- Probability Distributions

Содержание

- 2. Random Variable A random variable x takes on a defined set of values with different probabilities.

- 3. Random variables can be discrete or continuous Discrete random variables have a countable number of outcomes

- 4. Probability functions A probability function maps the possible values of x against their respective probabilities of

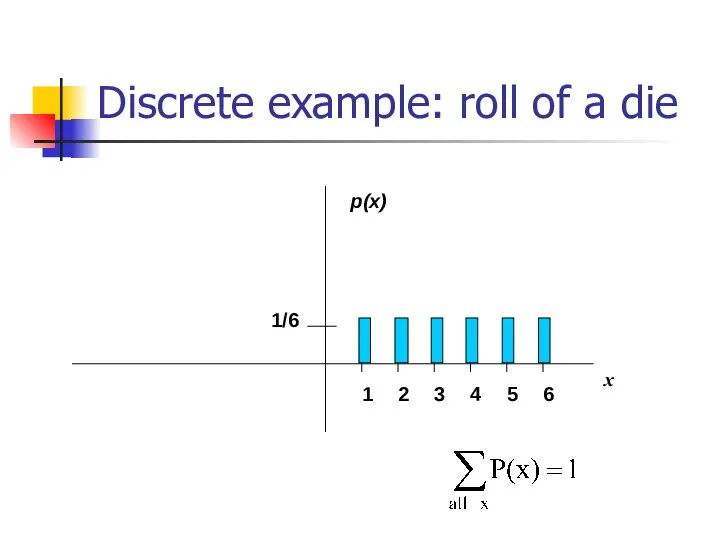

- 5. Discrete example: roll of a die

- 6. Probability mass function (pmf)

- 7. Cumulative distribution function (CDF)

- 8. Cumulative distribution function

- 9. Examples 1. What’s the probability that you roll a 3 or less? P(x≤3)=1/2 2. What’s the

- 10. Practice Problem Which of the following are probability functions? a. f(x)=.25 for x=9,10,11,12 b. f(x)= (3-x)/2

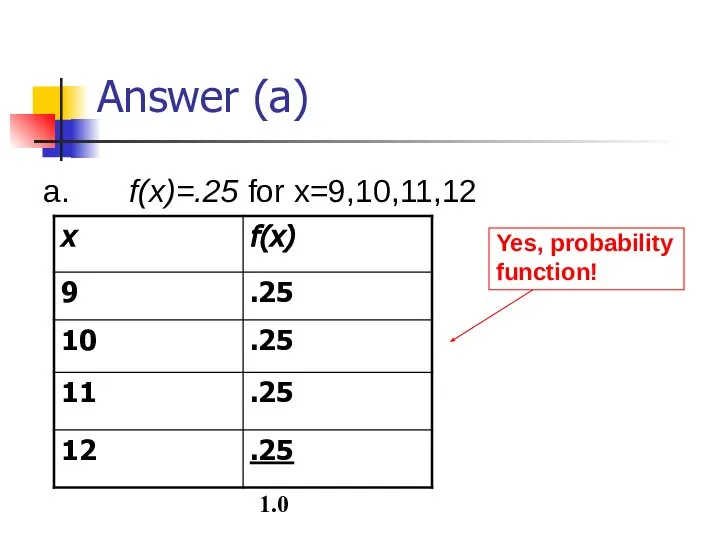

- 11. Answer (a) a. f(x)=.25 for x=9,10,11,12 1.0

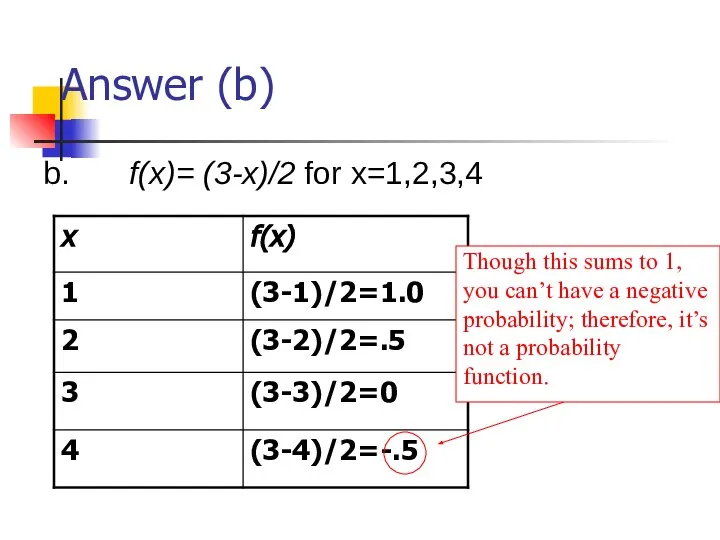

- 12. Answer (b) b. f(x)= (3-x)/2 for x=1,2,3,4

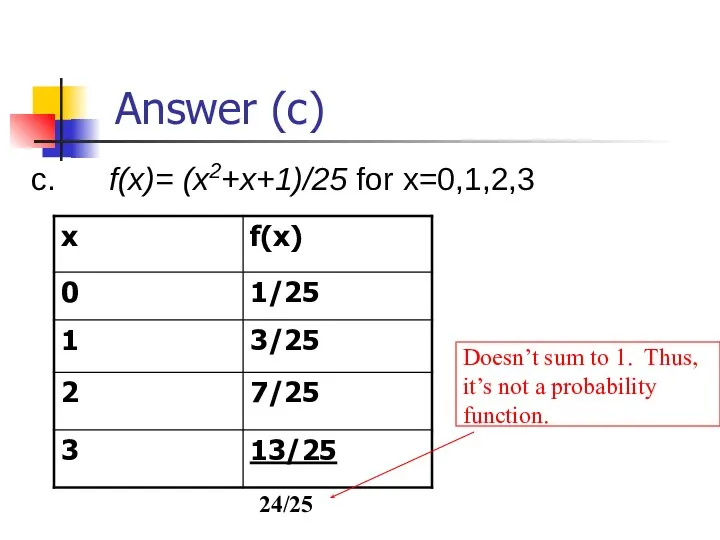

- 13. Answer (c) c. f(x)= (x2+x+1)/25 for x=0,1,2,3

- 14. Practice Problem: The number of ships to arrive at a harbor on any given day is

- 15. Practice Problem: You are lecturing to a group of 1000 students. You ask them to each

- 16. Important discrete distributions in epidemiology… Binomial Yes/no outcomes (dead/alive, treated/untreated, smoker/non-smoker, sick/well, etc.) Poisson Counts (e.g.,

- 17. Continuous case The probability function that accompanies a continuous random variable is a continuous mathematical function

- 18. Continuous case For example, recall the negative exponential function (in probability, this is called an “exponential

- 19. Continuous case: “probability density function” (pdf) The probability that x is any exact particular value (such

- 20. For example, the probability of x falling within 1 to 2:

- 21. Cumulative distribution function As in the discrete case, we can specify the “cumulative distribution function” (CDF):

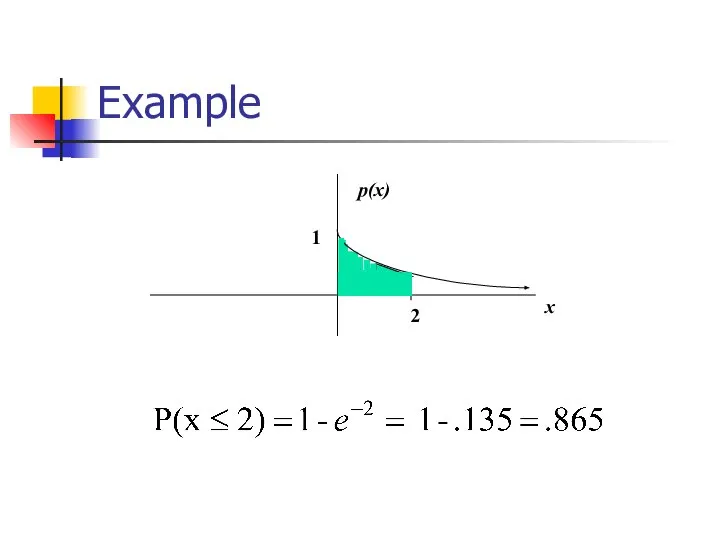

- 22. Example

- 23. Example 2: Uniform distribution The uniform distribution: all values are equally likely The uniform distribution: f(x)=

- 24. Example: Uniform distribution What’s the probability that x is between ¼ and ½? P(½ ≥x≥ ¼

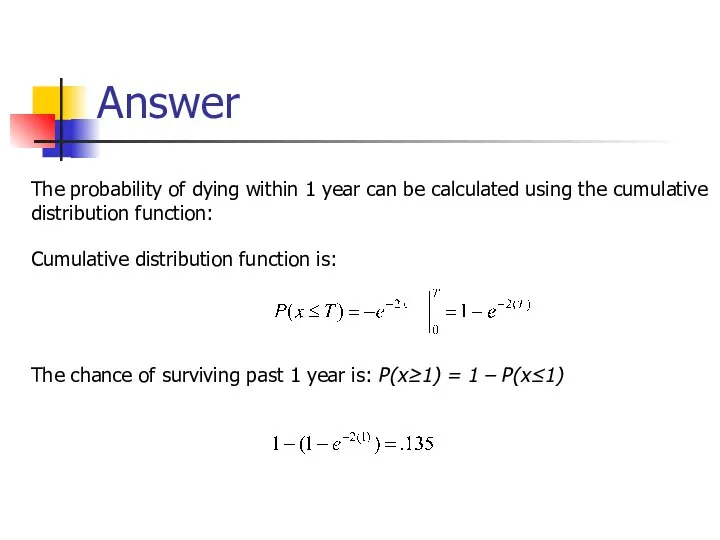

- 25. Practice Problem 4. Suppose that survival drops off rapidly in the year following diagnosis of a

- 26. Answer The probability of dying within 1 year can be calculated using the cumulative distribution function:

- 27. Expected Value and Variance All probability distributions are characterized by an expected value and a variance

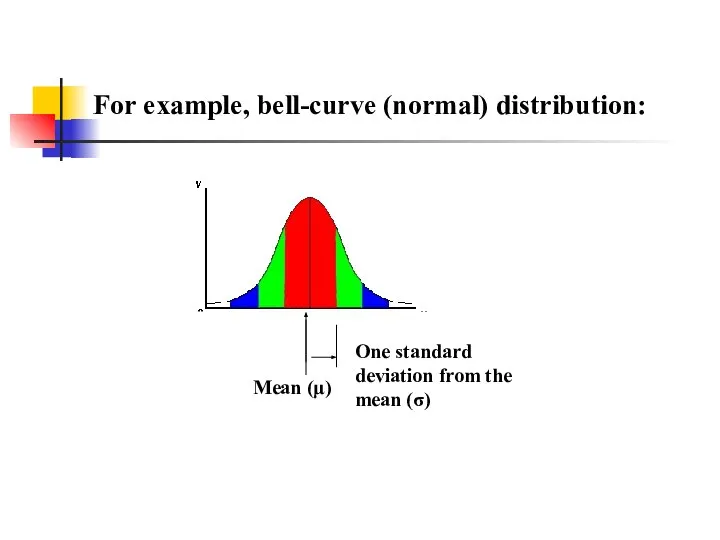

- 28. For example, bell-curve (normal) distribution:

- 29. Expected value, or mean If we understand the underlying probability function of a certain phenomenon, then

- 30. Example: expected value Recall the following probability distribution of ship arrivals:

- 31. Expected value, formally Discrete case: Continuous case:

- 32. Empirical Mean is a special case of Expected Value… Sample mean, for a sample of n

- 33. Expected value, formally Discrete case: Continuous case:

- 34. Extension to continuous case: uniform distribution x p(x) 1 1

- 35. Symbol Interlude E(X) = µ these symbols are used interchangeably

- 36. Expected Value Expected value is an extremely useful concept for good decision-making!

- 37. Example: the lottery The Lottery (also known as a tax on people who are bad at

- 38. Lottery Calculate the probability of winning in 1 try: The probability function (note, sums to 1.0):

- 39. Expected Value The probability function Expected Value E(X) = P(win)*$2,000,000 + P(lose)*-$1.00 = 2.0 x 106

- 40. Expected Value If you play the lottery every week for 10 years, what are your expected

- 41. Gambling (or how casinos can afford to give so many free drinks…) A roulette wheel has

- 42. **A few notes about Expected Value as a mathematical operator: If c= a constant number (i.e.,

- 43. E(c) = c E(c) = c Example: If you cash in soda cans in CA, you

- 44. E(cX)=cE(X) E(cX)=cE(X) Example: If the casino charges $10 per game instead of $1, then the casino

- 45. E(c + X)=c + E(X) E(c + X)=c + E(X) Example, if the casino throws in

- 46. E(X+Y)= E(X) + E(Y) E(X+Y)= E(X) + E(Y) Example: If you play the lottery twice, you

- 47. Practice Problem If a disease is fairly rare and the antibody test is fairly expensive, in

- 48. Answer (a) a. Suppose a particular disease has a prevalence of 10% in a third-world population

- 49. Answer (b) b. What if you pool only 10 samples at a time? E(X) = (.90)10

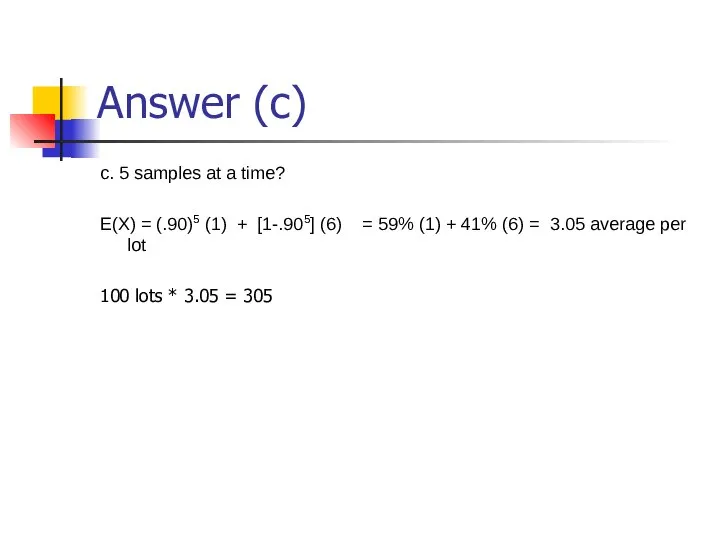

- 50. Answer (c) c. 5 samples at a time? E(X) = (.90)5 (1) + [1-.905] (6) =

- 51. Practice Problem If X is a random integer between 1 and 10, what’s the expected value

- 52. Answer If X is a random integer between 1 and 10, what’s the expected value of

- 53. Expected value isn’t everything though… Take the show “Deal or No Deal” Everyone know the rules?

- 54. Deal or No Deal… This could really be represented as a probability distribution and a non-random

- 55. Expected value doesn’t help…

- 56. How to decide? Variance! If you take the deal, the variance/standard deviation is 0. If you

- 57. Variance/standard deviation “The average (expected) squared distance (or deviation) from the mean” **We square because squaring

- 58. Variance, formally Discrete case: Continuous case:

- 59. Similarity to empirical variance The variance of a sample: s2 =

- 60. Symbol Interlude Var(X) = σ2 these symbols are used interchangeably

- 61. Variance: Deal or No Deal Now you examine your personal risk tolerance…

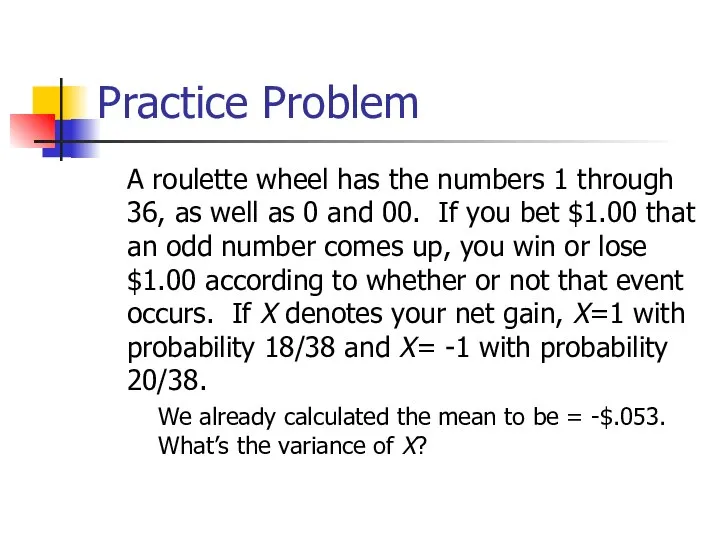

- 62. Practice Problem A roulette wheel has the numbers 1 through 36, as well as 0 and

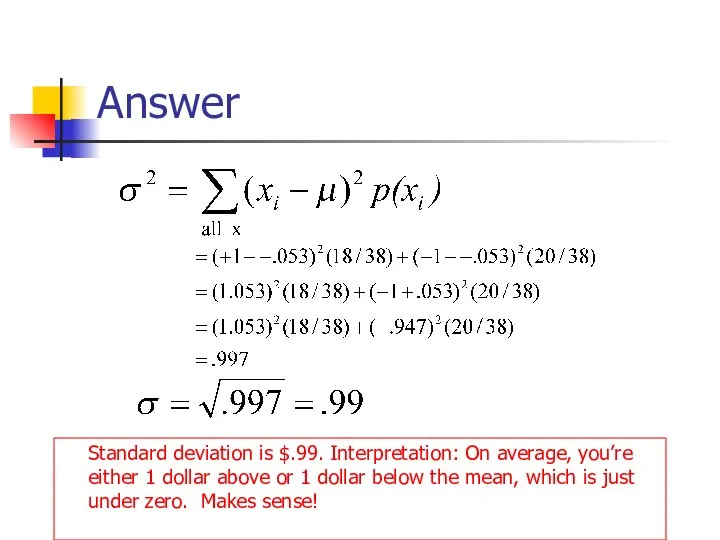

- 63. Answer Standard deviation is $.99. Interpretation: On average, you’re either 1 dollar above or 1 dollar

- 64. Handy calculation formula! Handy calculation formula (if you ever need to calculate by hand!):

- 65. Var(x) = E(x-μ)2 = E(x2) – [E(x)]2 (your calculation formula!) Proofs (optional!): E(x-μ)2 = E(x2–2μx +

- 66. For example, what’s the variance and standard deviation of the roll of a die?

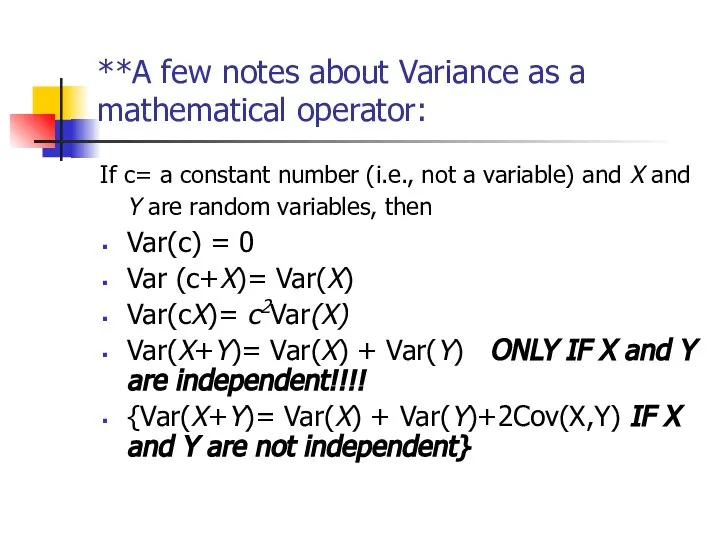

- 67. **A few notes about Variance as a mathematical operator: If c= a constant number (i.e., not

- 68. Var(c) = 0 Var(c) = 0 Constants don’t vary!

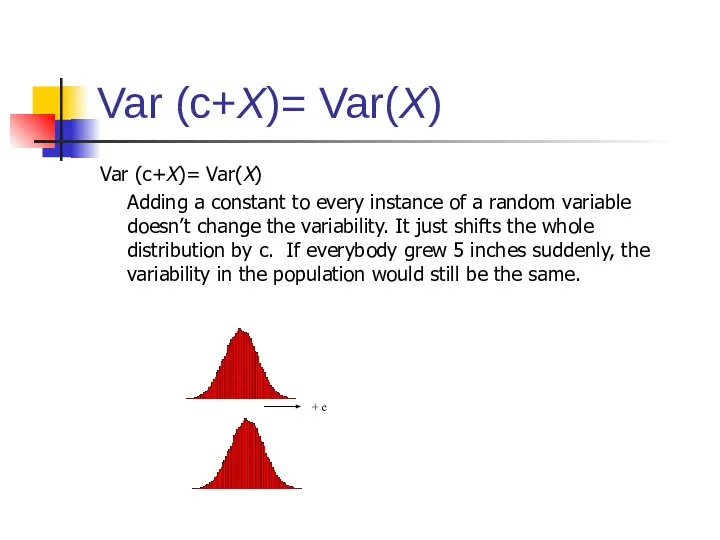

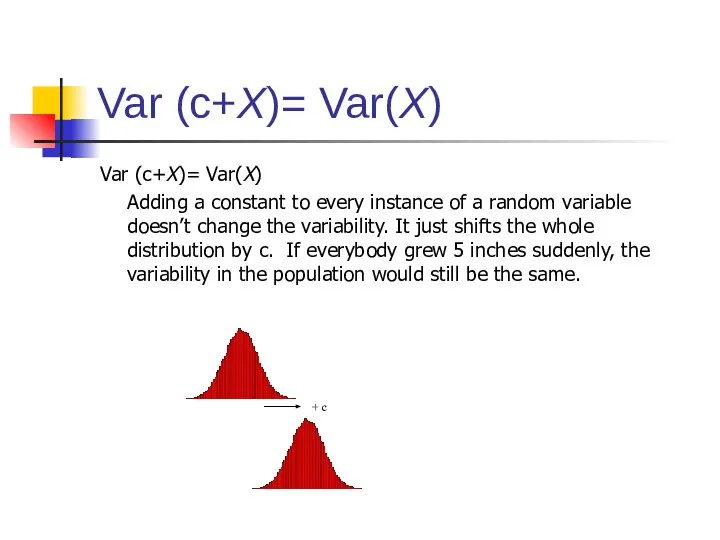

- 69. Var (c+X)= Var(X) Var (c+X)= Var(X) Adding a constant to every instance of a random variable

- 70. Var (c+X)= Var(X) Var (c+X)= Var(X) Adding a constant to every instance of a random variable

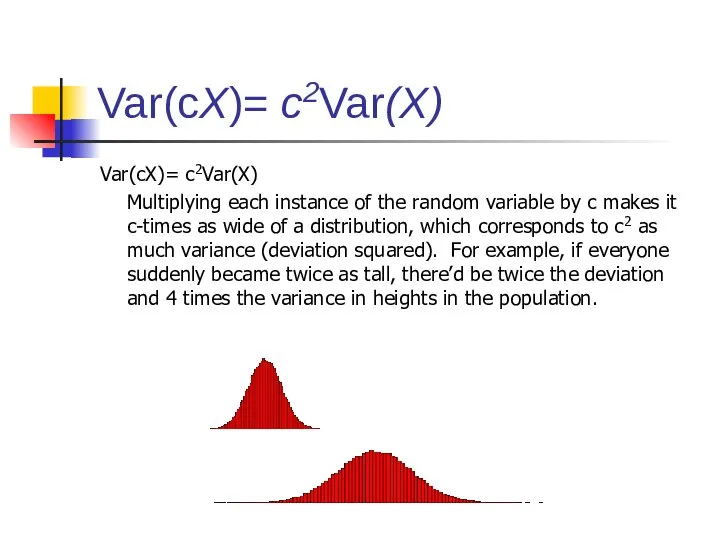

- 71. Var(cX)= c2Var(X) Var(cX)= c2Var(X) Multiplying each instance of the random variable by c makes it c-times

- 72. Var(X+Y)= Var(X) + Var(Y) Var(X+Y)= Var(X) + Var(Y) ONLY IF X and Y are independent!!!!!!!! With

- 73. Example of Var(X+Y)= Var(X) + Var(Y): TPMT TPMT metabolizes the drugs 6- mercaptopurine, azathioprine, and 6-thioguanine

- 74. TPMT activity by genotype Weinshilboum R. Drug Metab Dispos. 2001 Apr;29(4 Pt 2):601-5

- 75. TPMT activity by genotype Weinshilboum R. Drug Metab Dispos. 2001 Apr;29(4 Pt 2):601-5 The variability in

- 76. TPMT activity by genotype Weinshilboum R. Drug Metab Dispos. 2001 Apr;29(4 Pt 2):601-5 There is variability

- 77. Practice Problem Find the variance and standard deviation for the number of ships to arrive at

- 78. Answer: variance and std dev Interpretation: On an average day, we expect 11.3 ships to arrive

- 79. Practice Problem You toss a coin 100 times. What’s the expected number of heads? What’s the

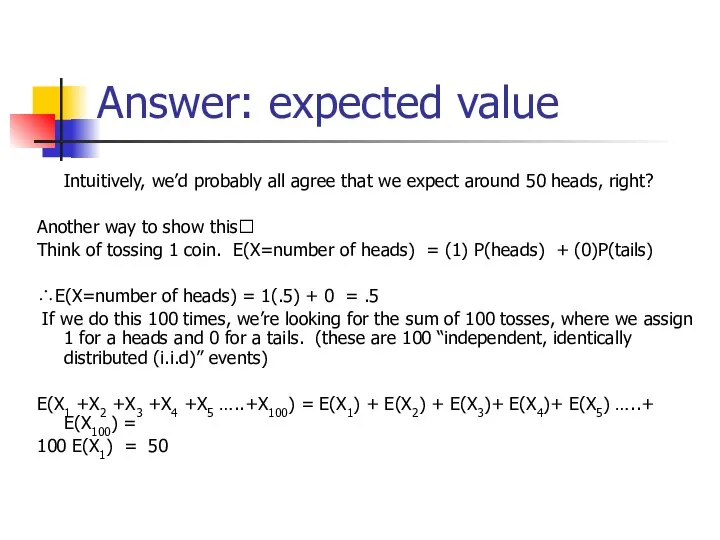

- 80. Answer: expected value Intuitively, we’d probably all agree that we expect around 50 heads, right? Another

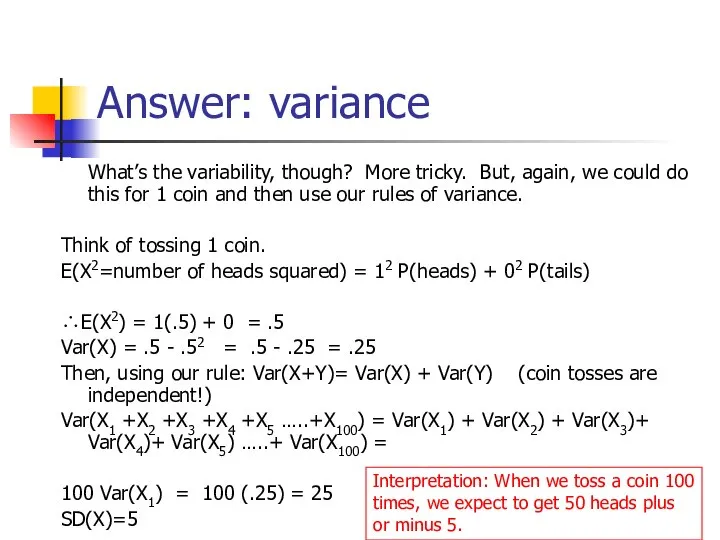

- 81. Answer: variance What’s the variability, though? More tricky. But, again, we could do this for 1

- 82. Or use computer simulation… Flip coins virtually! Flip a virtual coin 100 times; count the number

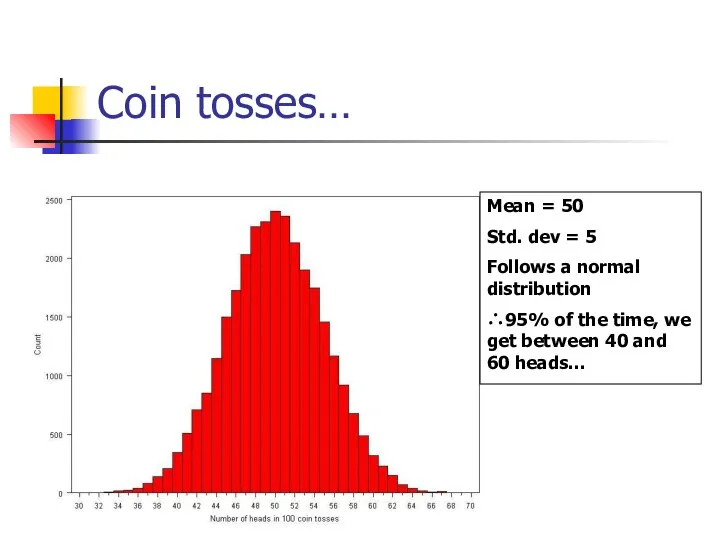

- 83. Coin tosses… Mean = 50 Std. dev = 5 Follows a normal distribution ∴95% of the

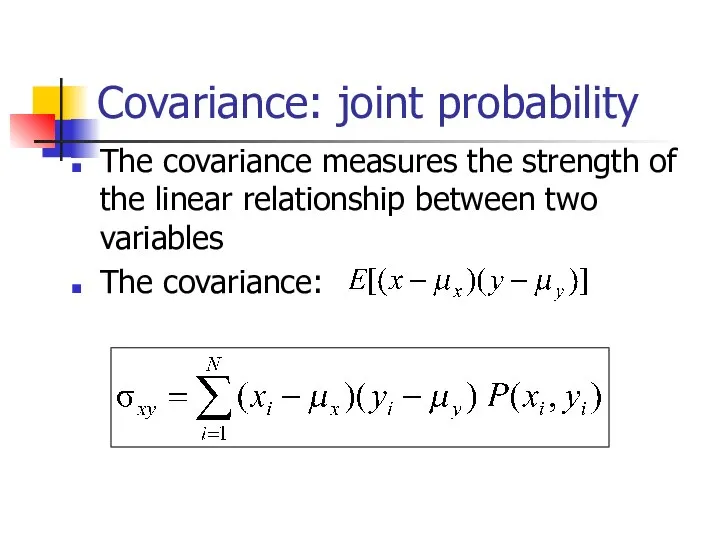

- 84. Covariance: joint probability The covariance measures the strength of the linear relationship between two variables The

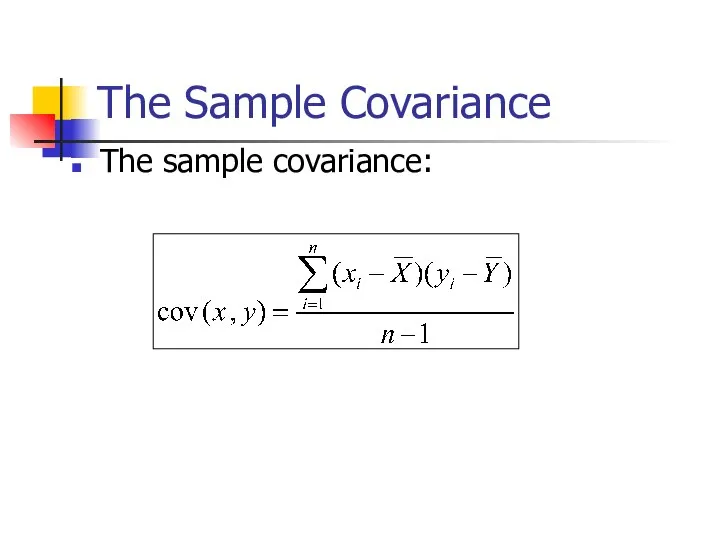

- 85. The Sample Covariance The sample covariance:

- 87. Скачать презентацию

Слайд 3Random variables can be discrete or continuous

Discrete random variables have a countable

Random variables can be discrete or continuous

Discrete random variables have a countable

Слайд 4Probability functions

A probability function maps the possible values of x against their

Probability functions

A probability function maps the possible values of x against their

Слайд 5

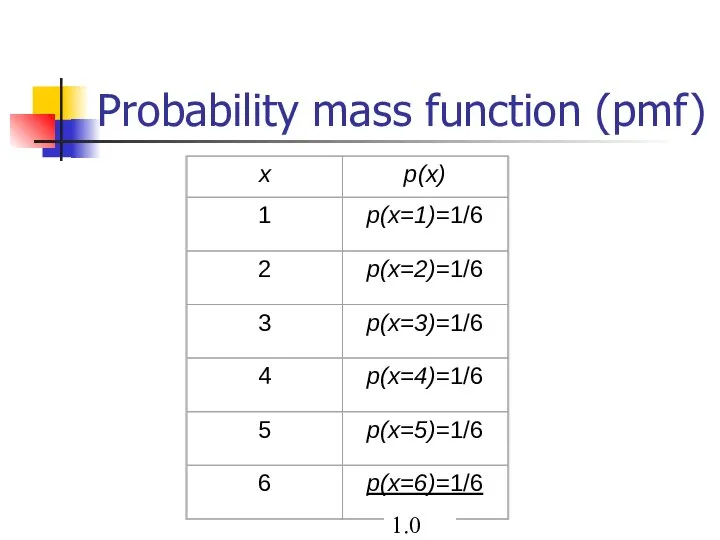

Discrete example: roll of a die

Discrete example: roll of a die

Слайд 6Probability mass function (pmf)

Probability mass function (pmf)

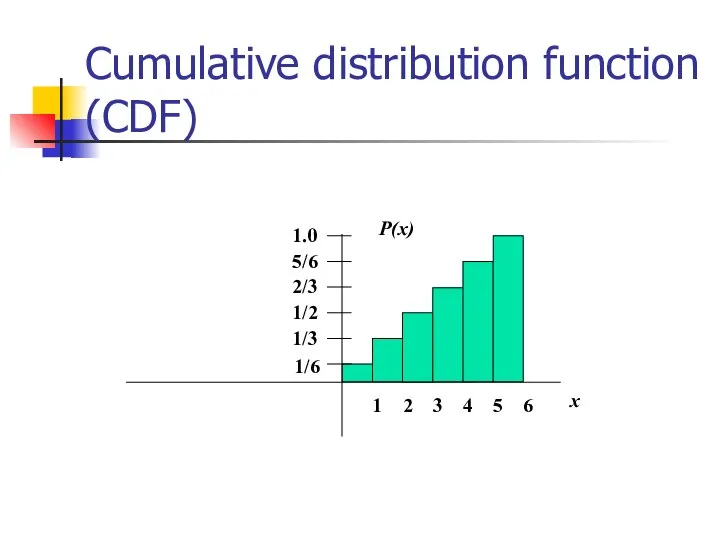

Слайд 7Cumulative distribution function (CDF)

Cumulative distribution function (CDF)

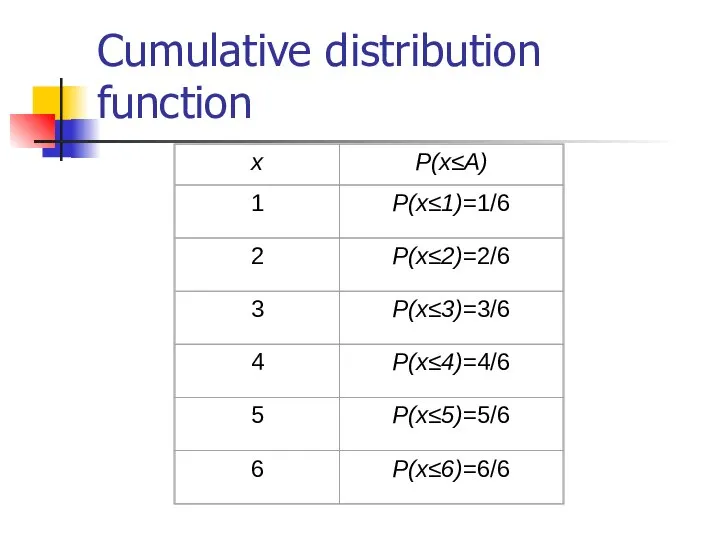

Слайд 8Cumulative distribution function

Cumulative distribution function

Слайд 9Examples

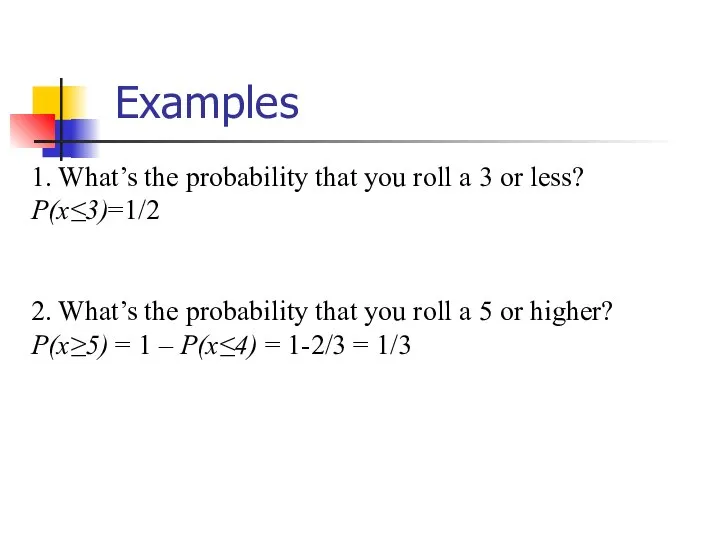

1. What’s the probability that you roll a 3 or less?

P(x≤3)=1/2

2.

Examples

1. What’s the probability that you roll a 3 or less?

P(x≤3)=1/2

2.

Слайд 10Practice Problem

Which of the following are probability functions?

a. f(x)=.25 for x=9,10,11,12

b. f(x)=

Practice Problem

Which of the following are probability functions?

a. f(x)=.25 for x=9,10,11,12

b. f(x)=

Слайд 11Answer (a)

a. f(x)=.25 for x=9,10,11,12

1.0

Answer (a)

a. f(x)=.25 for x=9,10,11,12

1.0

Слайд 12Answer (b)

b. f(x)= (3-x)/2 for x=1,2,3,4

Answer (b)

b. f(x)= (3-x)/2 for x=1,2,3,4

Слайд 13Answer (c)

c. f(x)= (x2+x+1)/25 for x=0,1,2,3

Answer (c)

c. f(x)= (x2+x+1)/25 for x=0,1,2,3

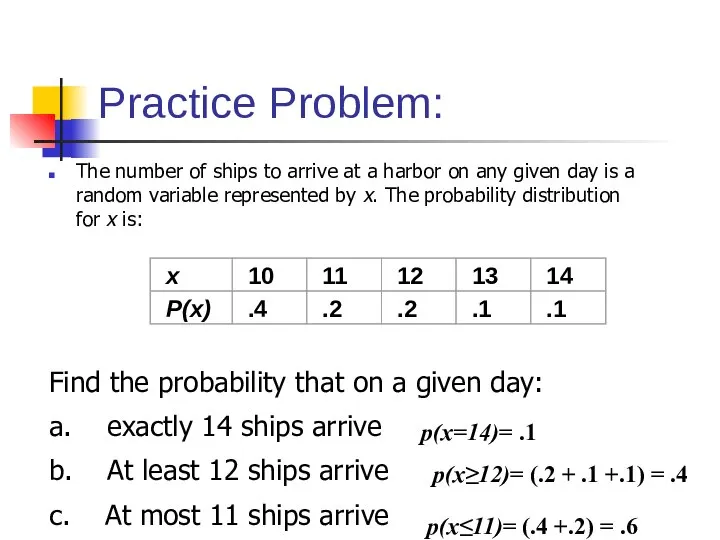

Слайд 14Practice Problem:

The number of ships to arrive at a harbor on any

Practice Problem:

The number of ships to arrive at a harbor on any

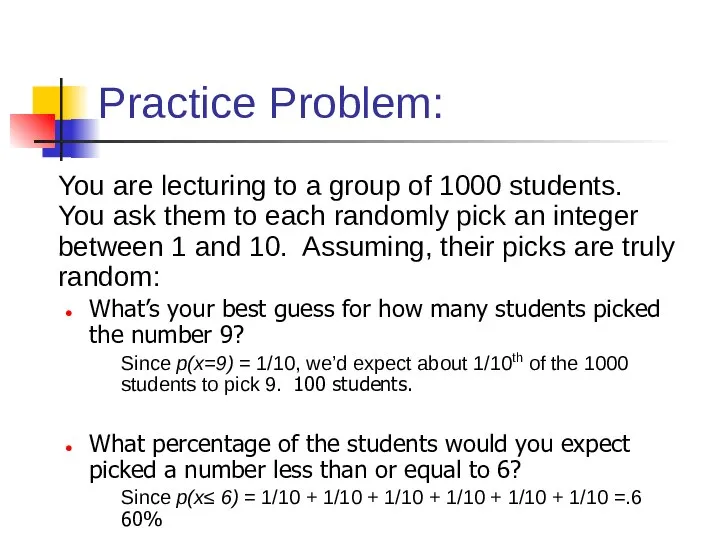

Слайд 15Practice Problem:

You are lecturing to a group of 1000 students. You ask

Practice Problem:

You are lecturing to a group of 1000 students. You ask

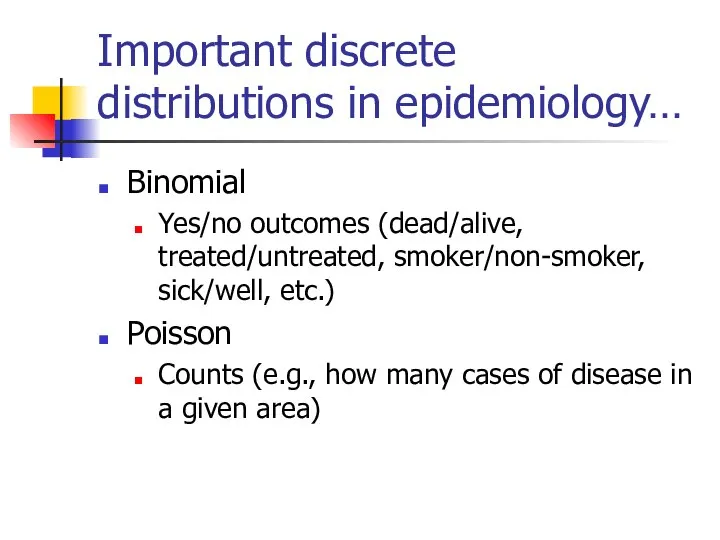

Слайд 16Important discrete distributions in epidemiology…

Binomial

Yes/no outcomes (dead/alive, treated/untreated, smoker/non-smoker, sick/well, etc.)

Poisson

Counts (e.g.,

Important discrete distributions in epidemiology…

Binomial

Yes/no outcomes (dead/alive, treated/untreated, smoker/non-smoker, sick/well, etc.)

Poisson

Counts (e.g.,

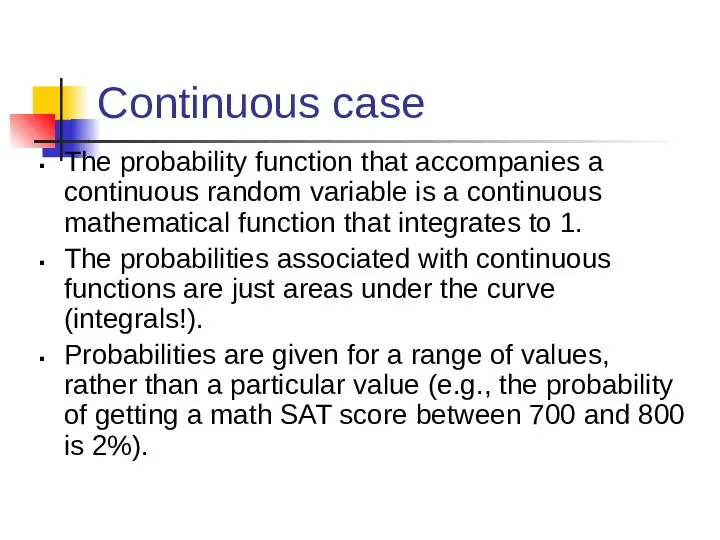

Слайд 17Continuous case

The probability function that accompanies a continuous random variable is a

Continuous case

The probability function that accompanies a continuous random variable is a

Слайд 18Continuous case

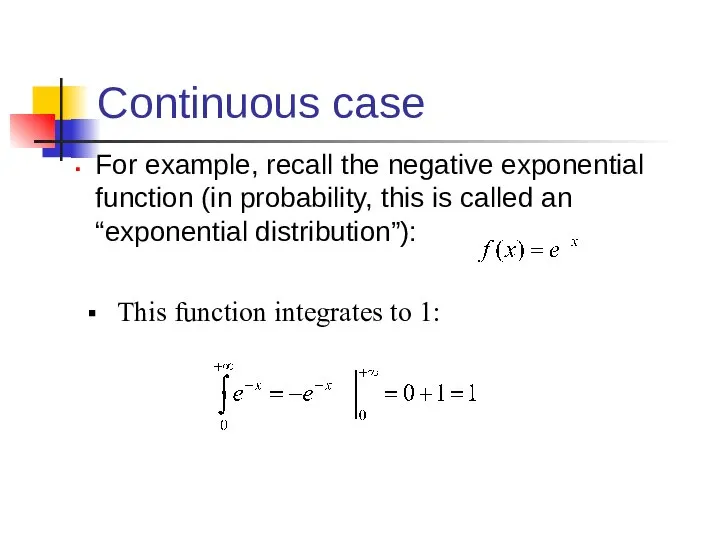

For example, recall the negative exponential function (in probability, this is

Continuous case

For example, recall the negative exponential function (in probability, this is

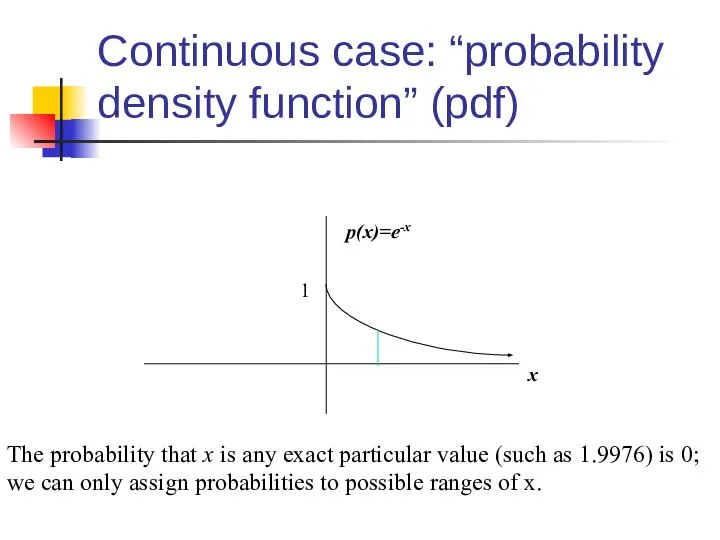

Слайд 19Continuous case: “probability density function” (pdf)

The probability that x is any exact

Continuous case: “probability density function” (pdf)

The probability that x is any exact

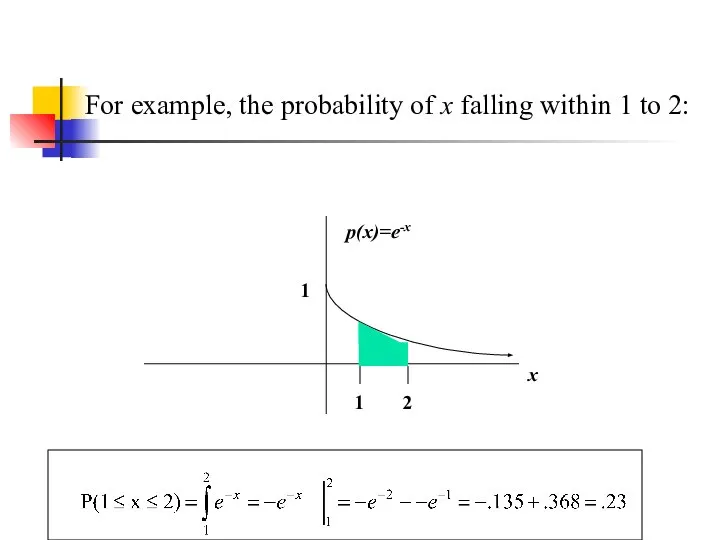

Слайд 20For example, the probability of x falling within 1 to 2:

For example, the probability of x falling within 1 to 2:

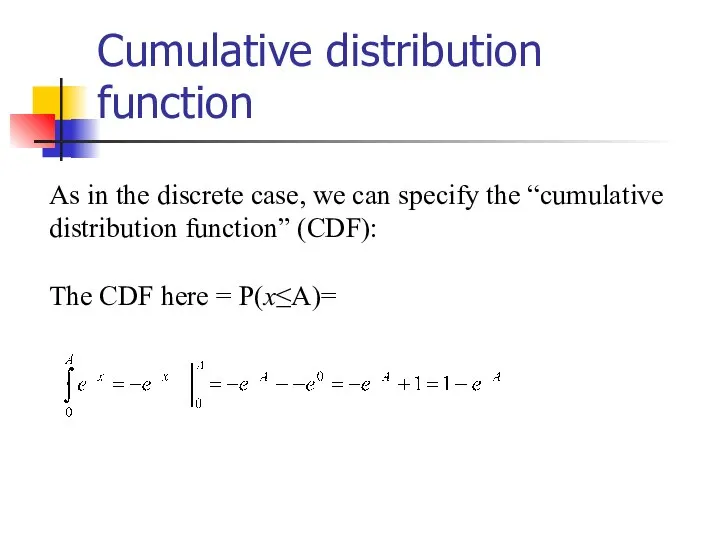

Слайд 21Cumulative distribution function

As in the discrete case, we can specify the “cumulative

Cumulative distribution function

As in the discrete case, we can specify the “cumulative

Слайд 22Example

Example

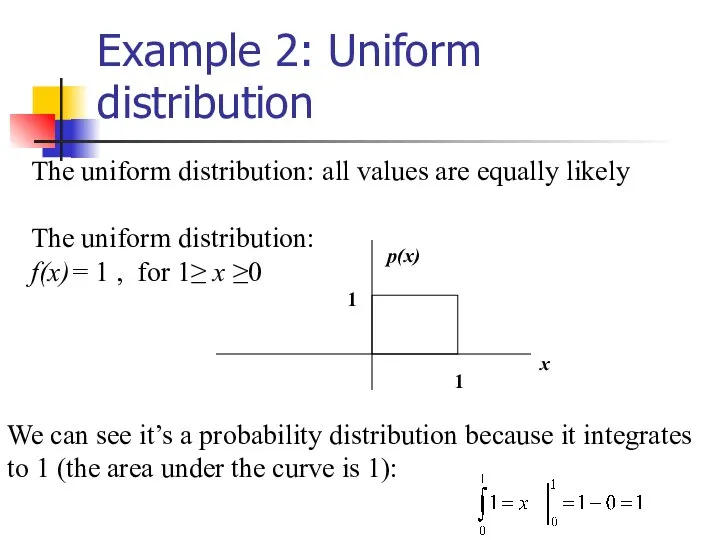

Слайд 23Example 2: Uniform distribution

The uniform distribution: all values are equally likely

The uniform

Example 2: Uniform distribution

The uniform distribution: all values are equally likely

The uniform

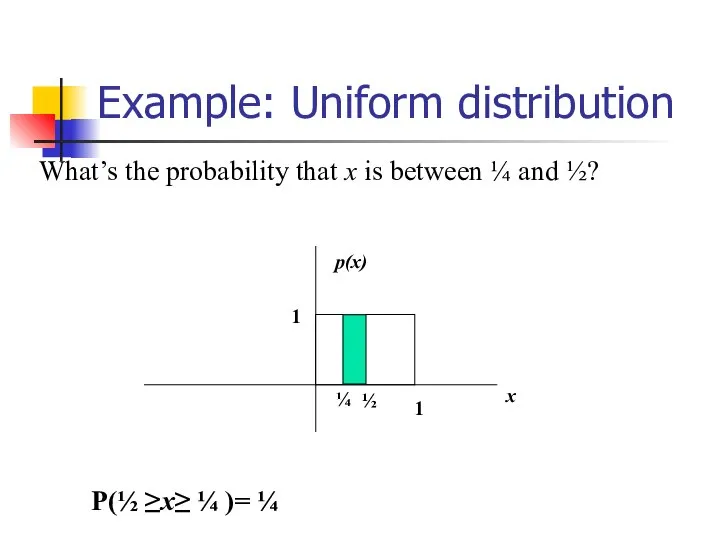

Слайд 24Example: Uniform distribution

What’s the probability that x is between ¼ and ½?

Example: Uniform distribution

What’s the probability that x is between ¼ and ½?

Слайд 25Practice Problem

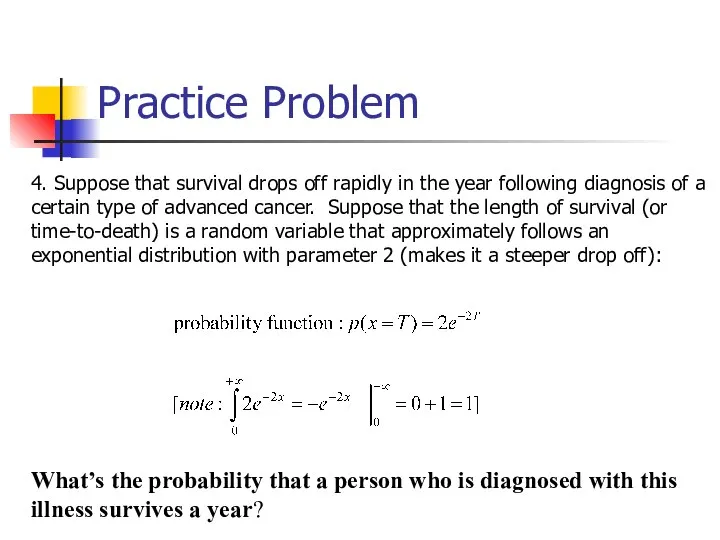

4. Suppose that survival drops off rapidly in the year

Practice Problem

4. Suppose that survival drops off rapidly in the year

Слайд 26Answer

The probability of dying within 1 year can be calculated using

Answer

The probability of dying within 1 year can be calculated using

Слайд 27Expected Value and Variance

All probability distributions are characterized by an expected value

Expected Value and Variance

All probability distributions are characterized by an expected value

Слайд 28For example, bell-curve (normal) distribution:

For example, bell-curve (normal) distribution:

Слайд 29Expected value, or mean

If we understand the underlying probability function of a

Expected value, or mean

If we understand the underlying probability function of a

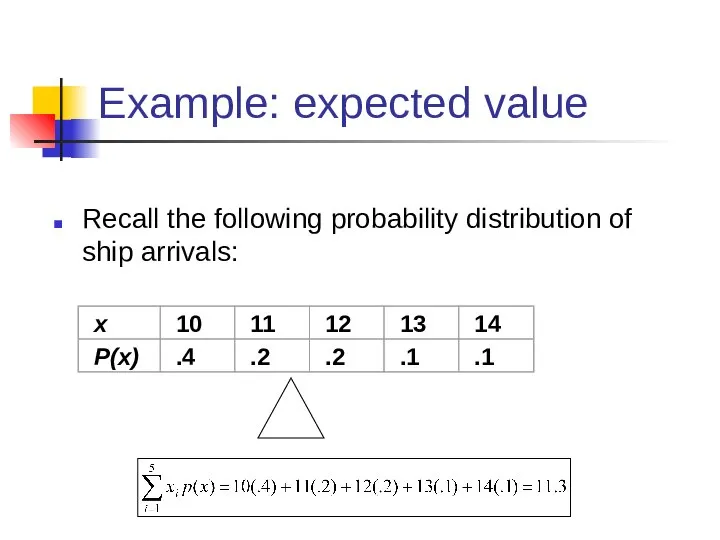

Слайд 30Example: expected value

Recall the following probability distribution of ship arrivals:

Example: expected value

Recall the following probability distribution of ship arrivals:

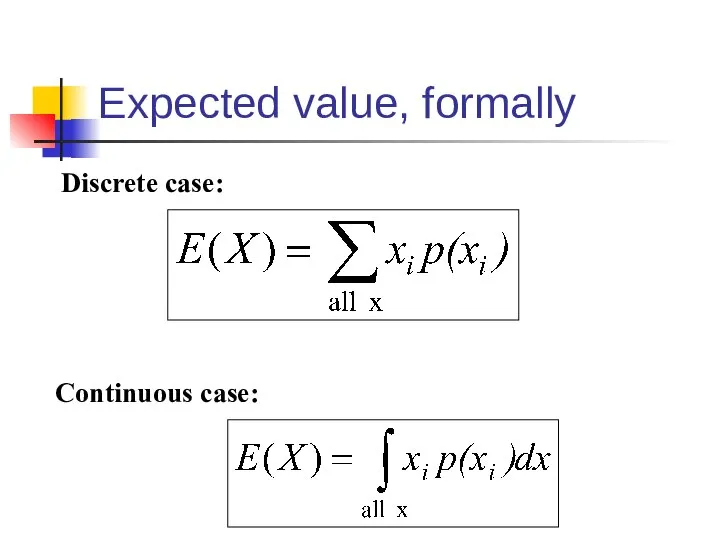

Слайд 31Expected value, formally

Discrete case:

Continuous case:

Expected value, formally

Discrete case:

Continuous case:

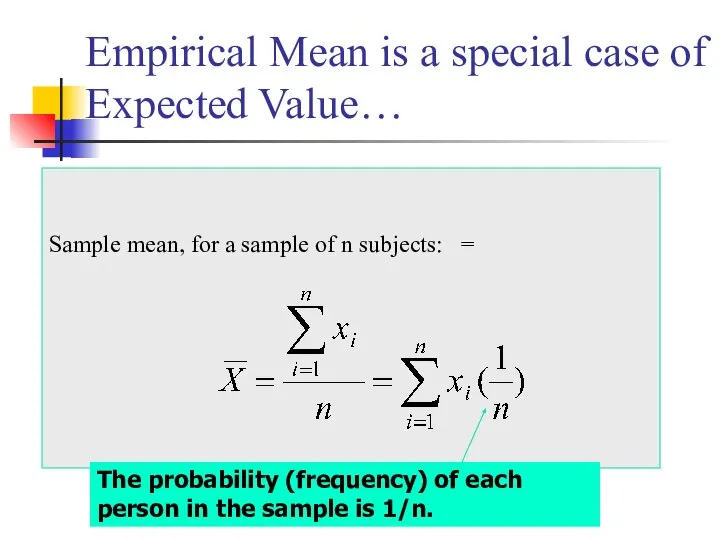

Слайд 32Empirical Mean is a special case of Expected Value…

Sample mean, for a

Empirical Mean is a special case of Expected Value…

Sample mean, for a

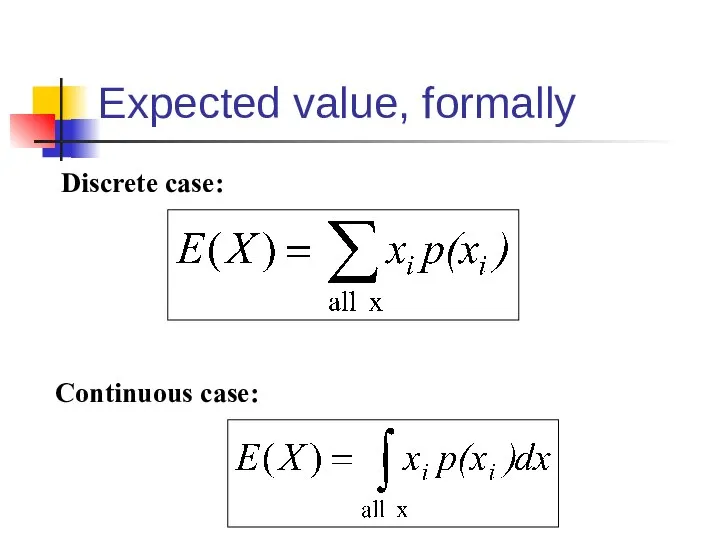

Слайд 33Expected value, formally

Discrete case:

Continuous case:

Expected value, formally

Discrete case:

Continuous case:

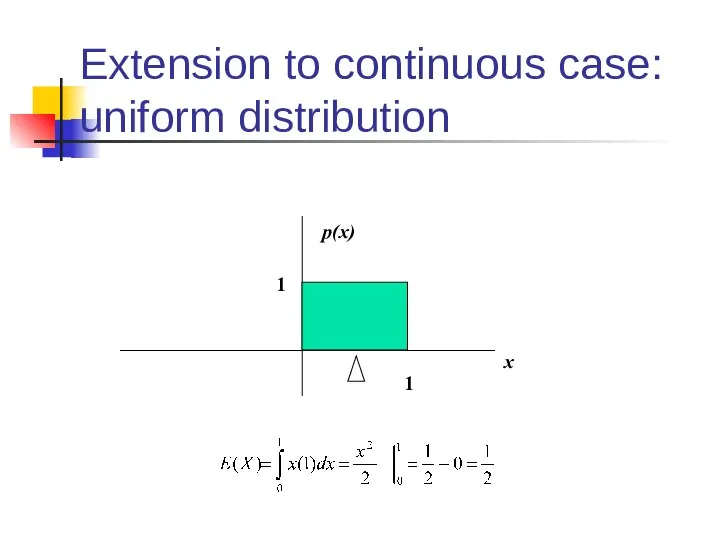

Слайд 34Extension to continuous case:

uniform distribution

x

p(x)

1

1

Extension to continuous case:

uniform distribution

x

p(x)

1

1

Слайд 35Symbol Interlude

E(X) = µ

these symbols are used interchangeably

Symbol Interlude

E(X) = µ

these symbols are used interchangeably

Слайд 36Expected Value

Expected value is an extremely useful concept for good decision-making!

Expected Value

Expected value is an extremely useful concept for good decision-making!

Слайд 37Example: the lottery

The Lottery (also known as a tax on people who

Example: the lottery

The Lottery (also known as a tax on people who

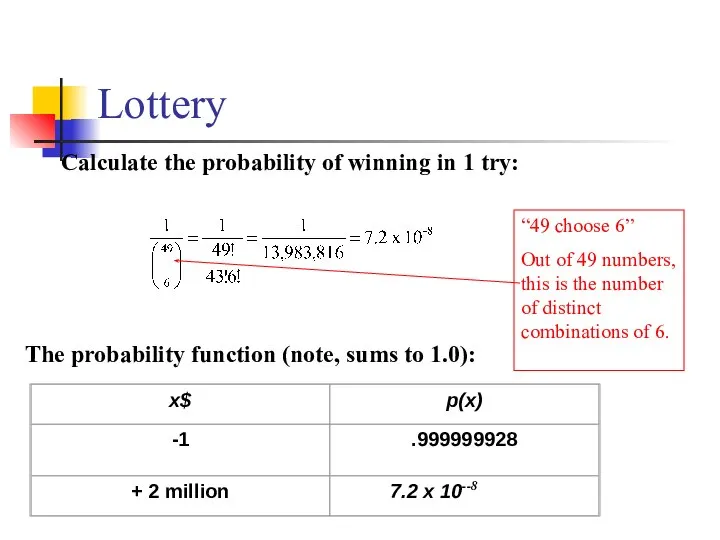

Слайд 38Lottery

Calculate the probability of winning in 1 try:

The probability function (note, sums

Lottery

Calculate the probability of winning in 1 try:

The probability function (note, sums

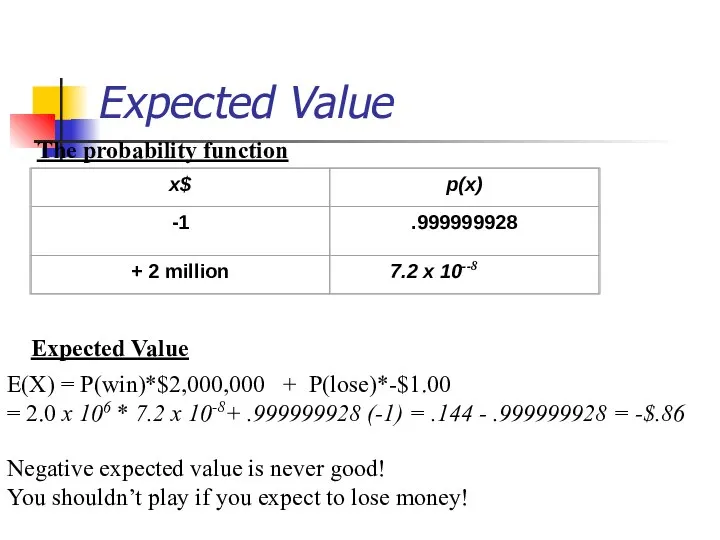

Слайд 39Expected Value

The probability function

Expected Value

E(X) = P(win)*$2,000,000 + P(lose)*-$1.00

= 2.0 x

Expected Value

The probability function

Expected Value

E(X) = P(win)*$2,000,000 + P(lose)*-$1.00

= 2.0 x

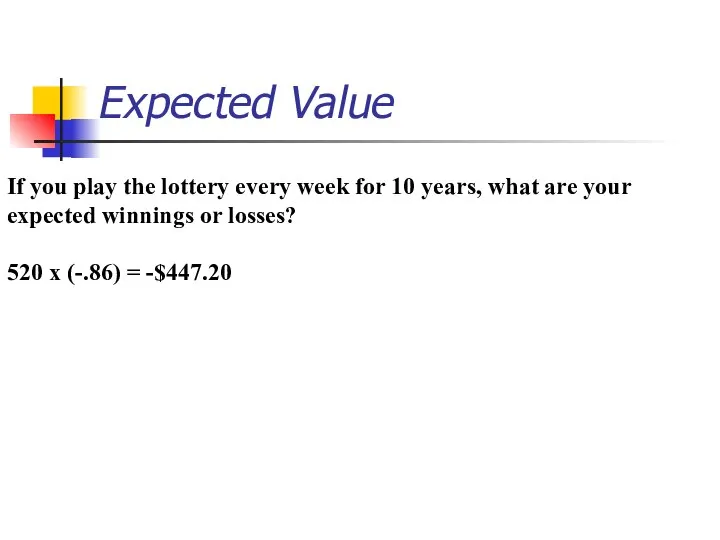

Слайд 40Expected Value

If you play the lottery every week for 10 years, what

Expected Value

If you play the lottery every week for 10 years, what

Слайд 41

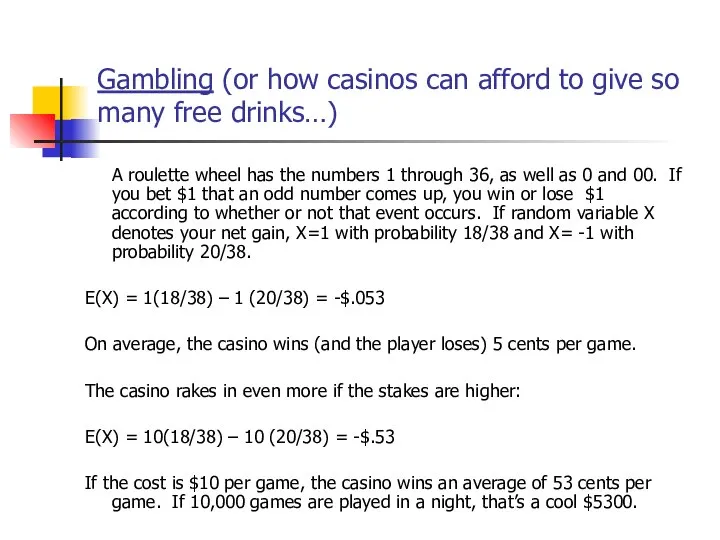

Gambling (or how casinos can afford to give so many free drinks…)

A

Gambling (or how casinos can afford to give so many free drinks…)

A

Слайд 42**A few notes about Expected Value as a mathematical operator:

If c= a

**A few notes about Expected Value as a mathematical operator:

If c= a

Слайд 43

E(c) = c

E(c) = c

Example: If you cash in soda

E(c) = c

E(c) = c

Example: If you cash in soda

Слайд 44E(cX)=cE(X)

E(cX)=cE(X)

Example: If the casino charges $10 per game instead of $1, then

E(cX)=cE(X)

E(cX)=cE(X)

Example: If the casino charges $10 per game instead of $1, then

Слайд 45E(c + X)=c + E(X)

E(c + X)=c + E(X)

Example, if the casino

E(c + X)=c + E(X)

E(c + X)=c + E(X)

Example, if the casino

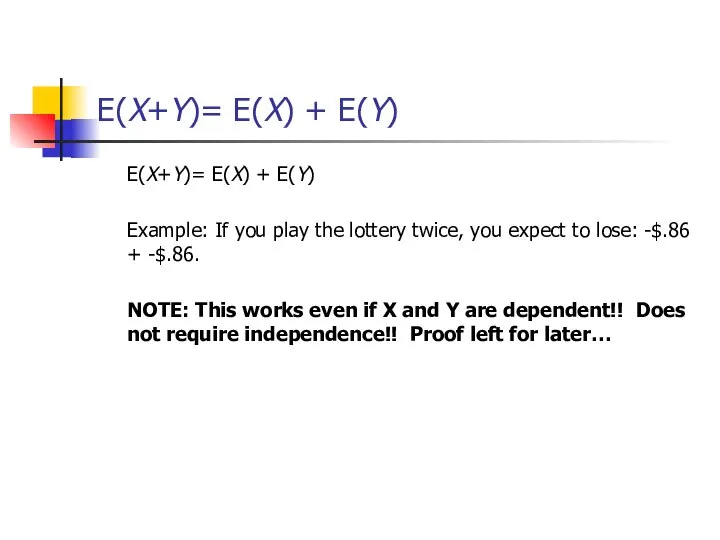

Слайд 46E(X+Y)= E(X) + E(Y)

E(X+Y)= E(X) + E(Y)

Example: If you play

E(X+Y)= E(X) + E(Y)

E(X+Y)= E(X) + E(Y)

Example: If you play

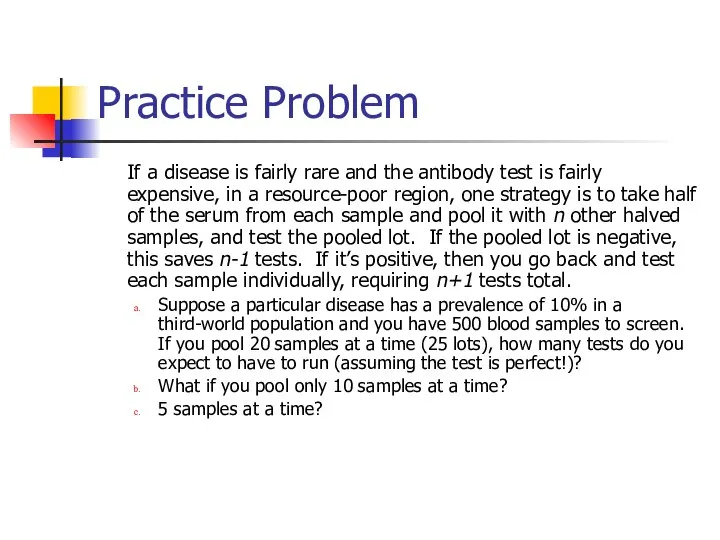

Слайд 47Practice Problem

If a disease is fairly rare and the antibody test is

Practice Problem

If a disease is fairly rare and the antibody test is

Слайд 48Answer (a)

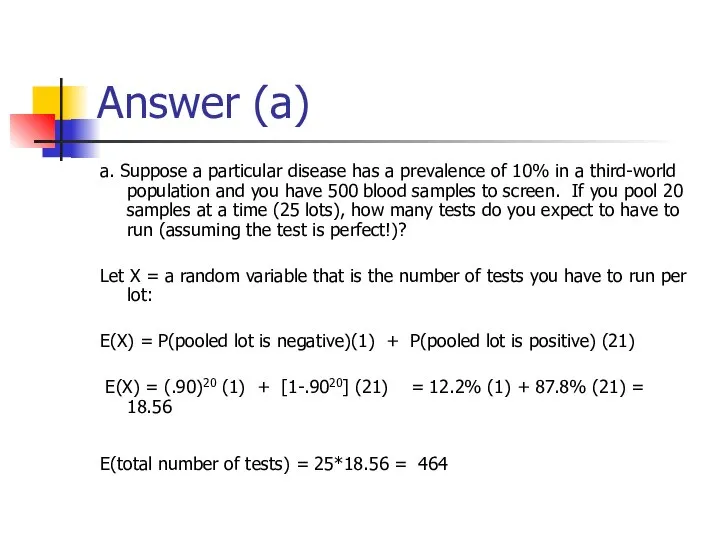

a. Suppose a particular disease has a prevalence of 10% in

Answer (a)

a. Suppose a particular disease has a prevalence of 10% in

Слайд 49Answer (b)

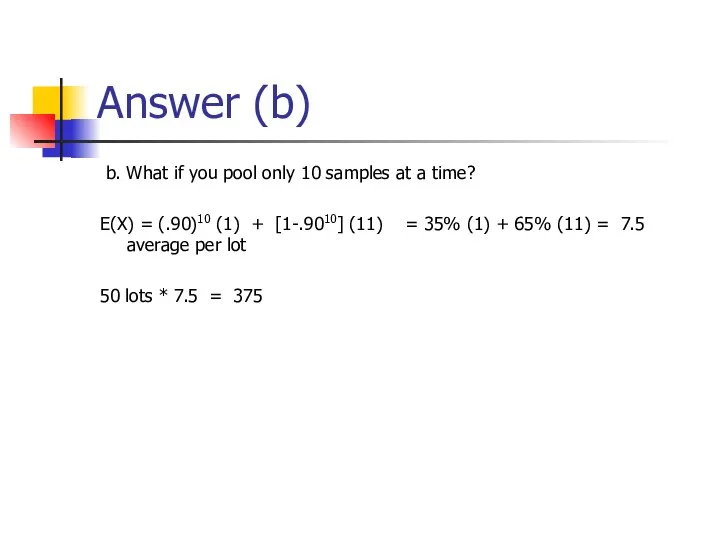

b. What if you pool only 10 samples at a

Answer (b)

b. What if you pool only 10 samples at a

Слайд 50Answer (c)

c. 5 samples at a time?

E(X) = (.90)5 (1) + [1-.905]

Answer (c)

c. 5 samples at a time?

E(X) = (.90)5 (1) + [1-.905]

Слайд 51Practice Problem

If X is a random integer between 1 and

Practice Problem

If X is a random integer between 1 and

Слайд 52Answer

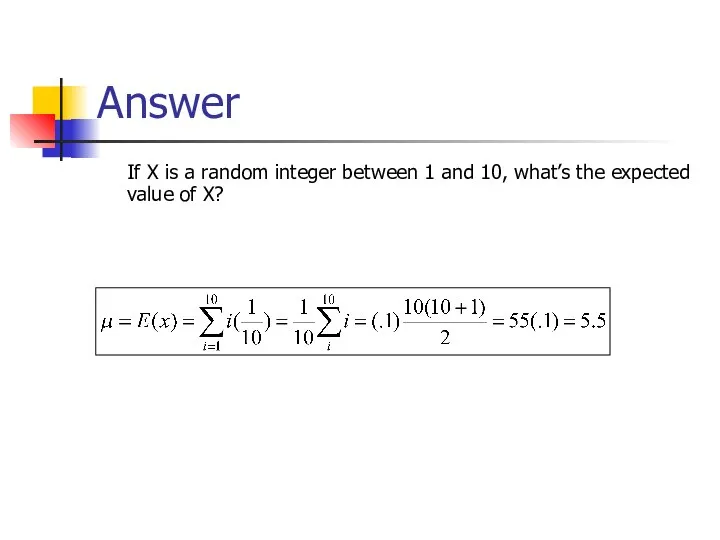

If X is a random integer between 1 and 10, what’s the

Answer

If X is a random integer between 1 and 10, what’s the

Слайд 53Expected value isn’t everything though…

Take the show “Deal or No Deal”

Everyone know

Expected value isn’t everything though…

Take the show “Deal or No Deal”

Everyone know

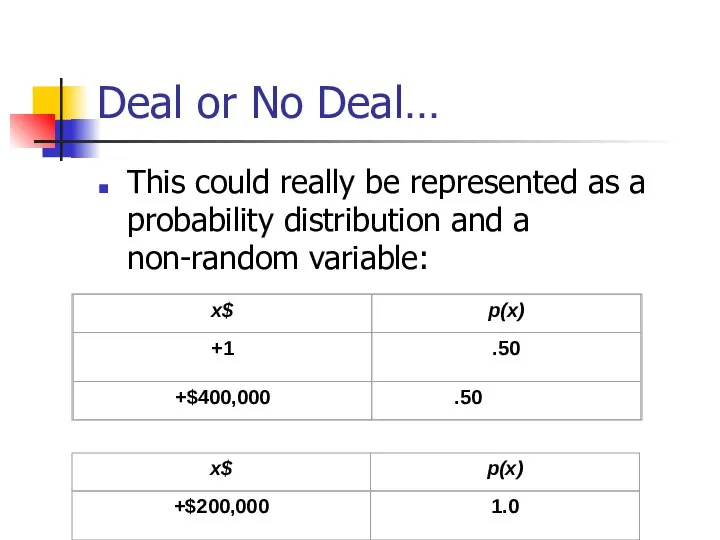

Слайд 54Deal or No Deal…

This could really be represented as a probability distribution

Deal or No Deal…

This could really be represented as a probability distribution

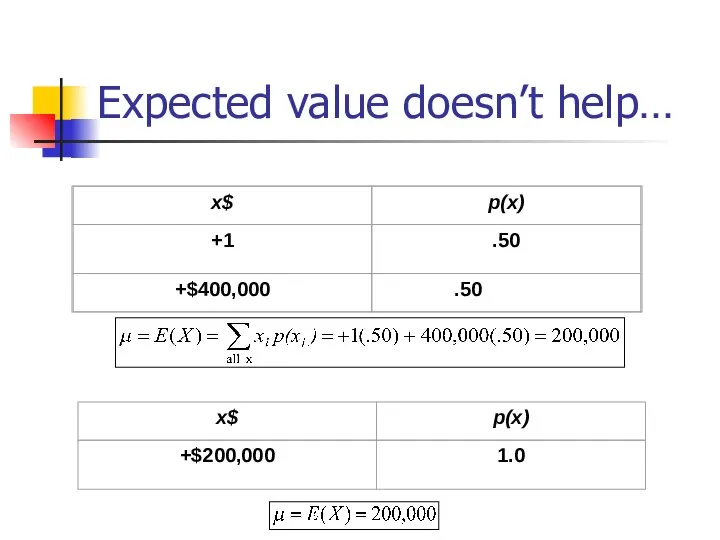

Слайд 55Expected value doesn’t help…

Expected value doesn’t help…

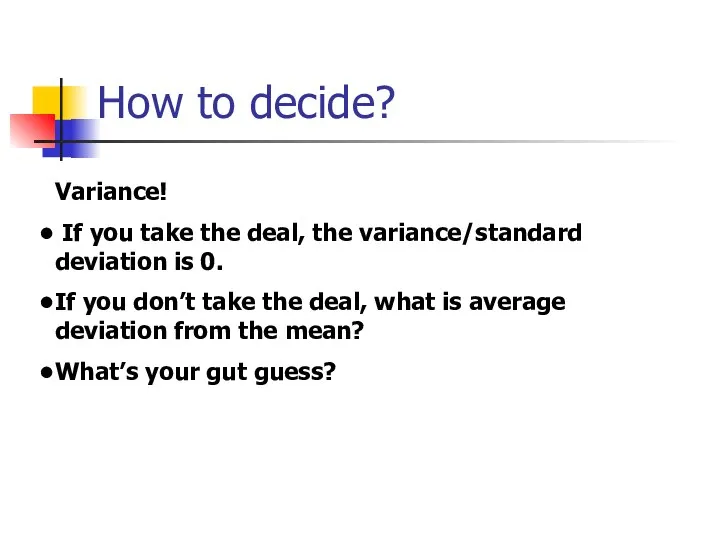

Слайд 56How to decide?

Variance!

If you take the deal, the variance/standard deviation

How to decide?

Variance!

If you take the deal, the variance/standard deviation

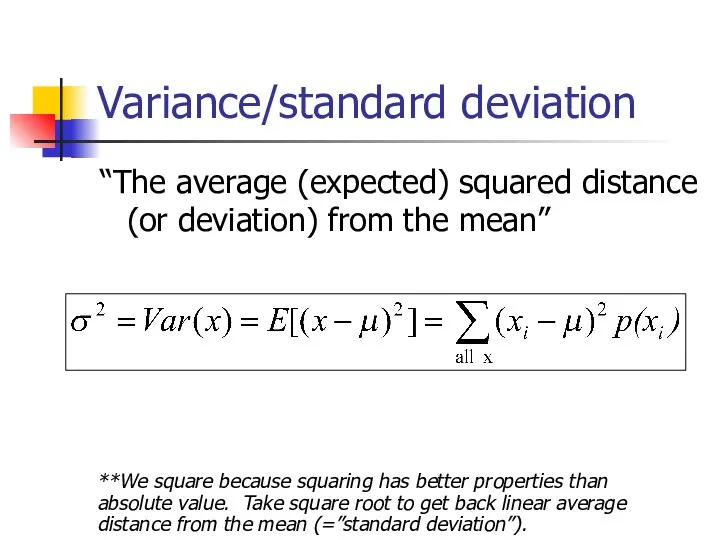

Слайд 57Variance/standard deviation

“The average (expected) squared distance (or deviation) from the mean”

**We square

Variance/standard deviation

“The average (expected) squared distance (or deviation) from the mean”

**We square

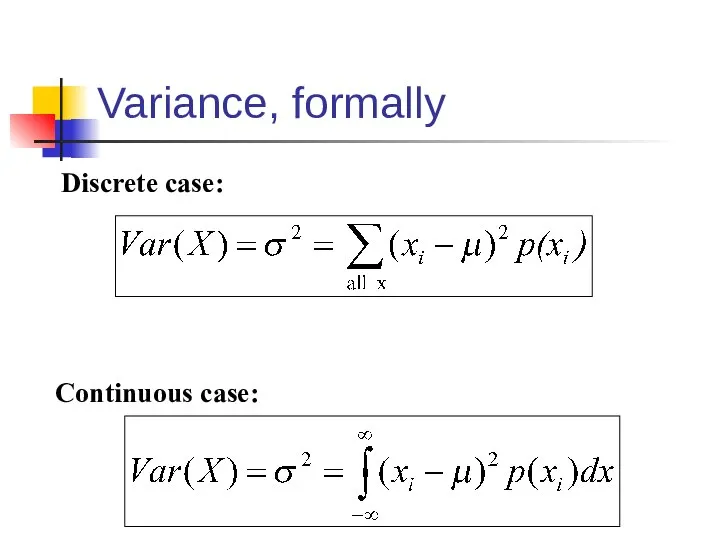

Слайд 58Variance, formally

Discrete case:

Continuous case:

Variance, formally

Discrete case:

Continuous case:

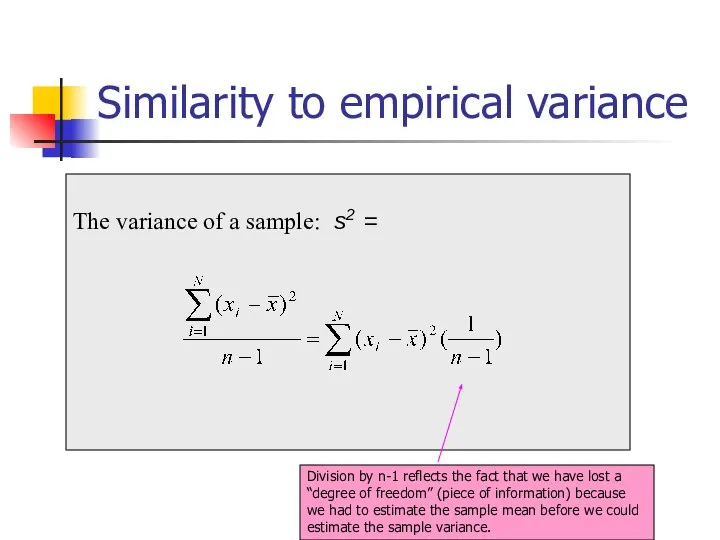

Слайд 59Similarity to empirical variance

The variance of a sample: s2 =

Similarity to empirical variance

The variance of a sample: s2 =

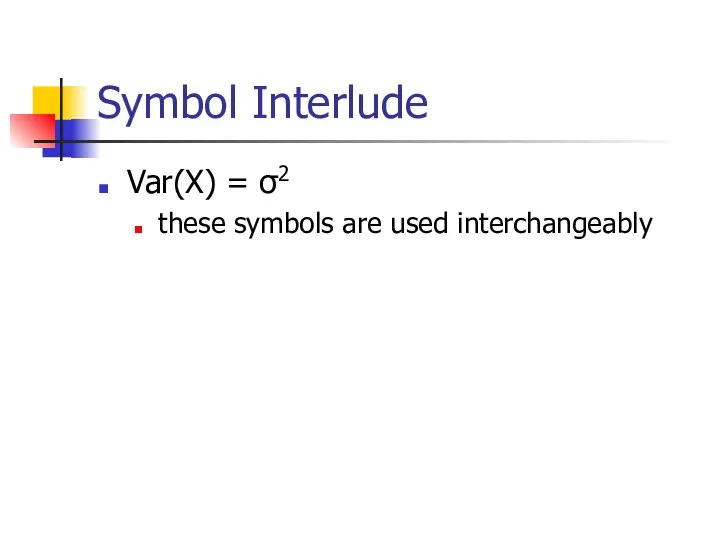

Слайд 60Symbol Interlude

Var(X) = σ2

these symbols are used interchangeably

Symbol Interlude

Var(X) = σ2

these symbols are used interchangeably

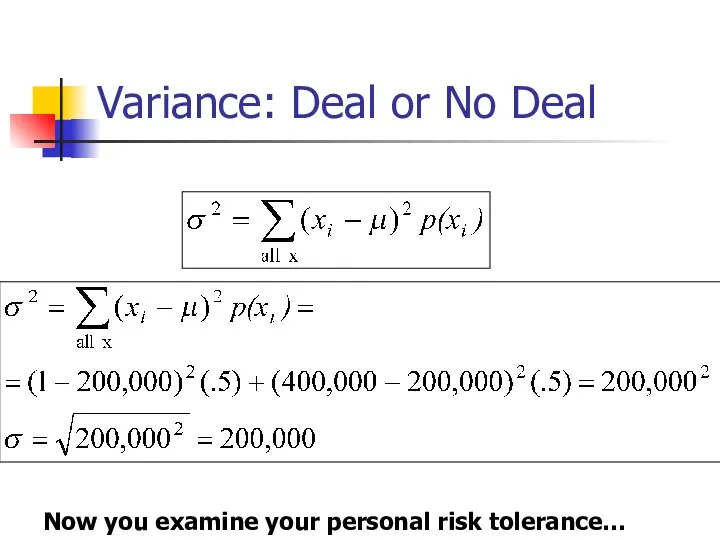

Слайд 61Variance: Deal or No Deal

Now you examine your personal risk tolerance…

Variance: Deal or No Deal

Now you examine your personal risk tolerance…

Слайд 62Practice Problem

A roulette wheel has the numbers 1 through 36, as well

Practice Problem

A roulette wheel has the numbers 1 through 36, as well

Слайд 63Answer

Standard deviation is $.99. Interpretation: On average, you’re either 1 dollar above

Answer

Standard deviation is $.99. Interpretation: On average, you’re either 1 dollar above

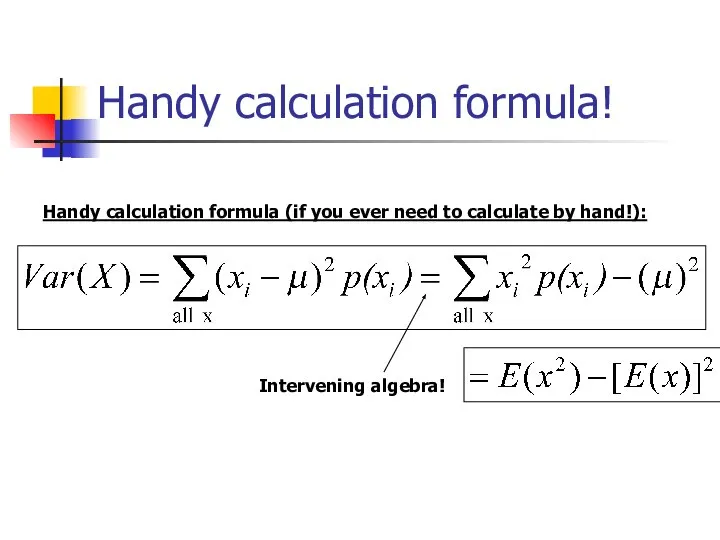

Слайд 64Handy calculation formula!

Handy calculation formula (if you ever need to calculate by

Handy calculation formula!

Handy calculation formula (if you ever need to calculate by

Слайд 65Var(x) = E(x-μ)2 = E(x2) – [E(x)]2 (your calculation formula!)

Proofs (optional!):

E(x-μ)2

Var(x) = E(x-μ)2 = E(x2) – [E(x)]2 (your calculation formula!)

Proofs (optional!):

E(x-μ)2

![Var(x) = E(x-μ)2 = E(x2) – [E(x)]2 (your calculation formula!) Proofs (optional!):](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/1058868/slide-64.jpg)

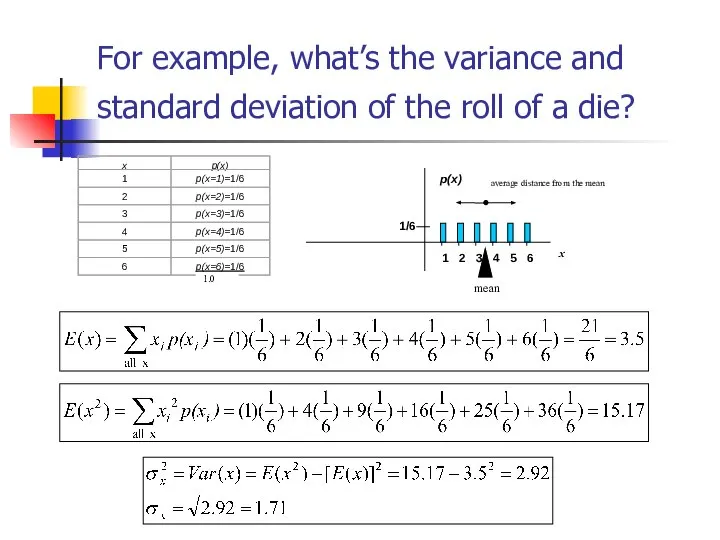

Слайд 66For example, what’s the variance and standard deviation of the roll of

For example, what’s the variance and standard deviation of the roll of

Слайд 67**A few notes about Variance as a mathematical operator:

If c= a constant

**A few notes about Variance as a mathematical operator:

If c= a constant

Слайд 68Var(c) = 0

Var(c) = 0

Constants don’t vary!

Var(c) = 0

Var(c) = 0

Constants don’t vary!

Слайд 69Var (c+X)= Var(X)

Var (c+X)= Var(X)

Adding a constant to every instance of a

Var (c+X)= Var(X)

Var (c+X)= Var(X)

Adding a constant to every instance of a

Слайд 70Var (c+X)= Var(X)

Var (c+X)= Var(X)

Adding a constant to every instance of a

Var (c+X)= Var(X)

Var (c+X)= Var(X)

Adding a constant to every instance of a

Слайд 71Var(cX)= c2Var(X)

Var(cX)= c2Var(X)

Multiplying each instance of the random variable by c makes

Var(cX)= c2Var(X)

Var(cX)= c2Var(X)

Multiplying each instance of the random variable by c makes

Слайд 72Var(X+Y)= Var(X) + Var(Y)

Var(X+Y)= Var(X) + Var(Y) ONLY IF X and Y

Var(X+Y)= Var(X) + Var(Y)

Var(X+Y)= Var(X) + Var(Y) ONLY IF X and Y

Слайд 73Example of Var(X+Y)= Var(X) + Var(Y): TPMT

TPMT metabolizes the drugs 6- mercaptopurine,

Example of Var(X+Y)= Var(X) + Var(Y): TPMT

TPMT metabolizes the drugs 6- mercaptopurine,

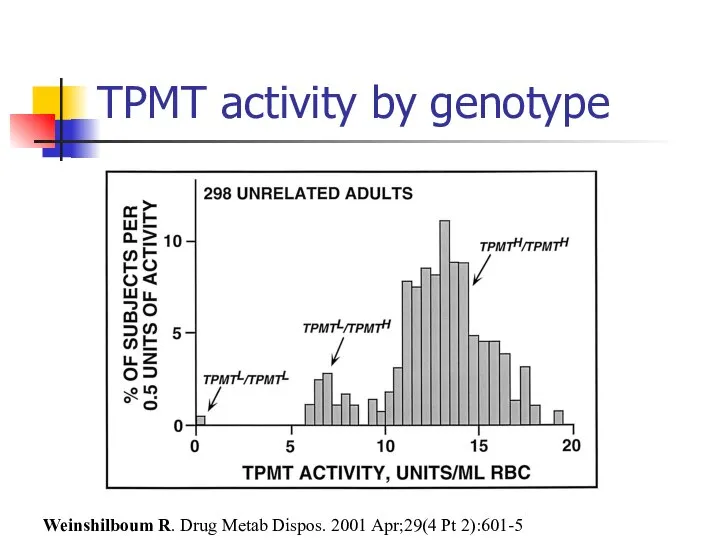

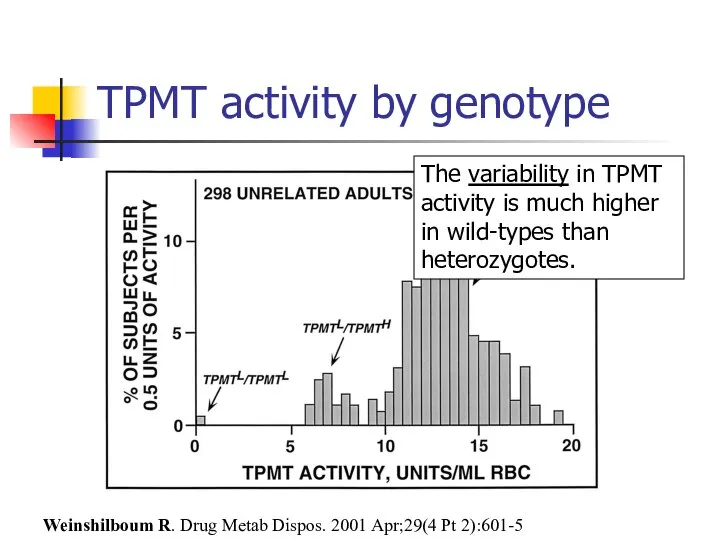

Слайд 74TPMT activity by genotype

Weinshilboum R. Drug Metab Dispos. 2001 Apr;29(4 Pt 2):601-5

TPMT activity by genotype

Weinshilboum R. Drug Metab Dispos. 2001 Apr;29(4 Pt 2):601-5

Слайд 75TPMT activity by genotype

Weinshilboum R. Drug Metab Dispos. 2001 Apr;29(4 Pt 2):601-5

The

TPMT activity by genotype

Weinshilboum R. Drug Metab Dispos. 2001 Apr;29(4 Pt 2):601-5

The

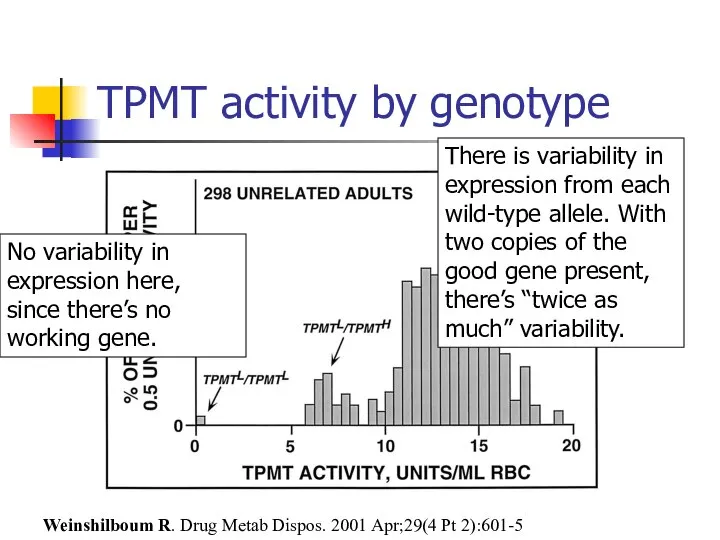

Слайд 76TPMT activity by genotype

Weinshilboum R. Drug Metab Dispos. 2001 Apr;29(4 Pt 2):601-5

There

TPMT activity by genotype

Weinshilboum R. Drug Metab Dispos. 2001 Apr;29(4 Pt 2):601-5

There

Слайд 77Practice Problem

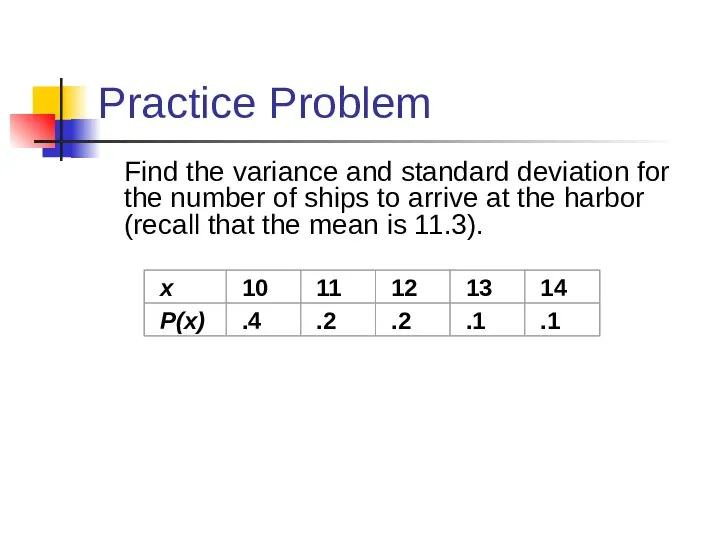

Find the variance and standard deviation for the number of ships

Practice Problem

Find the variance and standard deviation for the number of ships

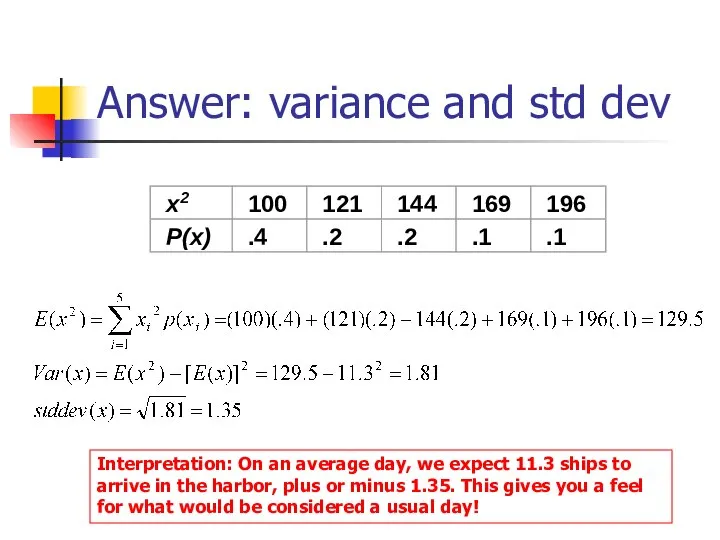

Слайд 78Answer: variance and std dev

Interpretation: On an average day, we expect 11.3

Answer: variance and std dev

Interpretation: On an average day, we expect 11.3

Слайд 79Practice Problem

You toss a coin 100 times. What’s the expected number of

Practice Problem

You toss a coin 100 times. What’s the expected number of

Слайд 80Answer: expected value

Intuitively, we’d probably all agree that we expect around 50

Answer: expected value

Intuitively, we’d probably all agree that we expect around 50

Слайд 81Answer: variance

What’s the variability, though? More tricky. But, again, we could do

Answer: variance

What’s the variability, though? More tricky. But, again, we could do

Слайд 82Or use computer simulation…

Flip coins virtually!

Flip a virtual coin 100 times; count

Or use computer simulation…

Flip coins virtually!

Flip a virtual coin 100 times; count

Слайд 83Coin tosses…

Mean = 50

Std. dev = 5

Follows a normal distribution

∴95% of the

Coin tosses…

Mean = 50

Std. dev = 5

Follows a normal distribution

∴95% of the

Слайд 84Covariance: joint probability

The covariance measures the strength of the linear relationship between

Covariance: joint probability

The covariance measures the strength of the linear relationship between

Слайд 85The Sample Covariance

The sample covariance:

The Sample Covariance

The sample covariance:

Стародубцева Анна 9-а класс

Стародубцева Анна 9-а класс Площадь поверхности прямоугольного параллелепипеда

Площадь поверхности прямоугольного параллелепипеда Центральная симметрия

Центральная симметрия Учимся писать цифры

Учимся писать цифры Длина окружности и площадь круга

Длина окружности и площадь круга Графики функций

Графики функций Сложение и вычитание вида ±1

Сложение и вычитание вида ±1 Решение линейных неравенств с одной переменной. Числовые промежутки. Урок 15

Решение линейных неравенств с одной переменной. Числовые промежутки. Урок 15 Сравнение предметов по некоторой величине без её измерения: выше - ниже, шире - уже

Сравнение предметов по некоторой величине без её измерения: выше - ниже, шире - уже Лекция 20

Лекция 20 Презентация на тему ЗАДАЧИ НА ПОСТРОЕНИЕ

Презентация на тему ЗАДАЧИ НА ПОСТРОЕНИЕ  Определенный интеграл. Пример 3

Определенный интеграл. Пример 3 Разность квадратов

Разность квадратов Сколько останется? Посчитай и назови ответ

Сколько останется? Посчитай и назови ответ Угол между двумя плоскостями

Угол между двумя плоскостями 70 задач на чертежах по планиметрии

70 задач на чертежах по планиметрии В мире треугольников. (1) 7 класс

В мире треугольников. (1) 7 класс Урок начинается. Занимательная математика

Урок начинается. Занимательная математика Понятия равно, не равно

Понятия равно, не равно Презентация на тему Натуральные числа (5 класс)

Презентация на тему Натуральные числа (5 класс)  Множества

Множества Логарифмическая линия в ЕГЭ

Логарифмическая линия в ЕГЭ Методика изучения массы

Методика изучения массы Координаты на прямой

Координаты на прямой Симметрия в нашей жизни

Симметрия в нашей жизни Презентация на тему Наибольшее и наименьшее значения функции

Презентация на тему Наибольшее и наименьшее значения функции  Лекция 2 Плоскость как поверхность I порядка. Уравнения плоскости и их исследование

Лекция 2 Плоскость как поверхность I порядка. Уравнения плоскости и их исследование Нормальные формы булевых функций

Нормальные формы булевых функций