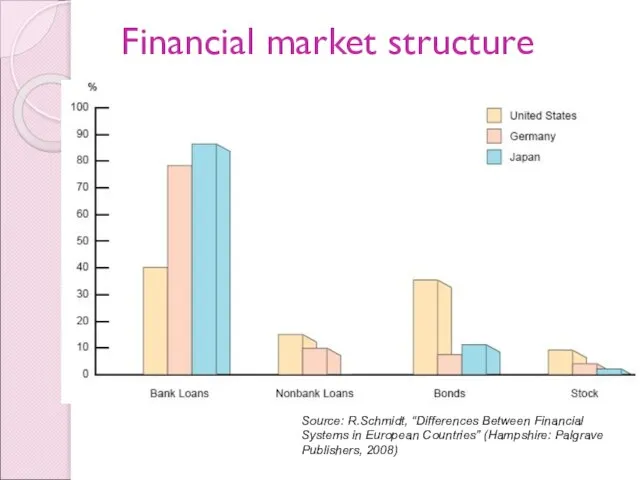

- 5. Financial market structure Source: R.Schmidt, “Differences Between Financial Systems in European Countries” (Hampshire: Palgrave Publishers, 2008)

- 6. Some puzzles of financial market structure Stocks are not the most important source of external financing

- 7. What is a financial service? Among the things money can buy, there is a distinction between

- 8. Types of financial services: Banking services Cash management services Card services Currency exchange Taking deposits Lending,

- 9. Key principles in financial services: Intermediation. It channels money from savers to borrowers, and it matches

- 10. The players Households Firms Financial intermediaries and Government all play a role in the financial system

- 11. Player-Households The opposite is true, unfortunately, for developing countries. According to the World Savings Banks Institute

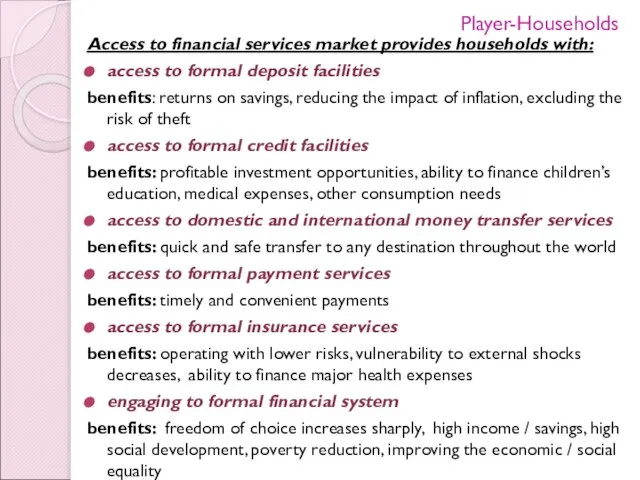

- 12. Access to financial services market provides households with: access to formal deposit facilities benefits: returns on

- 13. Firms can raise and invest capital using many sources with a variety of financial instruments. The

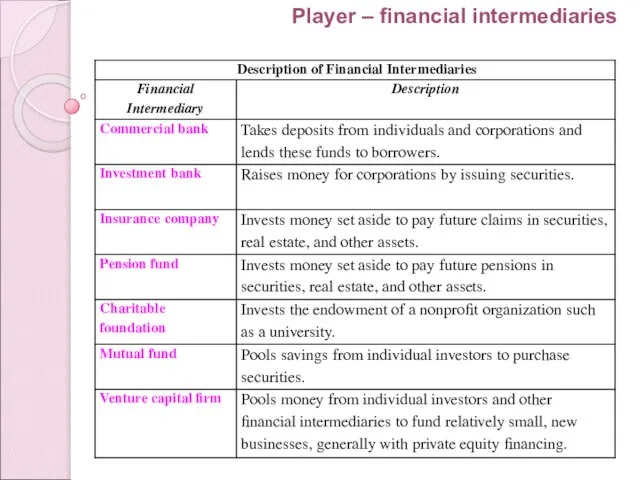

- 14. Financial intermediary - a financial institution that stands between counterparties in a transaction and connects surplus

- 15. Player – financial intermediaries

- 16. “Among the significant consequences of the latest crisis, one stands out in particular, - the belief

- 17. The government not only regulates financial markets and intermediaries, it is also an investor and borrower

- 18. Trends in financial services market Much of what we learn today - the sources of external

- 19. Globalization Financial markets are now global. Large multinational firms routinely issue debt and equity outside their

- 20. Trends Innovative Instruments Globalization has also spurred financial innovation. Firms have cleverly designed new instruments that

- 21. E-business and Universal Banking Business activity is being conducted through online banking and transactions. E-business capability

- 22. Negative trends Financial services institutions also face market change on next fronts: Tightening credit guidelines that

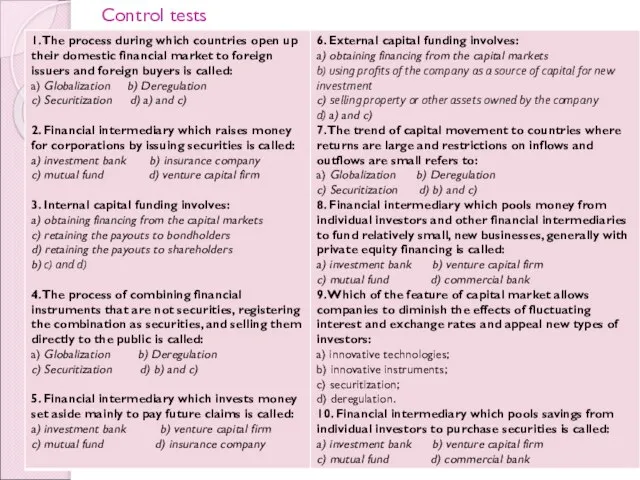

- 23. Control tests

- 25. Скачать презентацию

Слайд 3Financial market. Revision

Financial market is a mechanism that allows people to easily

Financial market. Revision

Financial market is a mechanism that allows people to easily

Слайд 4The financial markets can be divided into different subtypes:

1. Capital markets which

The financial markets can be divided into different subtypes:

1. Capital markets which

Слайд 5Financial market structure

Source: R.Schmidt, “Differences Between Financial Systems in European Countries” (Hampshire:

Financial market structure

Source: R.Schmidt, “Differences Between Financial Systems in European Countries” (Hampshire:

Слайд 6Some puzzles of financial market structure

Stocks are not the most important source

Some puzzles of financial market structure

Stocks are not the most important source

Слайд 7What is a financial service?

Among the things money can buy, there is

What is a financial service?

Among the things money can buy, there is

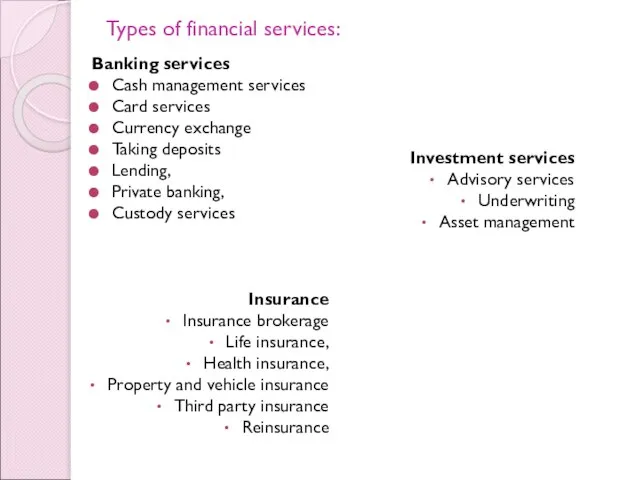

Слайд 8Types of financial services:

Banking services

Cash management services

Card services

Currency exchange

Taking deposits

Lending,

Private banking,

Custody services

Insurance

Types of financial services:

Banking services

Cash management services

Card services

Currency exchange

Taking deposits

Lending,

Private banking,

Custody services

Insurance

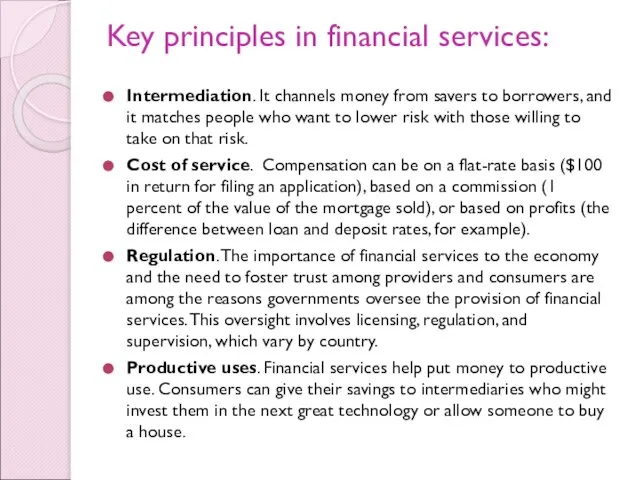

Слайд 9Key principles in financial services:

Intermediation. It channels money from savers to borrowers,

Key principles in financial services:

Intermediation. It channels money from savers to borrowers,

Слайд 10The players

Households

Firms

Financial intermediaries and

Government

all play a role in the financial

The players

Households

Firms

Financial intermediaries and

Government

all play a role in the financial

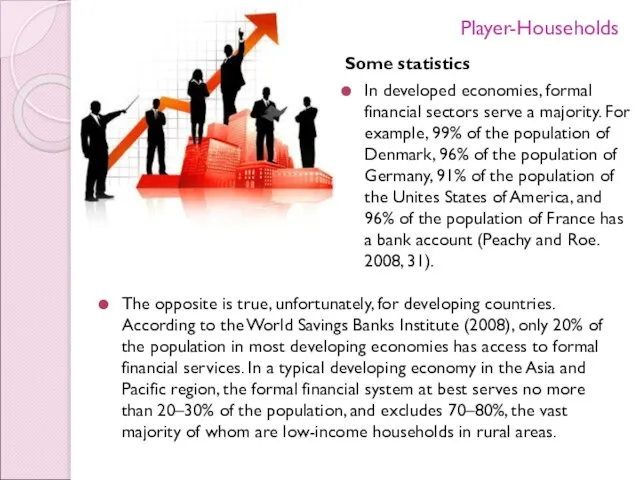

Слайд 11Player-Households

The opposite is true, unfortunately, for developing countries. According to the

Player-Households

The opposite is true, unfortunately, for developing countries. According to the

Слайд 12Access to financial services market provides households with:

access to formal deposit facilities

Access to financial services market provides households with:

access to formal deposit facilities

Слайд 13Firms can raise and invest capital using many sources with a variety

Firms can raise and invest capital using many sources with a variety

Слайд 14Financial intermediary - a financial institution that stands between counterparties in a

Financial intermediary - a financial institution that stands between counterparties in a

Слайд 15Player – financial intermediaries

Player – financial intermediaries

Слайд 16“Among the significant consequences of the latest crisis, one stands out in

“Among the significant consequences of the latest crisis, one stands out in

Слайд 17The government not only regulates financial markets and intermediaries, it is also

The government not only regulates financial markets and intermediaries, it is also

Слайд 18Trends in financial services market

Much of what we learn today - the

Trends in financial services market

Much of what we learn today - the

Слайд 19Globalization

Financial markets are now global. Large multinational firms routinely issue debt and

Globalization

Financial markets are now global. Large multinational firms routinely issue debt and

Слайд 20Trends

Innovative Instruments

Globalization has also spurred financial innovation. Firms have cleverly designed new

Trends

Innovative Instruments

Globalization has also spurred financial innovation. Firms have cleverly designed new

Слайд 21E-business and Universal Banking

Business activity is being conducted through online banking

E-business and Universal Banking

Business activity is being conducted through online banking

Слайд 22Negative trends

Financial services institutions also face market change on next fronts:

Tightening

Negative trends

Financial services institutions also face market change on next fronts:

Tightening

Слайд 23Control tests

Control tests

Теплые и холодные цвета. Цветной тон. Яркость и насыщенность. Способы увеличения и уменьшения рисунка. Изготовление образцов счетн

Теплые и холодные цвета. Цветной тон. Яркость и насыщенность. Способы увеличения и уменьшения рисунка. Изготовление образцов счетн Интересные факты об Австралии

Интересные факты об Австралии Система управления ресурсами Сервисного Центра IBA

Система управления ресурсами Сервисного Центра IBA Current Communicative Approaches

Current Communicative Approaches Презентация на тему Интерфейсы ПК

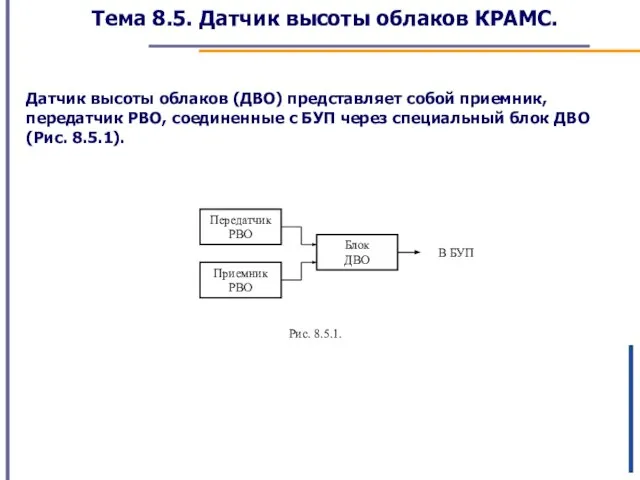

Презентация на тему Интерфейсы ПК Датчик высоты облаков КРАМС. Тема 8.5

Датчик высоты облаков КРАМС. Тема 8.5 «Технология хранения, поиска и сортировки информации в базах данных»

«Технология хранения, поиска и сортировки информации в базах данных» Рациональные способы вычислений

Рациональные способы вычислений HR-managers

HR-managers Еще три дня нашей смены...

Еще три дня нашей смены... Гастрономическое путешествие в Тверскую кулинарию

Гастрономическое путешествие в Тверскую кулинарию Роль политики в жизни общества

Роль политики в жизни общества PsychedelicWaves из моих OneNote Google. Документы

PsychedelicWaves из моих OneNote Google. Документы Дождик

Дождик Моя семья Майер

Моя семья Майер Педагогика

Педагогика Презентация на тему Боткин Сергей Петрович

Презентация на тему Боткин Сергей Петрович  Деятельность учителя начальных классов в рамках ФГОС

Деятельность учителя начальных классов в рамках ФГОС Презентация на тему:

Презентация на тему: И.Бунин Современная политическая ситуация в России: основные проблемы

И.Бунин Современная политическая ситуация в России: основные проблемы Алгоритмы

Алгоритмы КАЦАПИН РОБИНЗОН АЛЕКСЕЕВИЧ – командир, инженер - аналитик высокого класса, специалист связи широкого профиля, воин – интернаци

КАЦАПИН РОБИНЗОН АЛЕКСЕЕВИЧ – командир, инженер - аналитик высокого класса, специалист связи широкого профиля, воин – интернаци Национальный костюм в зеркале веков

Национальный костюм в зеркале веков ТК 122 «Стандарты финансовых операций»

ТК 122 «Стандарты финансовых операций» Модели и моделирование

Модели и моделирование Поощрительные программы

Поощрительные программы Место президента РФ в системе федеральных органов государственной власти

Место президента РФ в системе федеральных органов государственной власти Презентация на тему Гидросфера - водная оболочка Земли

Презентация на тему Гидросфера - водная оболочка Земли